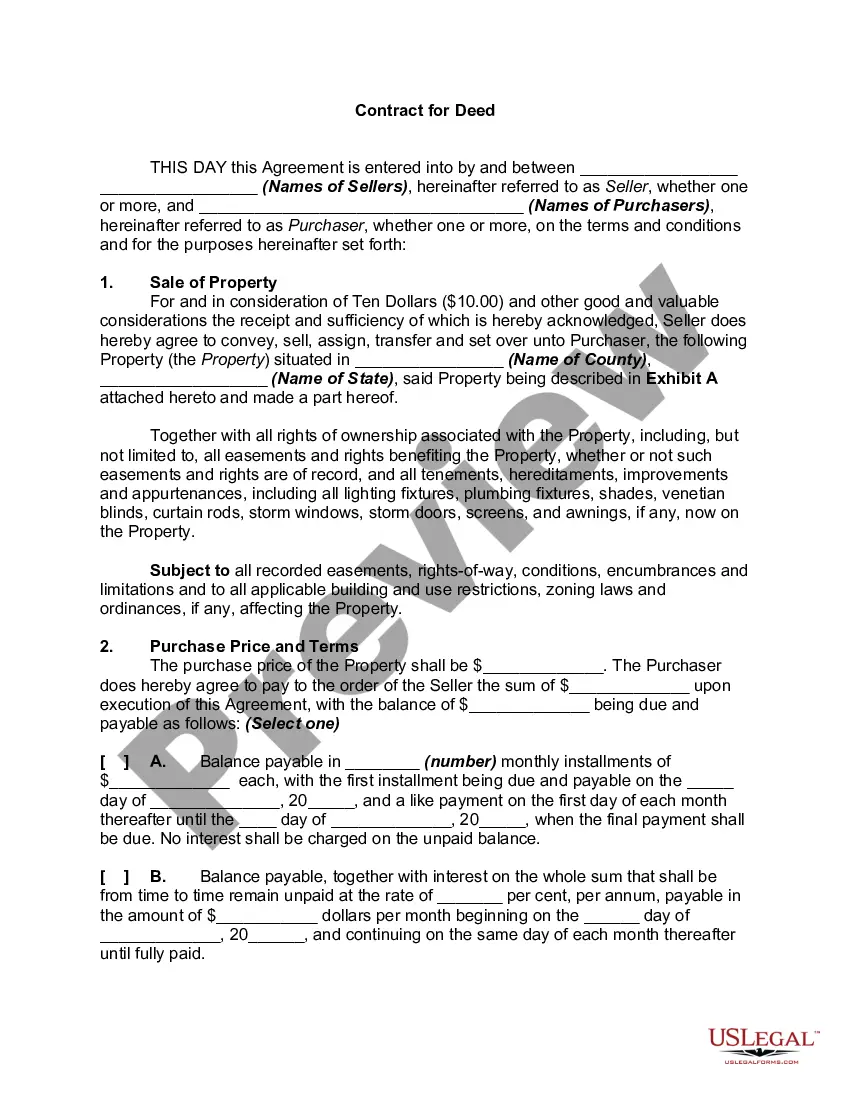

Bond For Deed With A Mortgage

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Louisiana Bond For Deed - Contract For Deed?

What is the most reliable service to obtain the Bond For Deed With A Mortgage and other updated editions of legal paperwork? US Legal Forms is the answer! It's the finest collection of legal documents for any purpose.

Each template is expertly crafted and verified for adherence to federal and local regulations. They are categorized by area and state of application, making it easy to find the one you require.

US Legal Forms is an outstanding resource for anyone needing to manage legal documents. Premium users can enjoy even more benefits as they can complete and authorize previously saved forms electronically at any time using the built-in PDF editing tool. Try it out today!

- Seasoned users of the platform only need to Log In to the system, verify if their subscription is current, and click the Download button next to the Bond For Deed With A Mortgage to obtain it.

- Once saved, the template remains accessible for future use in the My documents section of your account.

- If you do not yet have an account with us, here are the steps you must follow to create one.

- Form compliance evaluation. Before acquiring any template, you need to ensure that it meets your use case requirements and your state or county's regulations. Review the form description and utilize the Preview if it is offered.

Form popularity

FAQ

For sellers, a contract for deed with a mortgage can be an advantageous option, especially in a competitive real estate market. It enables sellers to attract buyers who might struggle with conventional financing. Additionally, sellers can potentially benefit from a steady income stream while maintaining ownership until the buyer fulfills the contract terms.

One disadvantage of a contract for deed with a mortgage is the limited buyer protections compared to traditional financing. If the seller defaults or faces financial difficulties, the buyer risks losing their investment. Additionally, since the seller retains legal title, the buyer may lack control over decisions regarding the property until the contract concludes, which can create uncertainty.

People often choose a contract for deed with a mortgage as an alternative to traditional home buying methods. It allows buyers to secure a home even if they face challenges obtaining a conventional mortgage. Sellers benefit as well by reaching a broader pool of potential buyers who may not qualify for typical financing options.

A mortgage bond is a financial security backed by a pool of mortgages, where payments from borrowers generate income for bondholders. This structure allows investors to gain exposure to the real estate market without needing to own property directly. Furthermore, a bond for deed with a mortgage typically operates similarly, ensuring that the lender has a secured interest in the property until full payment is received.

In American English, a deed is described as a formal written document that creates, transfers, or assigns an interest in real property. The deed establishes legal rights and helps resolve disputes related to property ownership. When discussing a bond for deed with a mortgage, it is essential to understand the deed's role in protecting your interests and ensuring a successful property transfer.

An example of a deed is a warranty deed, which provides a guarantee that the seller holds clear title to the property and has the right to sell it. In many cases, a bond for deed with a mortgage may also involve a quitclaim deed that allows the seller to transfer whatever interest they have in the property without any guarantees. Each type of deed has distinct implications, so selecting the appropriate one is important for successful property ownership.

In the United States, a deed is an official document that serves to transfer real property rights from one person to another. It includes essential details like the buyer and seller's names, the property's description, and any encumbrances that may affect the title. When you engage in a bond for deed with a mortgage, understanding the deed’s implications is crucial to ensuring a smooth property transaction.

A deed is a legal document that formally conveys property ownership from one party to another. In the context of a bond for deed with a mortgage, it outlines the agreement between the buyer and the seller regarding the property's transfer, while providing security for the seller's interest. This process allows buyers to occupy the property before fully obtaining the title, making it a beneficial arrangement for both parties.

A bond for deed with a mortgage can be a beneficial arrangement for both buyers and sellers, particularly when traditional financing options are not available. This method enables buyers to acquire property while establishing a payment plan that suits their financial situation. However, it's essential to carefully consider the risks involved, including the potential for default. Using platforms like US Legal Forms can help you navigate these complexities and provide guidance throughout the process.

Yes, you can have a deed with a mortgage simultaneously. In this scenario, the property is encumbered by the mortgage, and the seller retains ownership through the deed until the buyer fulfills the contractual obligations. This arrangement, such as a bond for deed with a mortgage, allows the buyer to occupy the property while making payments. Be sure to communicate openly with your lender about these arrangements to ensure compliance with the mortgage agreement.