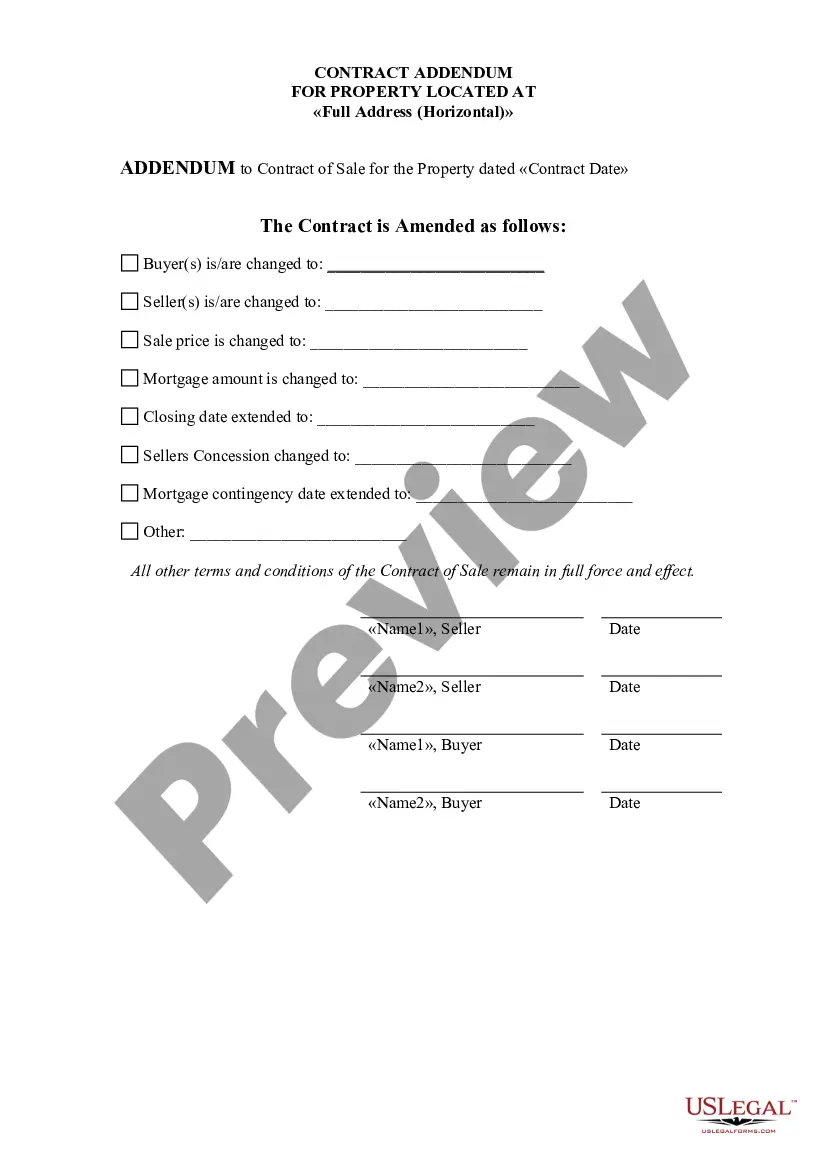

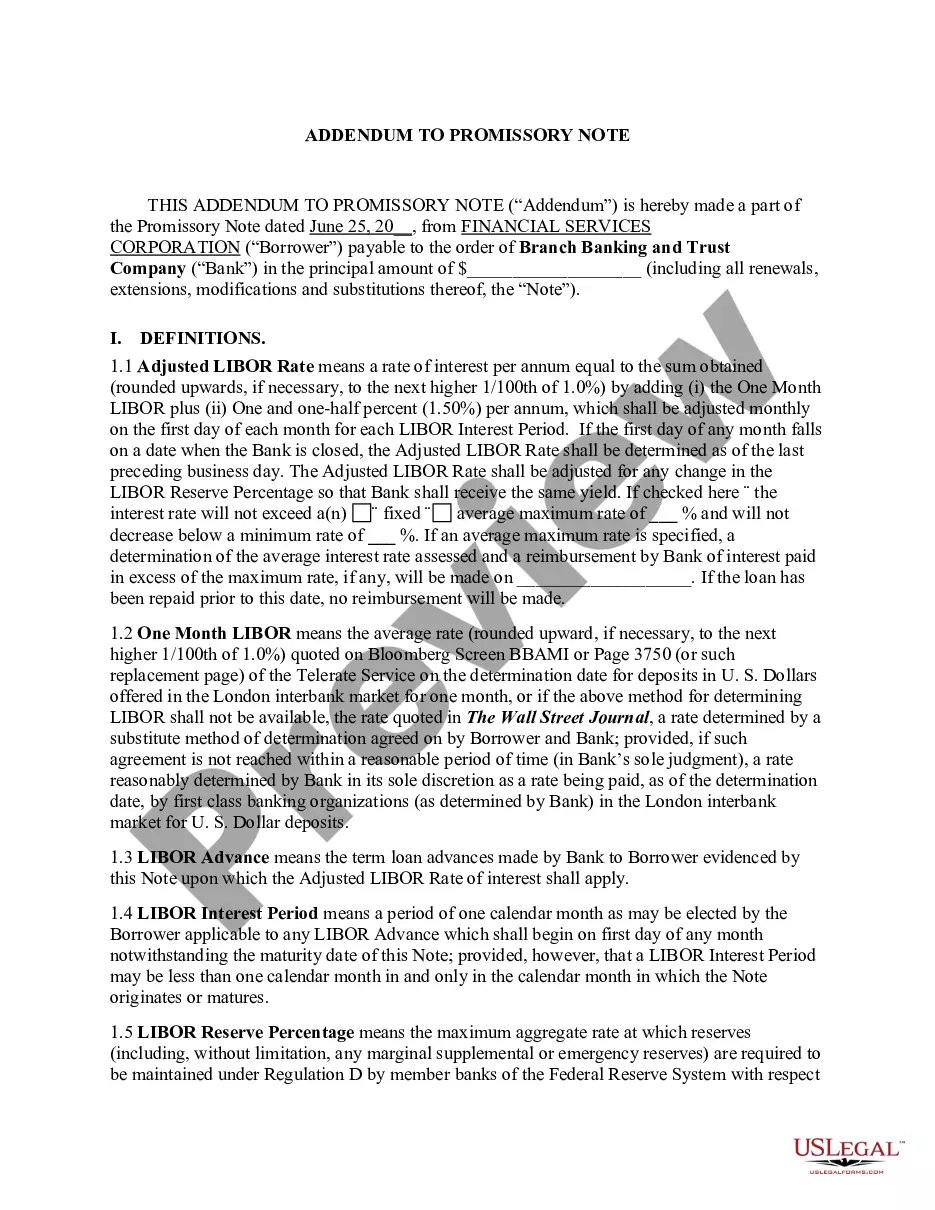

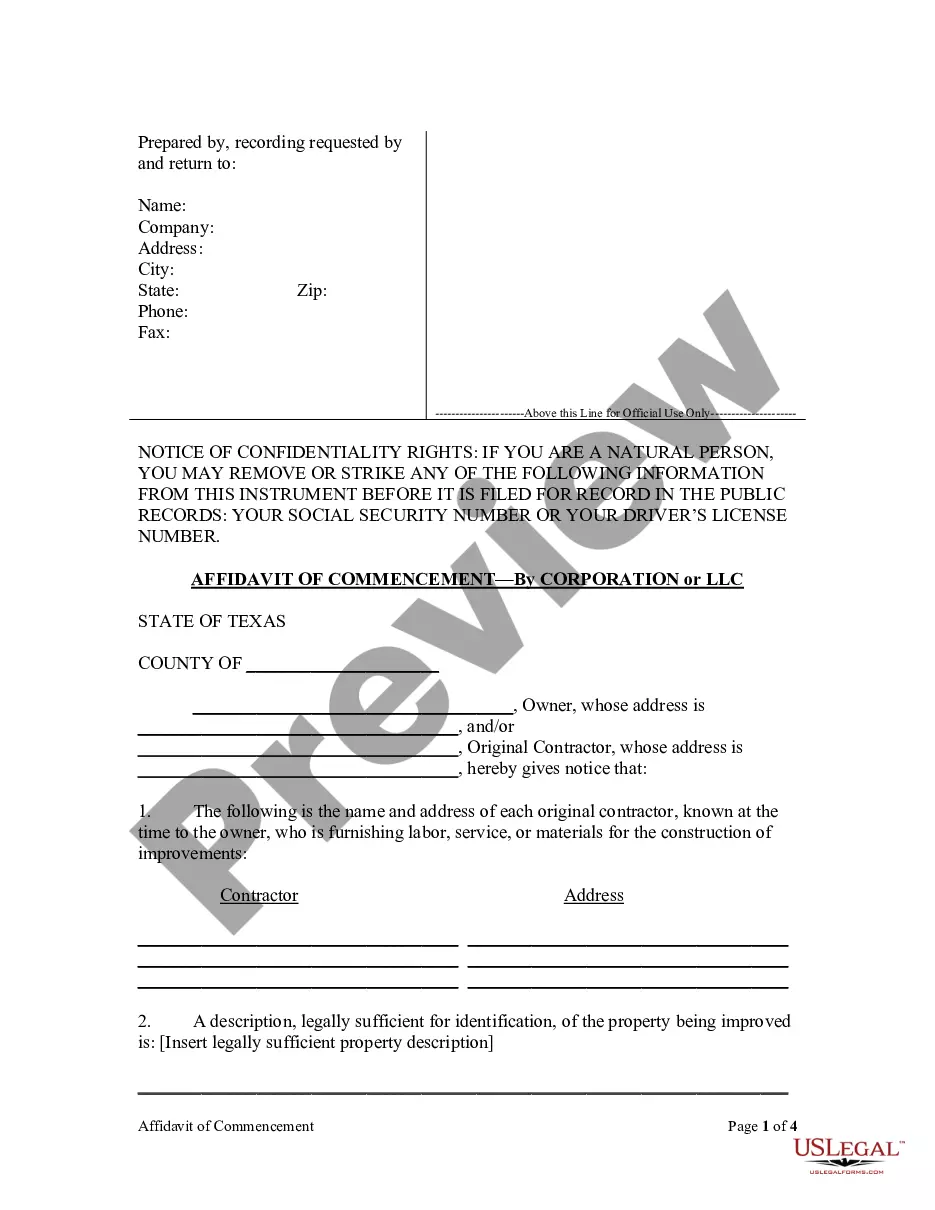

Security Instrument Addendum

Understanding this form

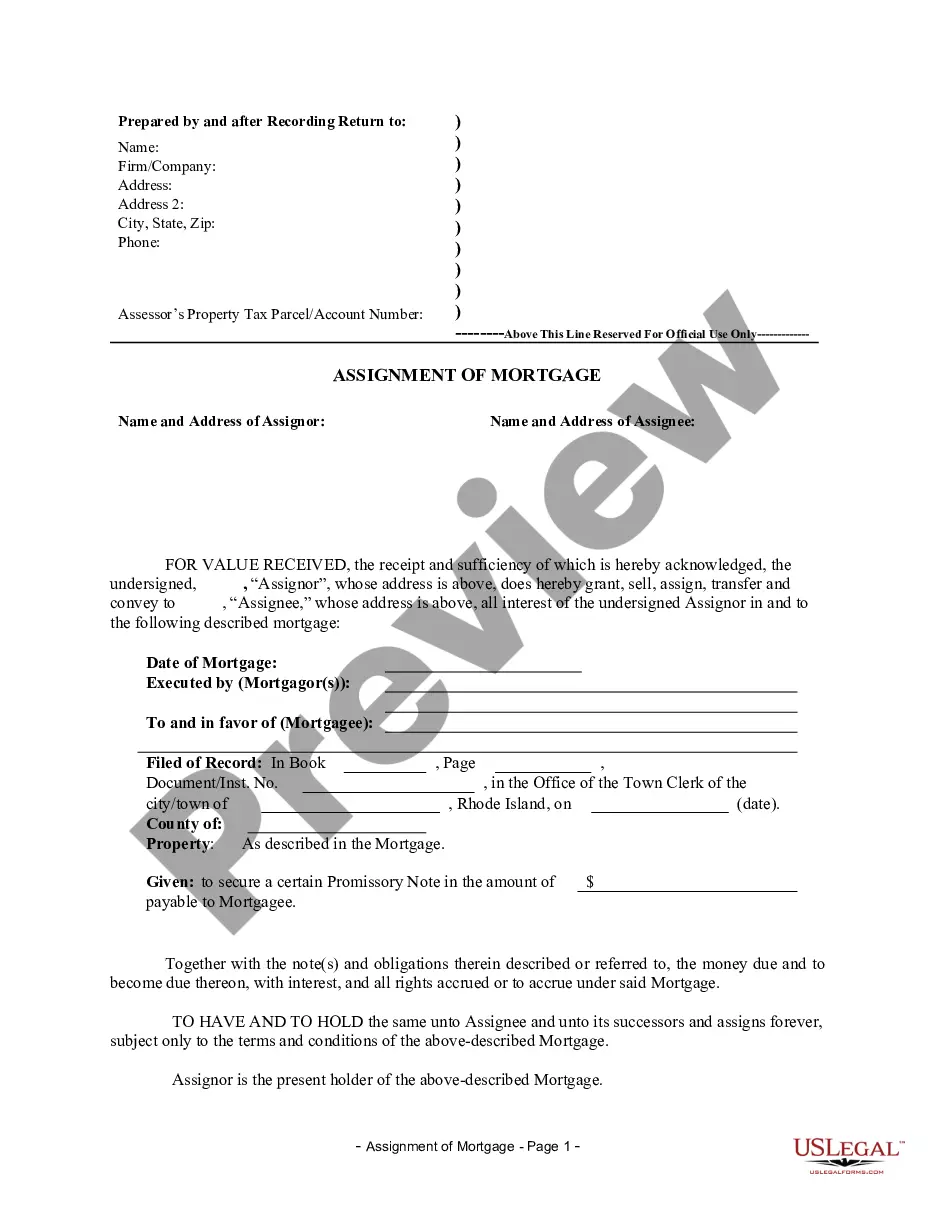

The Security Instrument Addendum is a legal document designed to establish a valid first lien on a mortgaged property in conjunction with a mortgage note. This form is essential for securing loans through different types of property agreements, including mortgages, deeds of trust, and security deeds. It serves as an important addendum that clarifies the terms applicable to the underlying security instrument, offering protection to lenders and ensuring compliance with local filing requirements.

Key parts of this document

- Parties involved: Identifies the lender and borrower.

- Property description: Specifies the mortgaged property being secured.

- Loan terms: Outlines terms of the mortgage note, including payment schedules.

- Legal compliance: Ensures conformance with local jurisdiction requirements.

- Signature fields: Designates areas for each party's signature and date.

Situations where this form applies

