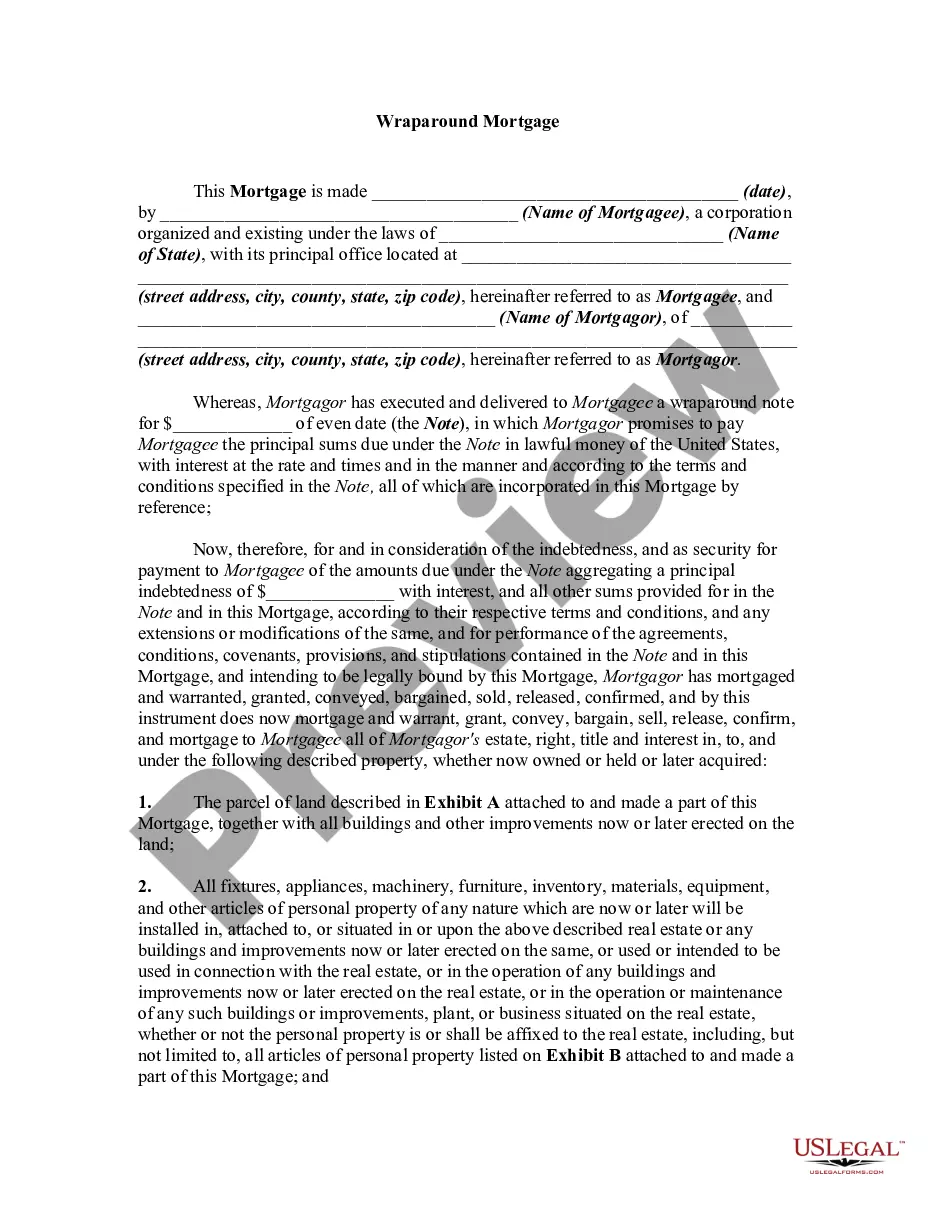

Wraparound Mortgage Due On Sale Clause

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Another common name for a wrap-around mortgage is an all-inclusive mortgage or AITD (All-Inclusive Trust Deed). This term reflects how the wrap-around financing encompasses the existing mortgage plus any new financing. Such terminology may vary regionally, but the concept remains the same. Familiarizing yourself with these terms can help in discussions with sellers and can clarify your options when exploring real estate financing.

The primary risks associated with a wrap-around mortgage include potential legal issues and the due on sale clause triggering. If the original mortgage lender becomes aware of the new agreement, they may demand immediate repayment. Additionally, if the seller defaults, you could lose your investment and face eviction. Therefore, it's essential to conduct thorough due diligence and perhaps use resources like USLegalForms to draft solid agreements that mitigate these risks.

Yes, a wrap-around mortgage often includes a due on sale clause, which means the seller’s existing mortgage can become due if they sell the property. This clause protects the lender by ensuring that all obligations are settled before the transfer of ownership. Understanding the implications of this clause is crucial for both buyers and sellers who engage in wrap-around mortgages. As a buyer, it is important to be prepared for this possibility when negotiating terms.

Banks typically do not offer wrap-around mortgages directly, as these are more common in private transactions. However, you can still use this financing method when purchasing a property. In these cases, the seller holds the mortgage, and you make payments to them. This arrangement can facilitate deals that traditional banks may not support, especially in niche markets.

around contract for deed is a financing method where the seller retains legal title to the property while allowing the buyer to occupy it. In this arrangement, the buyer makes payments directly to the seller, who continues paying the original mortgage. This type of contract can be beneficial for buyers facing challenges with traditional financing. Be sure to consider the implications of a wraparound mortgage due on sale clause when entering into such agreements.

around mortgage works by allowing the seller to provide financing for the buyer, who makes monthly payments on the new mortgage. The seller continues to make payments on the original mortgage, and the difference in the two amounts can be profit for the seller. This arrangement simplifies the buying process, especially when traditional financing options are limited. Remember, understanding the wraparound mortgage due on sale clause is vital, as it can impact how the transaction is structured.

In a wrap-around mortgage, the original borrower remains liable for the underlying mortgage, while the new buyer is responsible for the wrap-around payments. This structure allows you to enjoy the benefits of ownership without taking over the existing mortgage directly. However, it's crucial to understand that if the new buyer defaults, the original borrower could face significant financial repercussions. Therefore, it's important to have clear agreements in place regarding liability.

Navigating around a due-on-sale clause can be tricky, but there are a few strategies you can consider. One option is to negotiate directly with your lender, as some may be willing to allow for a wrap-around mortgage under certain conditions. Additionally, consulting a legal expert or using platforms like US Legal Forms can provide valuable guidance on your options. Being informed and proactive can help you find a solution that meets your needs.

The acceleration clause, commonly found in many mortgage agreements, typically limits the ability to use wraparound mortgages. This clause gives lenders the right to demand full repayment if the property changes ownership. It's important to identify such clauses in your mortgage documents. Understanding these legal stipulations can help you explore alternative financing options that comply with your current mortgage.

In a wrap-around mortgage, the seller typically retains the title to the property while the buyer occupies it. The buyer makes payments to the seller based on the wraparound mortgage agreement. The title remains with the seller until the buyer fulfills their obligations, which allows for a smoother transaction process. This setup can streamline the transfer and maintain clarity regarding ownership.