Llc Ltd

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

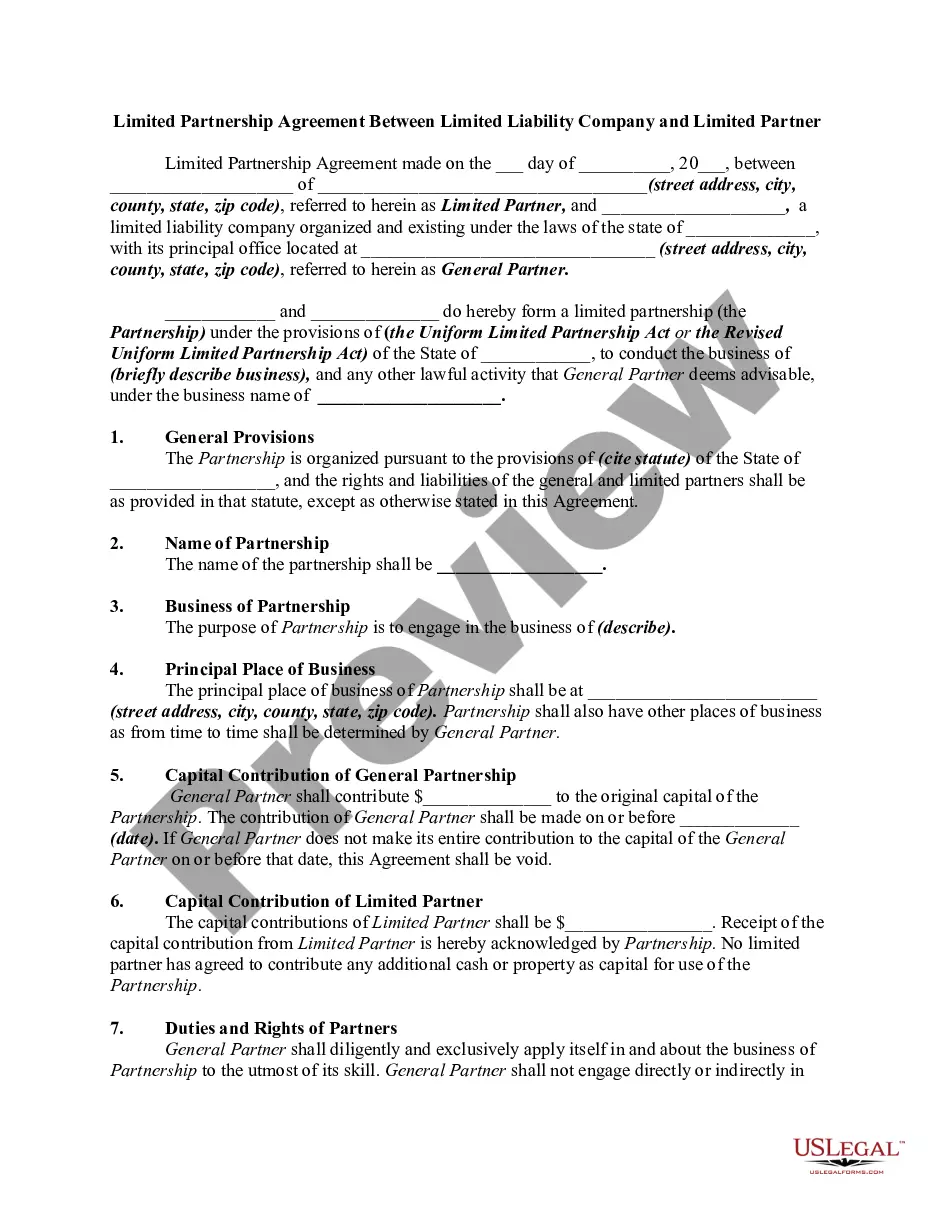

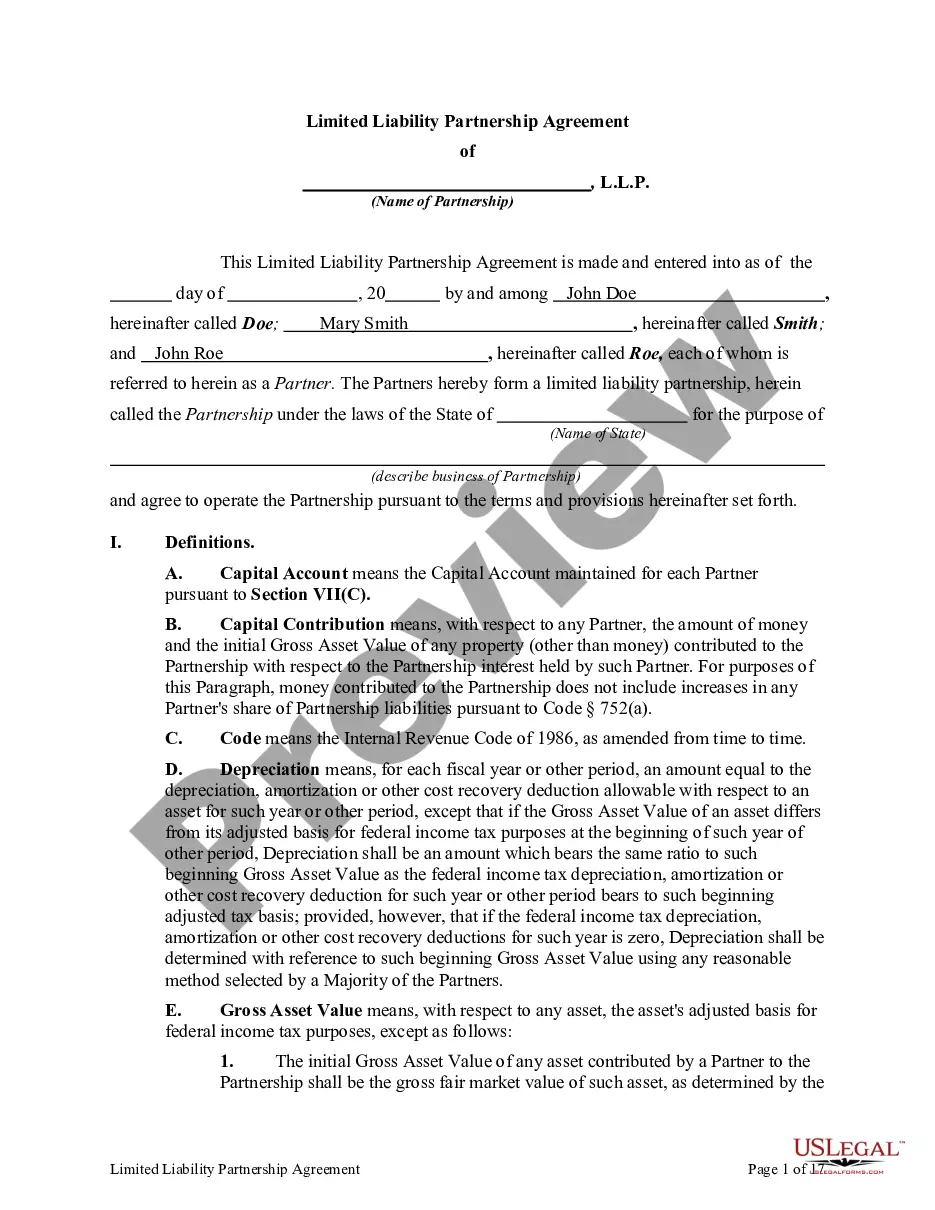

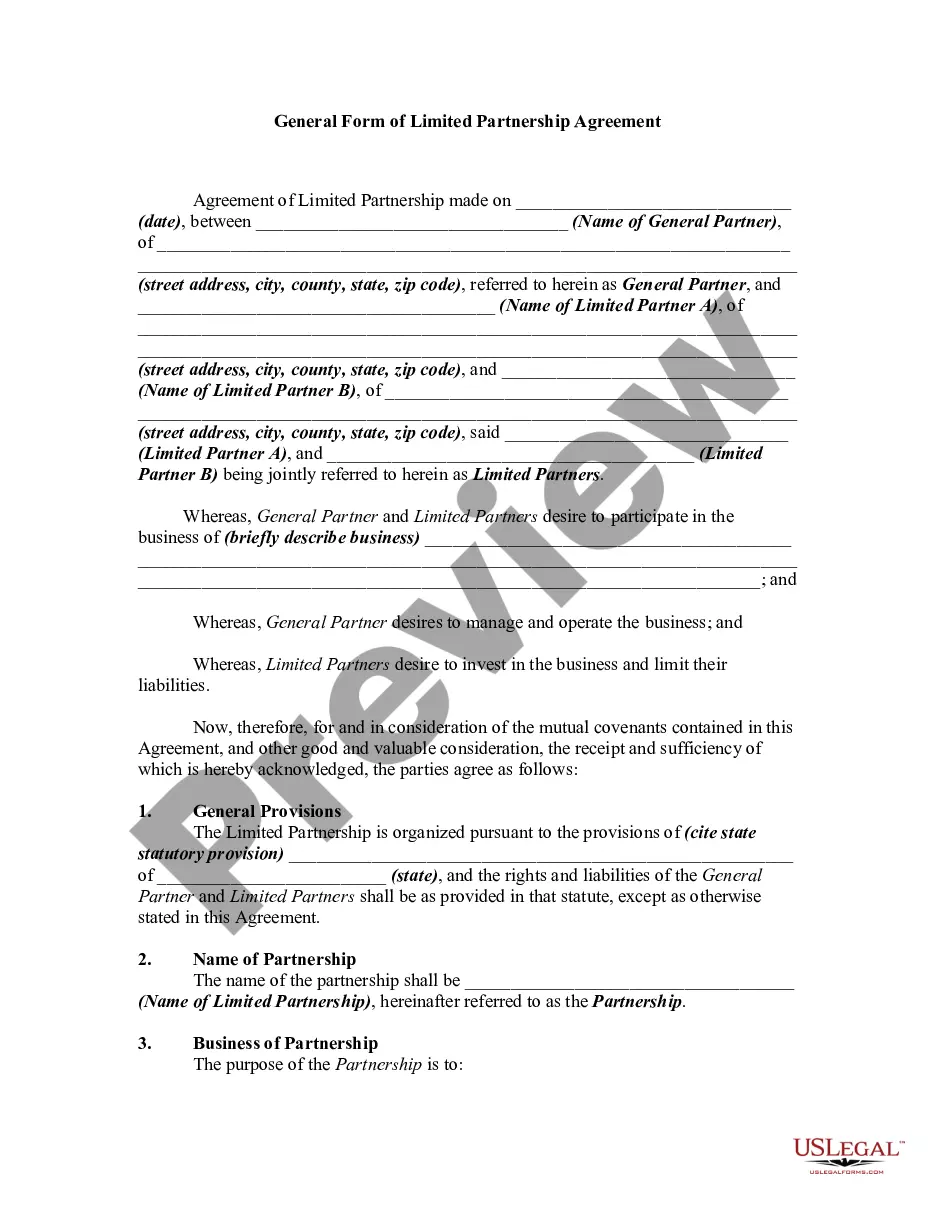

How to fill out Colorado Limited Partnership Agreement Between Limited Liability Company And Limited Partner?

- Log into your account if you're an existing user. Ensure your subscription is active before proceeding to download.

- Review the form preview carefully. Verify that the chosen document meets your specific needs and complies with your local jurisdiction.

- If you find inconsistencies, utilize the search function to explore alternative templates.

- Select and purchase the needed document. Click the 'Buy Now' button and choose your preferred subscription plan.

- Complete your transaction by entering your payment details or using your PayPal account.

- Download the document to your device and access it anytime in the 'My Forms' section of your profile.

US Legal Forms offers a unique advantage by providing over 85,000 editable legal forms, ensuring that you can find exactly what you need. With their robust library and access to premium expert assistance, you can confidently navigate legal processes.

Take charge of your legal needs today and explore the benefits of US Legal Forms. Start your journey by visiting their website!

Form popularity

FAQ

The US equivalent of a Limited Company (Ltd) is a Limited Liability Company (LLC). Both offer limited liability, but the operational and tax structures may differ. An LLC provides flexibility in management and taxation options, making it a popular choice for entrepreneurs. If you're exploring options for forming a business entity, consider using US Legal Forms to navigate the process of establishing your LLC ltd efficiently.

