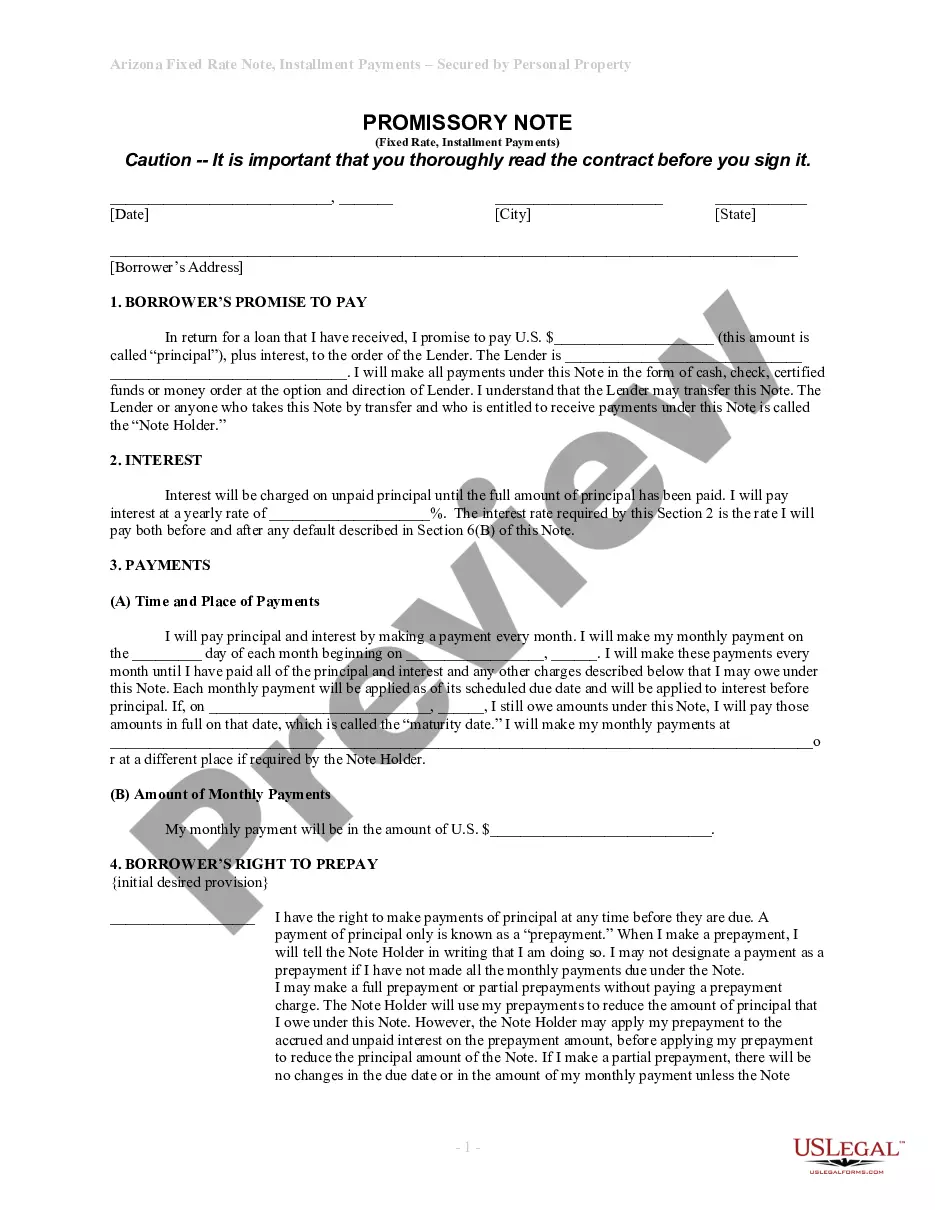

Arizona Promissory Note With Personal Guarantee

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Arizona Installments Fixed Rate Promissory Note Secured By Commercial Real Estate?

Red tape necessitates exactness and correctness.

If you don't manage completing documentation like Arizona Promissory Note With Personal Guarantee daily, it may lead to certain confusions.

Choosing the appropriate example from the beginning will guarantee that your document submission proceeds smoothly and avoids the inconveniences of re-submitting a file or starting the entire process from the beginning.

Locating the correct and up-to-date samples for your documents takes just a few minutes with an account at US Legal Forms. Eliminate the concerns of bureaucracy and enhance your efficiency with paperwork.

- Find the template using the search feature.

- Confirm the Arizona Promissory Note With Personal Guarantee you found is suitable for your state or region.

- Access the preview or review the details that provide specifics on the sample's use.

- If the outcome corresponds to your search, click the Buy Now button.

- Choose the right option from the proposed subscription plans.

- Log In to your account or sign up for a new one.

- Finalize the transaction using a credit card or PayPal payment method.

- Download the form in your preferred format.

Form popularity

FAQ

There is no legal requirement for a promissory note to be witnessed or notarized in Arizona. Still, the parties may decide to have the document certified by a notary public for protection in the event of a lawsuit.

At its most basic, a promissory note should include the following things:Date.Name of the lender and borrower.Loan amount.Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral?Payment amount and frequency.Payment due date.Whether the loan has a cosigner, and if so, who.

Generally, promissory notes do not need to be notarized. Typically, legally enforceable promissory notes must be signed by individuals and contain unconditional promises to pay specific amounts of money.

Personal Guarantee: Taking Responsibility A promissory note alone may not be enough to secure the loan your business needs. That's why your promissory note could include a personal guarantee. Since a promissory note is basically just an IOU, a lender will want some kind of collateral to secure the loan.

You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.