Notice Of Default Form Withdrawal

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

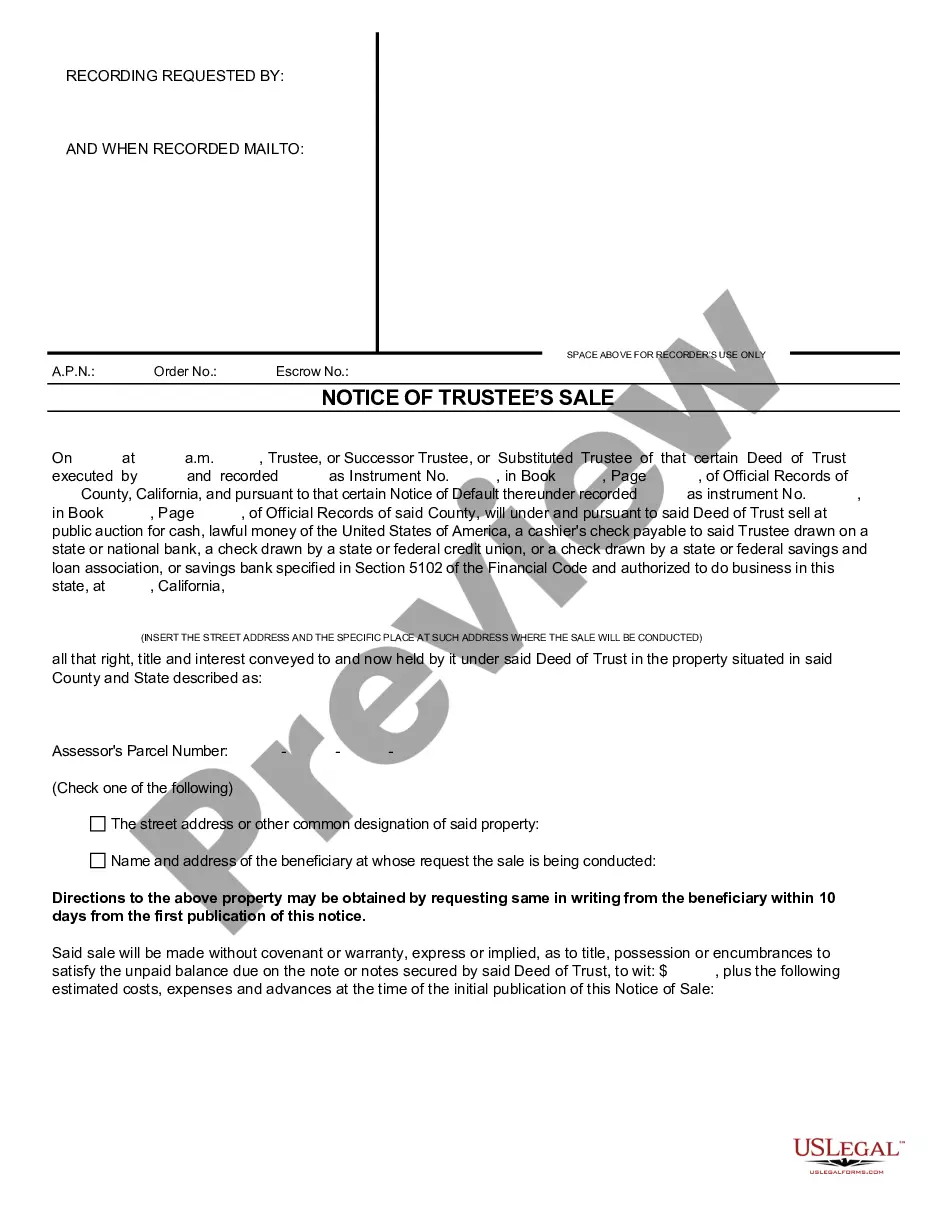

How to fill out California Notice Of Default And Election To Sell Under Deed Of Trust?

Acquiring legal document examples that comply with federal and local laws is crucial, and the web provides countless alternatives to choose from.

However, why squander time searching for the appropriate Notice Of Default Form Withdrawal example online when the US Legal Forms digital library has already compiled such documents in one location.

US Legal Forms is the largest online legal repository with over 85,000 editable templates created by attorneys for any professional and personal circumstances.

Review the template using the Preview feature or the text description to ensure it satisfies your requirements.

- They are simple to navigate with all documents sorted by state and intended use.

- Our specialists stay updated with legislative changes, ensuring your form is current and compliant when acquiring a Notice Of Default Form Withdrawal from our platform.

- Obtaining a Notice Of Default Form Withdrawal is straightforward and quick for both existing and new users.

- If you have an existing account with an active subscription, Log In and download the document example you need in the appropriate format.

- If you are new to our site, follow the steps outlined below.

Form popularity

FAQ

They have also taken steps to remove all medical collections under $500. This last step went into effect on April 11, 2023, and with this change, it's estimated that roughly half of those with medical debt on their reports will have it removed from their credit history.

The Truth in Lending Act (TILA) protects you against inaccurate and unfair credit billing and credit card practices. It requires lenders to provide you with loan cost information so that you can comparison shop for certain types of loans.

A summary of your loan details, which include your loan amount, the term of your loan, and your initial monthly payment.

Federal Legislative Activity in 2023 Amend Section 604(c) of the FCRA to address the treatment of pre-screening report requests. Section 604(c) governs the furnishing of reports in connection with credit or insurance transactions that are not initiated by the consumer. [1]

CLAIM: A new law passed by Congress ?allows you to permanently remove any negative debt? from your credit report that is over two years old. AP'S ASSESSMENT: False. The law referenced in the video to support that claim, the Fair Credit Reporting Act, has been around since 1970.

Effective July 1, 2022, paid medical collection debt is no longer included on U.S. consumer credit reports.

Under a new rule from the Federal Housing Finance Agency (FHFA), which took effect on May 1st, borrowers with lower credit ratings and less money for a down payment will qualify for better mortgage rates, while those with higher ratings will pay increased fees.

Technically, a loan estimate is only binding on the date it's issued. The lender has to give you the loan, with exactly the terms listed in the loan estimate, if on that day you take steps to accept the loan and lock your rate in.