Yes, a Limited Company (Ltd) typically needs an Employer Identification Number (EIN) for tax purposes, especially if it has employees or plans to open a business bank account. An EIN serves as a unique identifier for your company, similar to how a Social Security number works for individuals. If you're forming an LLC ltd in the US, obtaining an EIN from the IRS is crucial for compliance and operational purposes.

While both LLCs and Ltds offer limited liability protections to their owners, they operate under different legal frameworks. LLCs are governed by state laws in the United States, whereas Ltds follow the regulations set in other countries, such as the UK. Additionally, the management and tax implications may vary between these structures. Therefore, understanding these differences is key when deciding whether to form an LLC ltd or a different entity type.

A Limited Company (Ltd) and a Limited Liability Company (LLC) are similar but differ primarily in their regulatory environments. Ltd is commonly used in the UK and other countries, while LLC is a US-based structure. Both provide limited liability protection, meaning owners are not personally responsible for business debts. Hence, if you're considering forming an LLC ltd, be aware of the legal distinctions between these entities.

To write a Limited Liability Company (LLC), you need to choose a unique name that includes 'LLC' or 'Limited Liability Company.' Next, you must file articles of organization with your state’s business filing body. Additionally, you should create an operating agreement that outlines the management structure and operating procedures. This is an important step to help protect your LLC ltd structure.

