Title Vii Of The Dodd-frank Act Pillars In Michigan

Description

Form popularity

FAQ

To achieve Dodd-Frank compliance for communication, financial organizations must take steps to preserve email communication for specific periods of time with redundancy and fail-safe procedures to ensure that it is protected. Firms must also make email communications accessible for e-discovery when necessary.

To promote the financial stability of the United States by improving accountability and transparency in the financial system, to end "too big to fail," to protect the American taxpayer by ending bailouts, to protect consumers from abusive financial services practices, and for other purposes.

To achieve Dodd-Frank compliance for communication, financial organizations must take steps to preserve email communication for specific periods of time with redundancy and fail-safe procedures to ensure that it is protected. Firms must also make email communications accessible for e-discovery when necessary.

Title VII subjects dealers and market participants to new internal and external business conduct requirements, such as establishing procedures for detecting internal conflicts of interests and requiring increased disclosures of material information about a swap or SBS to counterparties.

Title VII of the Dodd-Frank Act ("Title VII'), provides that the Securities and Exchange Commission ("SEC') and the Commodity Futures Trading Commission ("CFTC') (collectively, "the Commissions'), in consultation with the Board of Governors of the Federal Reserve System, shall jointly further define certain key terms ( ...

This might include making false or exaggerated claims, greenwashing, data manipulation, carbon offset fraud, and many other unethical practices. The Dodd-Frank Act provides protections for whistleblowers who report violations of securities law, especially those related to ESG fraud.

Simple principles like. . . . Markets should be transparent. Regulation should be consistent, without gaps that can be exploited by those who wish to indulge in risky, destabilizing or illegal behavior. Market participants, not taxpayers, should bear the risks of their market activities.

Title VII of the Dodd-Frank Act contains the US framework regulating OTC derivatives (swaps), including its G20 commitments for the reporting, clearing and exchange trading, as well as margin requirements for non-cleared swaps.

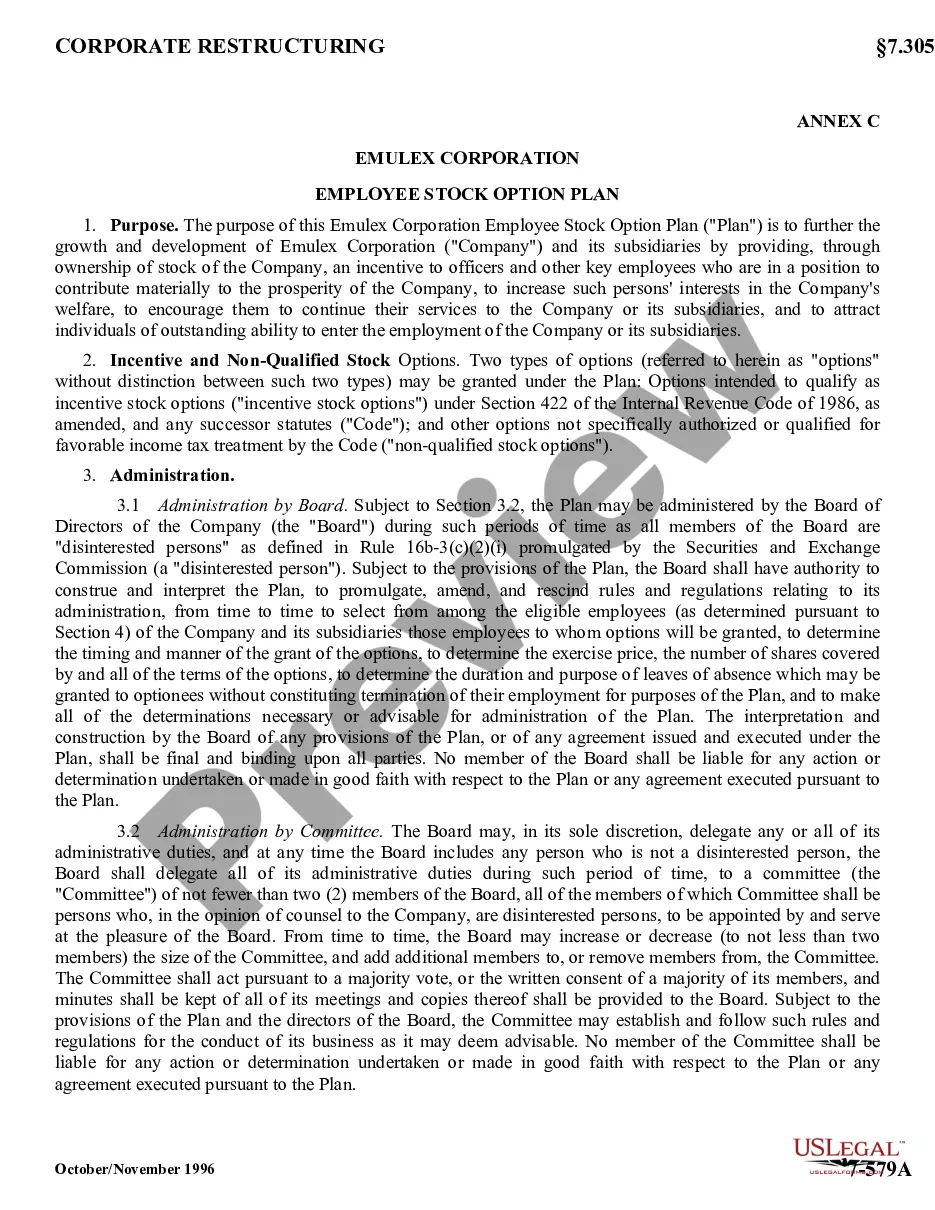

Basel regulation has evolved to comprise three pillars concerned with minimum capital requirements (Pillar 1), supervisory review (Pillar 2), and market discipline (Pillar 3). Today, the regulation applies to credit risk, market risk, operational risk and liquidity risk.