Residential Seller Financing With Sba Loan

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

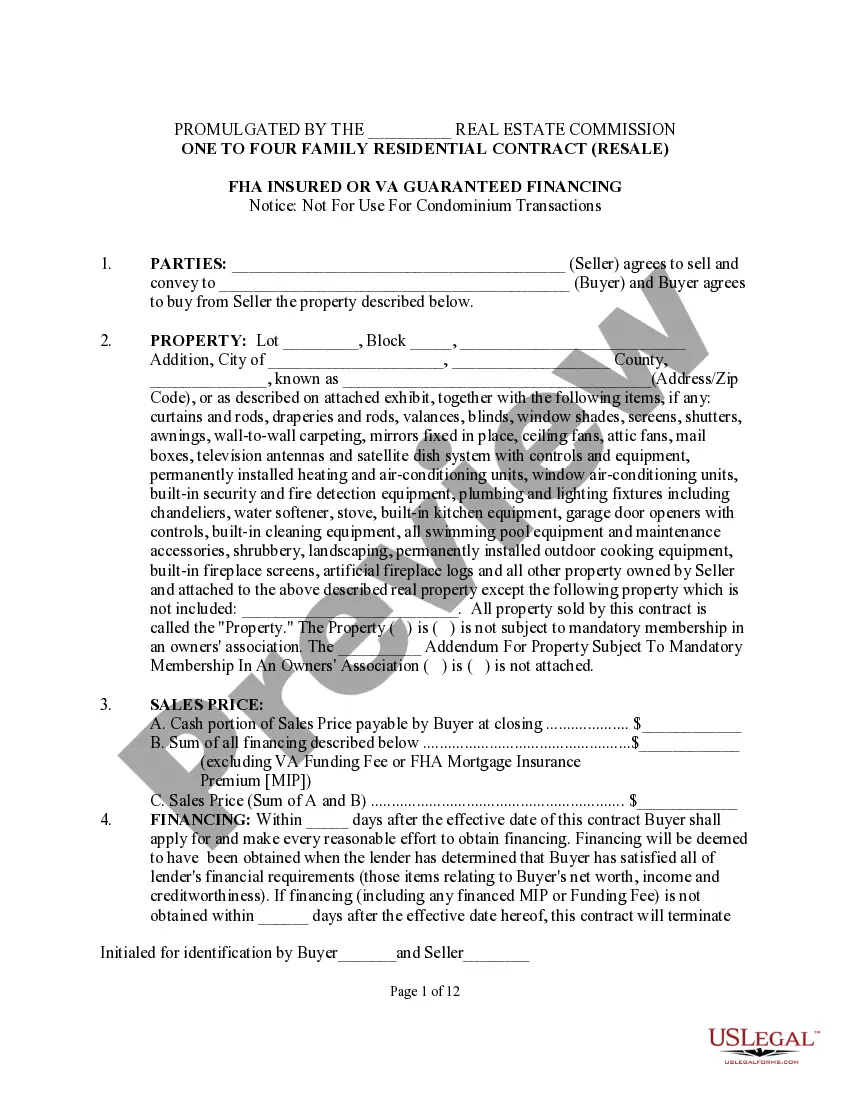

How to fill out Texas One To Four Family Residential Contract - Resale - All Cash, Assumption, Third Party Conventional Or Seller Financing?

It’s widely acknowledged that you cannot instantly become a legal authority, nor can you swiftly understand how to draft Residential Seller Financing With Sba Loan without having a specialized background.

Drafting legal documents is a lengthy process that requires specific training and expertise.

So why not entrust the drafting of the Residential Seller Financing With Sba Loan to the experts.

Preview it (if this option is available) and review the supporting description to see if Residential Seller Financing With Sba Loan is what you require.

Create a free account and select a subscription plan to purchase the template.

- With US Legal Forms, one of the most extensive legal document collections, you can locate anything from court forms to templates for internal communication.

- We understand the significance of compliance with federal and state laws and regulations.

- That’s why, on our site, all forms are location-specific and current.

- Here’s how you can begin with our platform and acquire the document you need in just minutes.

- Discover the form you need using the search bar at the top of the page.

Form popularity

FAQ

Here are three main ways to structure a seller-financed deal: Use a Promissory Note and Mortgage or Deed of Trust. If you're familiar with traditional mortgages, this model will sound familiar. ... Draft a Contract for Deed. ... Create a Lease-purchase Agreement.

There are two SBA loan types that can be used to buy real estate: SBA 7(a) loans and 504 loans. These loans, guaranteed by the SBA, offer large loan amounts, competitive interest rates and lengthy repayment terms. They can also be used to construct or renovate buildings, as well as to make improvements to land.

Seller Financing Sometimes, there is a margin between the amount that the buyer puts down and the amount covered by the SBA loan. If this occurs, the seller can extend seller financing terms. Selling financing allows the buyer to pay the seller a portion of the purchase price over time.

Most SBA lenders allow buyers to make payments on the seller financing, so long as they do not default on the SBA loan. However, a few will accept no payments on the seller financing until the SBA loan is satisfied. We highly recommend avoiding those lenders.

In change of ownership transactions, Sellers may agree to finance a portion of the purchase price through the use of a promissory note (?Seller Note?). Seller financing reduces the amount of the bank financing and thus reduces the risk to the Lender.