While a Ltd, or limited company, and an LLC both limit liability for their owners, they differ in structure and origin. A Ltd is commonly found in countries like the UK, while an LLC is primarily a US structure that offers flexibility in management and tax options. Understanding these distinctions can help you choose the right formation for your business. If you're considering options, the uslegalforms platform can assist you in navigating the details of both structures.

The tax rate for an LLC in Colorado can vary depending on the type of income the business generates. Generally, LLCs are treated as pass-through entities, meaning the income passes through to the members' personal tax returns. Therefore, the tax rate aligns with the individual rates, which range from 4.55% to 6.5%. Utilizing the uslegalforms platform can help you understand the specific tax obligations for an LLC in Colorado.

You can certainly file your LLC by itself, particularly if it elects to be treated as a corporation for tax purposes. This means your LLC will follow the corporate tax rules, separate from your personal taxes. To navigate this process successfully and avoid common pitfalls, consider obtaining resources from US Legal Forms that simplify forming and filing for your LLC.

Filing your LLC separately from your personal taxes is possible under certain conditions, especially if you elect to be taxed as a corporation. However, this approach may also create additional filing requirements and tax implications. Using US Legal Forms can provide the necessary guidance to ensure compliance with all tax obligations for both individual and LLC filings.

A single owner LLC generally files taxes as a sole proprietor, reporting business income and expenses on a Schedule C attached to their personal tax return. This simplifies the process, as it avoids double taxation often associated with corporations. Getting help through services like US Legal Forms can clarify the filing requirements and streamline your experience.