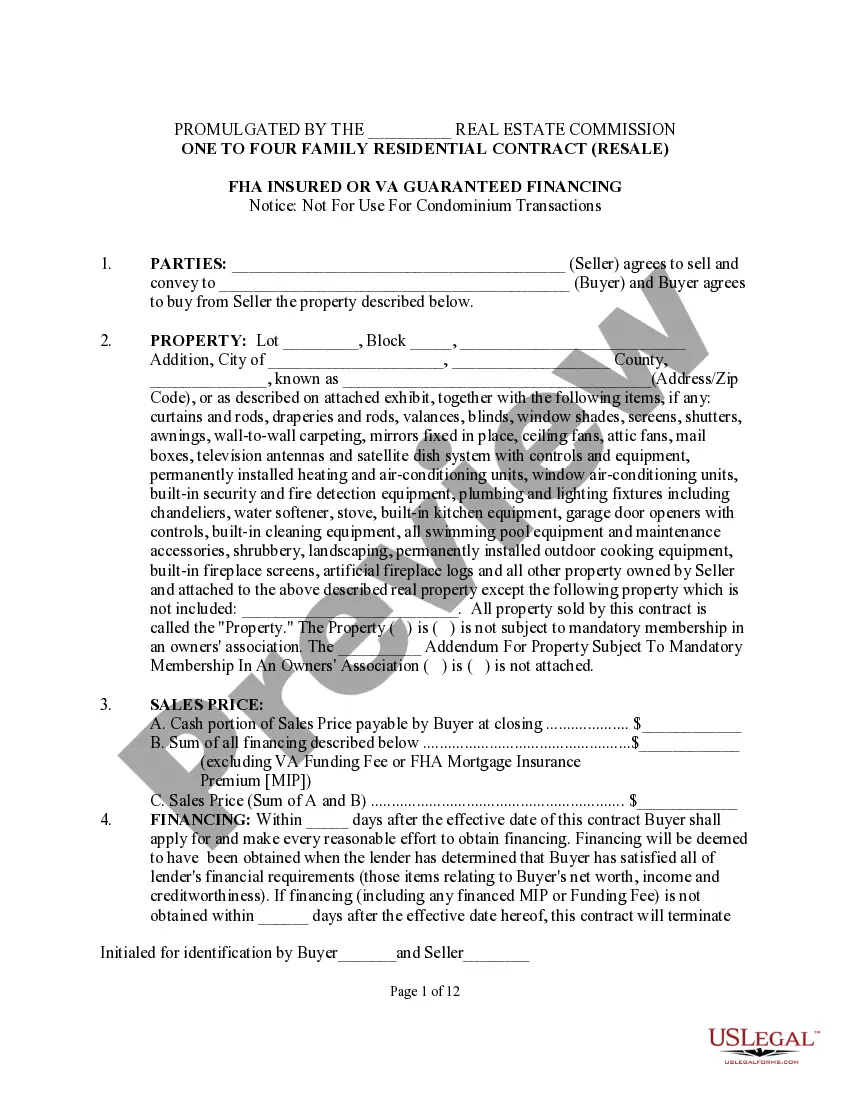

Residential Seller Financing With Balloon Payment

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Texas One To Four Family Residential Contract - Resale - All Cash, Assumption, Third Party Conventional Or Seller Financing?

Locating a primary source to obtain the most up-to-date and pertinent legal templates is half the battle when dealing with bureaucracy.

Identifying the appropriate legal documents requires precision and careful attention to detail, which is why it is essential to source samples of Residential Seller Financing With Balloon Payment exclusively from trustworthy providers, such as US Legal Forms. An incorrect template can squander your time and delay your situation.

Once you have the form on your device, you can alter it using the editor or print it out and complete it manually. Eliminate the hassle associated with your legal documentation. Explore the extensive US Legal Forms library where you can discover legal templates, verify their relevance to your situation, and download them right away.

- Utilize the library navigation or search option to find your template.

- Examine the form’s description to ensure it meets the criteria of your state and area.

- Check the form preview, if available, to confirm the template is what you need.

- Return to the search and seek the correct document if the Residential Seller Financing With Balloon Payment does not suit your requirements.

- When you are confident about the form’s applicability, download it.

- If you are a registered customer, click Log in to verify your identity and access your selected templates in My documents.

- If you do not have an account yet, click Buy now to acquire the form.

- Select the pricing option that aligns with your preferences.

- Proceed to registration to complete your purchase.

- Finalize your transaction by choosing a payment method (credit card or PayPal).

- Select the file format for downloading Residential Seller Financing With Balloon Payment.

Form popularity

FAQ

There are also some risks associated with balloon mortgages, including defaulting on the loan if you're unable to make the balloon payment at the end of the loan term. In such cases, your lender will likely take steps to foreclose on your home.

A balloon payment isn't allowed in a type of loan called a Qualified Mortgage, with some limited exceptions. Tip: A mortgage with a balloon payment can be risky because you owe a larger payment at the end of the loan.

One option is to refinance your balloon payment. This allows you to break the lump sum down into manageable monthly payments. The beauty of this is you won't need to use your cash savings to become the proud owner of the car you've been paying off!

The original promissory note is held by the seller. The buyer pays back the loan, typically with interest, over time. These loans can be short-term, and may include a balloon payment, meaning a lump sum is paid during or at the end of the term.

If you don't have the funds to settle your balloon payment and if you don't qualify for credit for refinancing, then you risk repossession. This could also get you blacklisted. It's more expensive.