Modification Mortgage Rate With Good Credit

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

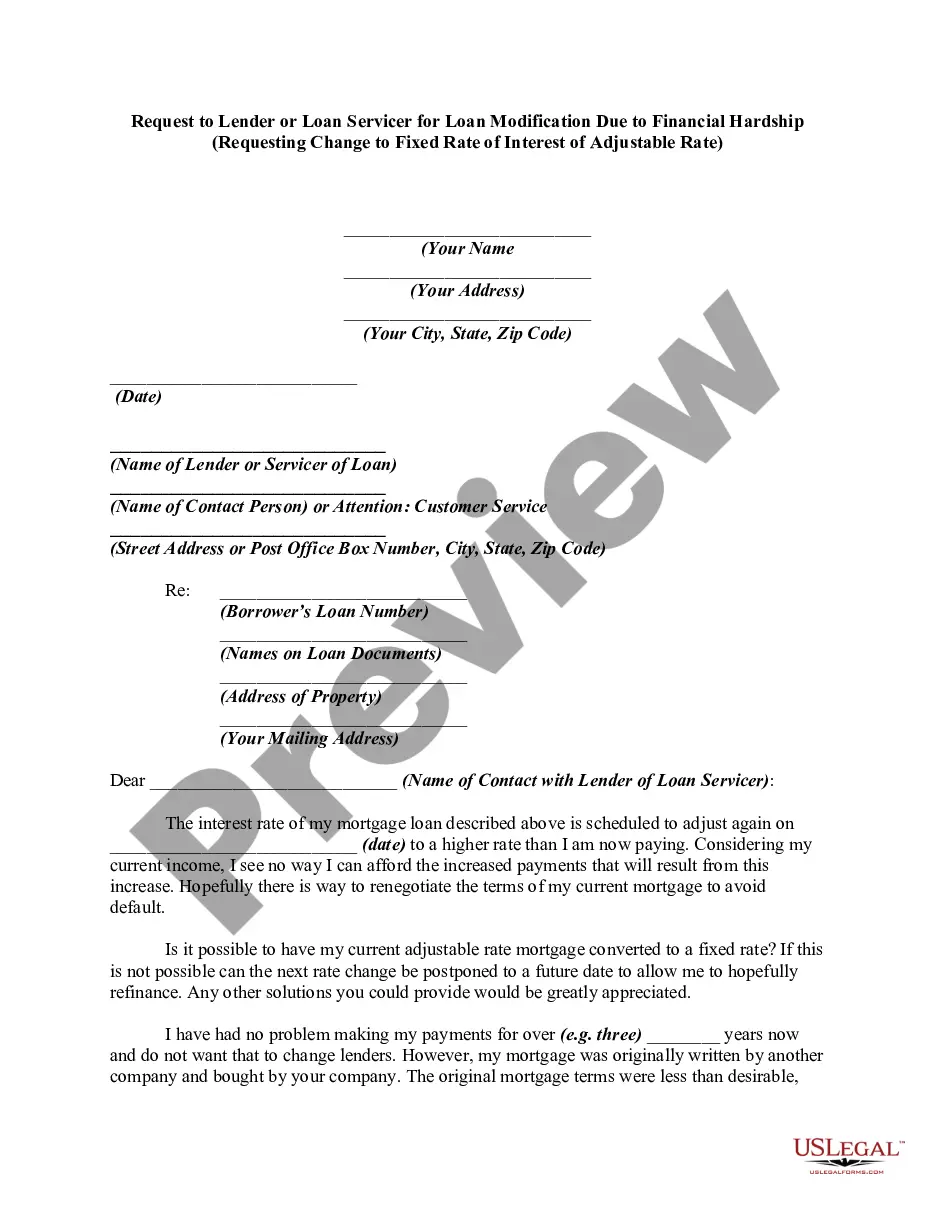

How to fill out Illinois Modification Of Mortgage Loan In Default To Bring It Current And To Change Variable Rate Of Interest To Fixed Rate?

The Modification Mortgage Rate With Good Credit you see on this page is a reusable legal template drafted by professional lawyers in accordance with federal and local regulations. For more than 25 years, US Legal Forms has provided individuals, companies, and legal professionals with more than 85,000 verified, state-specific forms for any business and personal scenario. It’s the quickest, most straightforward and most reliable way to obtain the documents you need, as the service guarantees bank-level data security and anti-malware protection.

Getting this Modification Mortgage Rate With Good Credit will take you only a few simple steps:

- Search for the document you need and check it. Look through the file you searched and preview it or check the form description to verify it satisfies your needs. If it does not, make use of the search bar to get the correct one. Click Buy Now once you have located the template you need.

- Subscribe and log in. Select the pricing plan that suits you and create an account. Use PayPal or a credit card to make a prompt payment. If you already have an account, log in and check your subscription to proceed.

- Obtain the fillable template. Choose the format you want for your Modification Mortgage Rate With Good Credit (PDF, DOCX, RTF) and download the sample on your device.

- Complete and sign the document. Print out the template to complete it by hand. Alternatively, use an online multi-functional PDF editor to rapidly and precisely fill out and sign your form with a eSignature.

- Download your papers one more time. Utilize the same document again anytime needed. Open the My Forms tab in your profile to redownload any earlier downloaded forms.

Sign up for US Legal Forms to have verified legal templates for all of life’s situations at your disposal.

Form popularity

FAQ

A modification typically changes the loan's rate or term (or both) to make monthly payments more affordable. Borrowers seeking a modification have to provide proof of hardship to their mortgage lender or servicer. Unlike forbearance, loan modifications are a permanent solution.

In many instances, the eligibility criteria for loan modification programs allow homeowners with low credit scores to participate. For example, the FHA Refinancing for Underwater Homes requires only a FICO score of 500. (FICO scores range from 300 to 850, with anything from 300 to 640 considered bad credit.)

You don't have a valid financial hardship reason. You make too much money and have too many assets. You have exceeded the number of loan modifications that you're allowed. Your investor does not offer loan modifications as a loss mitigation option.

Loan Modification: 10 Simple Tips for Success Explain your hardship. Why are you behind? ... Document your income. ... Outline your expenses. ... Gather your Federal Tax Returns. ... Provide proof of insurance. ... Be prepared to interview with a counselor. ... Stay connected. ... Deliver documents as requested.

Lenders will often report a loan modification to credit bureaus as a type of settlement or adjustment to the terms of the loan. If it shows up as not fulfilling the original terms of your loan, that can have a negative effect on your credit.