Affidavit Of Repossession With Car In Wayne

Description

Form popularity

FAQ

Know the Repo Laws of Your State. The first thing to know about how to repo a car is you need to be aware of how repo laws stand within the jurisdictions where you will conduct business. Make Sure the Debtor Is in Default. Locate and Verify the Car. Choose the Method to Repossess. Do Not Breach the Peace.

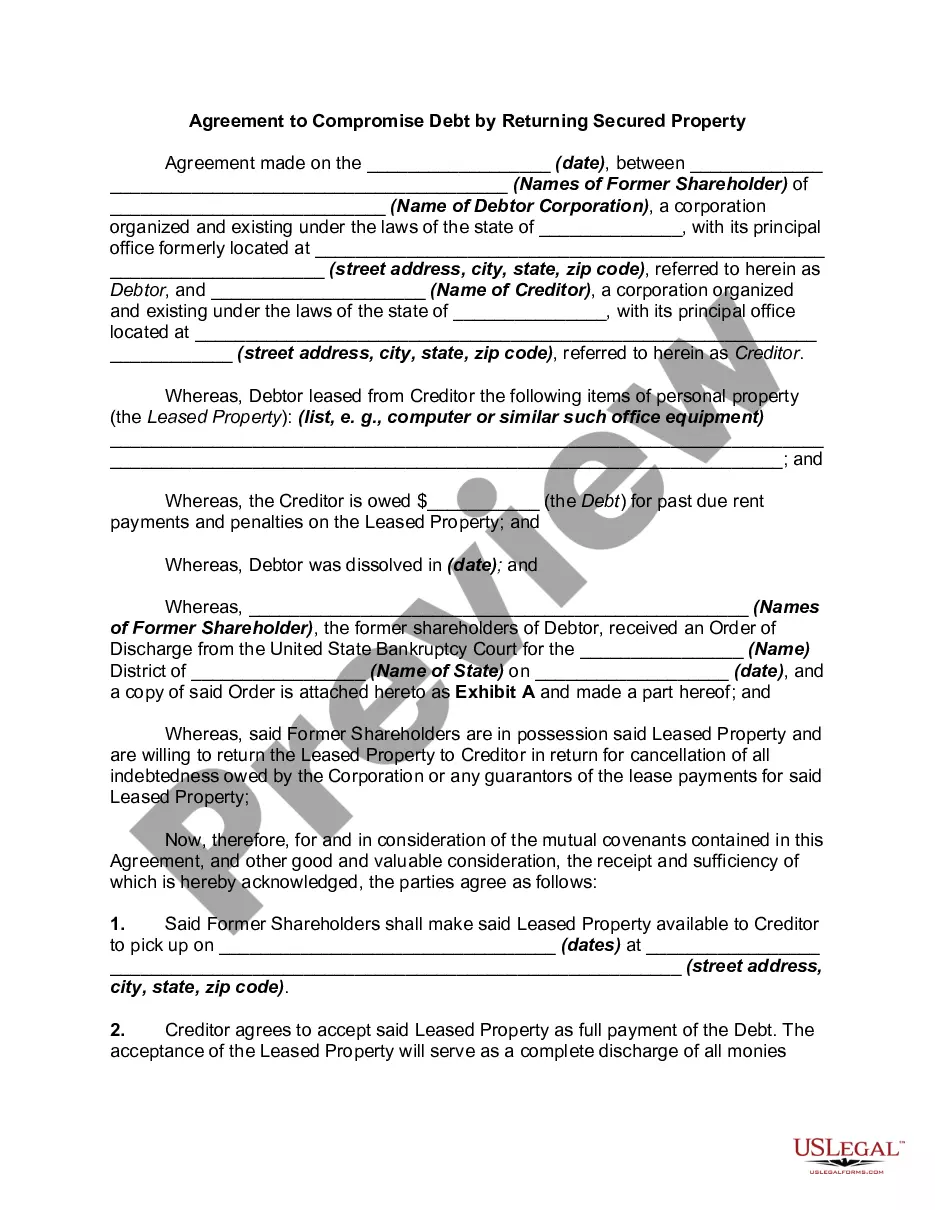

A repossession affidavit is a legal statement filed with the Department of Motor Vehicles when you repossess a car from a customer. This document provides details about the repossession such as why and how the vehicle was repossessed. It also informs government authorities that the vehicle has been repossessed.

What Happens If the Repo Agent Doesn't Find Your Car? But if you make it hard for the repo agent to get it, then the creditor may use another method to get the car back, called "replevin." Replevin can be just as costly as a repossession, if not more so.

Generally, cars are repossessed once payments are 90 days in default. Just don't expect lenders to give you a heads-up when the Repo Man will come calling. They typically contract that work out to towing services that specialize in snatching cars.

Each state has a different statute of limitations on car repossession debt, including auto loans, with most ranging from three to six years. After the statute of limitations has passed on your debt, debtors and collectors can still contact you.

There's no hard and fast rule on how much time you have to get a car back before the lender sells it. Generally speaking, the lender must give you notice that allows a "reasonable time" prior to the sale for you to react and exercise your options. At least ten days' notice is usually considered reasonable.

A creditor can repossess your automobile, but only if it can be done peacefully. The creditor cannot trick you into bringing your car to the shop in order to repossess it. The creditor cannot use any force or threats of violence to repossess your car.

There's no hard and fast rule on how much time you have to get a car back before the lender sells it. Generally speaking, the lender must give you notice that allows a "reasonable time" prior to the sale for you to react and exercise your options. At least ten days' notice is usually considered reasonable.