Debt Deduction On Les

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out California Authorization For Deduction From Pay For A Specific Debt?

The Debt Deduction On Les presented on this webpage is a reusable official template crafted by experienced attorneys in adherence to federal and local statutes and regulations.

For over 25 years, US Legal Forms has offered individuals, entities, and legal experts with more than 85,000 authenticated, state-specific documents for any business and personal needs. It’s the quickest, simplest, and most dependable method to acquire the paperwork you need, as the service ensures the utmost level of data security and anti-malware safeguards.

Select the format you desire for your Debt Deduction On Les (PDF, DOCX, RTF) and save the sample onto your device.

- Search for the document you require and examine it.

- Review the file you searched and preview it or evaluate the form description to confirm it meets your needs. If it doesn’t, utilize the search feature to find the appropriate one. Click Buy Now once you have found the template you seek.

- Register and Log In.

- Select the pricing scheme that fits you and set up an account. Use PayPal or a credit card for a swift transaction. If you already possess an account, Log In and check your subscription to continue.

- Acquire the fillable template.

Form popularity

FAQ

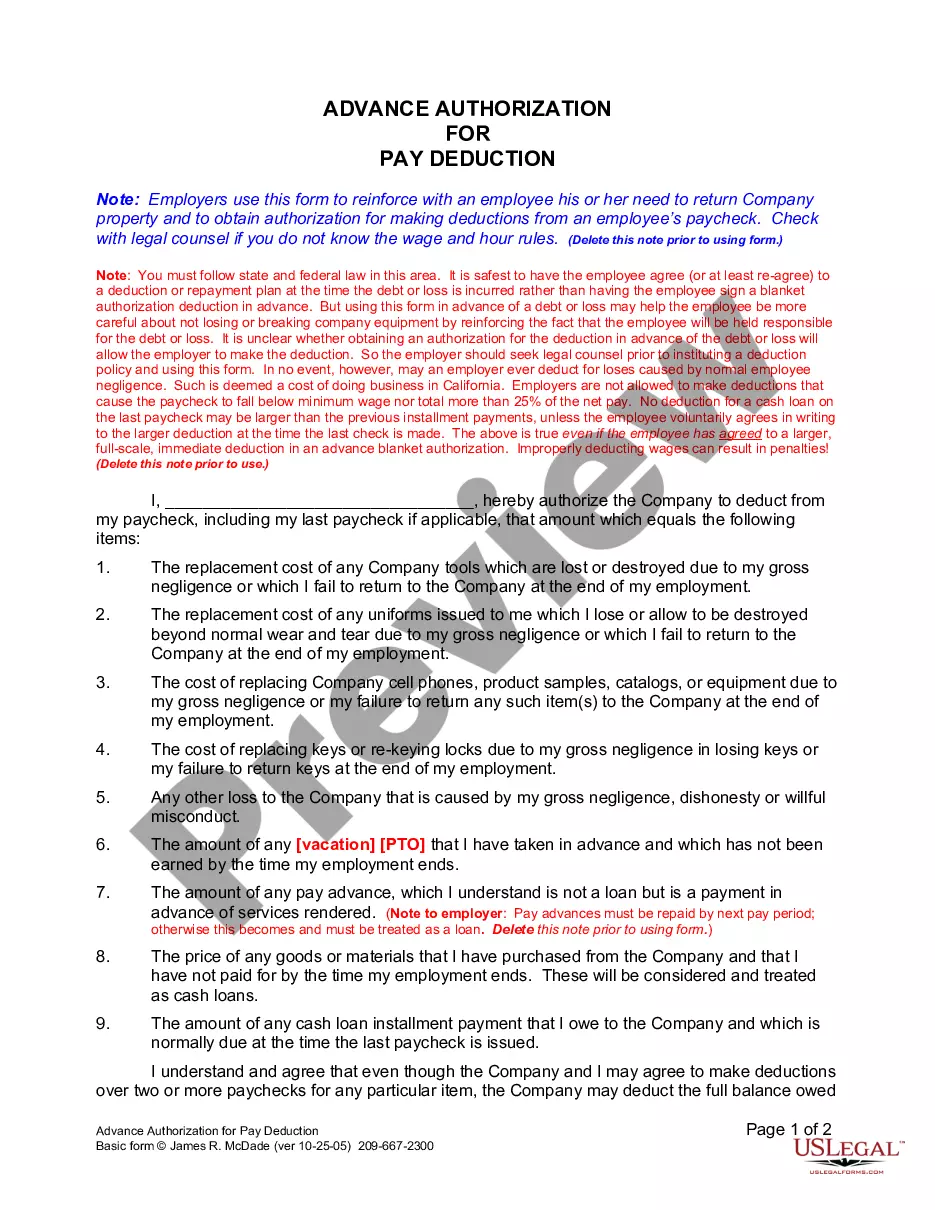

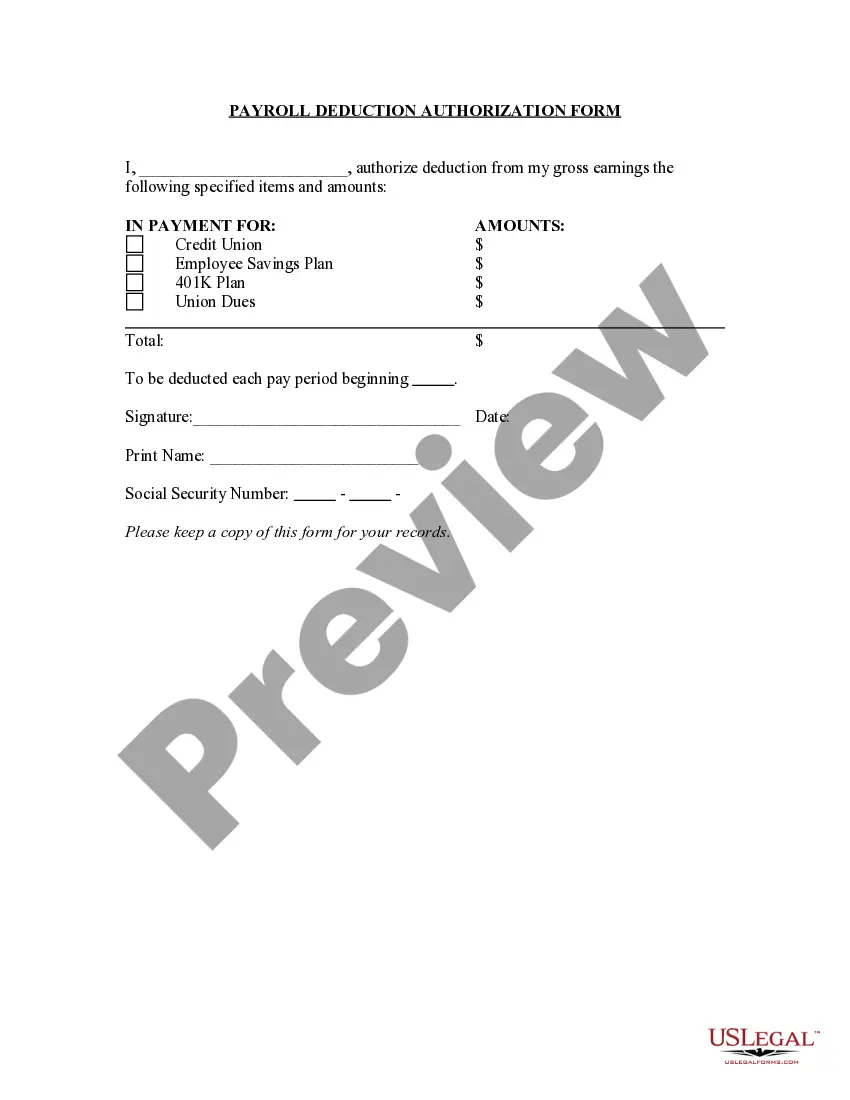

What does the term ?Advance Debt? on my LES means? That is our military pay system's way of notifying the member that they've been overpaid. This usually occurs during a PCS or a deployment, and the overpayment occurred in a previous months pay cycle.

Various types of government debts are listed on your LES. These may include debt from an overpayment, advance pay or advance Basic Allowance for Housing loan.

Support/Comm Debt: This is usually court-ordered child support payments being taken directly from the service member's pay and paid by the Defense Finance and Accounting Service (DFAS).

Because your previous payroll office or previous agency sent your Individual Retirement Record to the Office of Personnel Management (OPM), Block 19 ? Cumulative Retirement Total on your first LES will show only your retirement contributions for the time you are in your new payroll office or agency.

What does the term ?Advance Debt? on my LES means? That is our military pay system's way of notifying the member that they've been overpaid. This usually occurs during a PCS or a deployment, and the overpayment occurred in a previous months pay cycle.