This form should be used when entering into a mortgage arrangement where a property is being used as collateral. It is applicable when additional terms need to be attached to the original security instrument or when the local jurisdiction requires specific disclosures or provisions to be included. This form is also relevant during refinancing, where existing mortgage terms may need revision or clarification.

Who can use this document

- Lenders seeking to secure loans with real estate.

- Borrowers entering into mortgage agreements.

- Real estate agents and brokers involved in property transactions.

- Attorneys assisting clients with mortgage documentation.

Instructions for completing this form

- Identify the parties: Clearly state the names and addresses of the lender and borrower.

- Specify the property: Provide a detailed description of the mortgaged property, including its address.

- Enter the loan terms: Include key details such as the loan amount, interest rate, and repayment schedule.

- Review local requirements: Ensure that the form meets any additional conditions set by your local jurisdiction.

- Collect signatures: Have both parties sign and date the document to validate the agreement.

Is notarization required?

This form does not typically require notarization unless specified by local law. Always check your specific jurisdictionâs requirements for any additional legal formalities.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Not accurately describing the mortgaged property.

- Failing to include required disclosures specific to the local jurisdiction.

- Omitting signatures or dates from the form.

- Using outdated versions of the form that do not comply with current laws.

Benefits of using this form online

- Convenient access: Download and complete forms from anywhere, at any time.

- Editability: Easily customize the form to reflect specific terms and conditions.

- Reliable legal templates: Form templates are drafted by licensed attorneys, ensuring legal compliance.

Key takeaways

- The Security Instrument Addendum is critical for securing loans with real estate assets.

- Ensure that the form meets your local jurisdiction's legal requirements.

- Accurate completion of the form helps prevent common legal issues and misunderstandings.

Looking for another form?

Form popularity

FAQ

A deed of trust involves three parties: a lender, a borrower, and a trustee. The lender gives the borrower money. In exchange, the borrower gives the lender one or more promissory notes. As security for the promissory notes, the borrower transfers a real property interest to a third-party trustee.

This document may be called the Security Instrument, Deed of Trust, or Mortgage. When you sign this document, you are giving the lender the right to take your property by foreclosure if you fail to pay your mortgage ing to the terms you've agreed to.

Who holds legal title when this security instrument is used? The borrower holds legal title to the property that secures the loan when a mortgage instrument is used.

This document may be called the Security Instrument, Deed of Trust, or Mortgage. When you sign this document, you are giving the lender the right to take your property by foreclosure if you fail to pay your mortgage ing to the terms you've agreed to.

1-4 Family Rider. A 1-4 Family Rider is typically required for multifamily investment properties with up to four units or two-to-four unit properties that are owner-occupied. This type of rider permits the lender to collect rent from the property if you default on the loan.

Trustee: This is the third party who will hold the legal title to the real property. Beneficiary: This is the lender.

Security instruments for regularly amortizing mortgages include the Fannie Mae/Freddie Mac Uniform Mortgages, Mortgage Deeds, Deeds of Trust, or Security Deeds for each of the jurisdictions from which we purchase conventional mortgages.

An example of a security instrument in real estate is a mortgage (or, in some states, a deed of trust), which a borrower uses to finance the purchase of a home. The lender holds the mortgage, giving them a security interest in the home that serves as collateral.