Validation Of Debt With 1099

Description

How to fill out Letter Requesting A Collection Agency To Validate A Debt That You Allegedly Owe A Creditor?

Creating legal paperwork from the ground up can frequently be daunting.

Some situations may require extensive research and significant financial investment.

If you're looking for a more efficient and cost-effective method of producing Validation Of Debt With 1099 or any other paperwork without unnecessary obstacles, US Legal Forms is readily available to you.

Our online repository of over 85,000 current legal forms encompasses nearly every aspect of your financial, legal, and personal affairs. With just a few clicks, you can promptly obtain state- and county-compliant documents meticulously prepared for you by our legal professionals.

Ensure that the form you choose complies with the laws and regulations of your state and county. Select the most suitable subscription option to acquire the Validation Of Debt With 1099. Download the document, then complete, certify, and print it. US Legal Forms enjoys an impeccable reputation and more than 25 years of expertise. Join us now and simplify and streamline your document preparation process!

- Utilize our platform anytime you require trusted and dependable services through which you can easily locate and obtain the Validation Of Debt With 1099.

- If you are familiar with our site and have previously registered an account, just Log In to your account, choose the template, and download it or re-download it anytime later from the My documents section.

- Not registered yet? No problem. It only takes a few minutes to create an account and access the library.

- But before you rush to download Validation Of Debt With 1099, follow these guidelines.

- Review the form preview and descriptions to confirm you have the correct document.

Form popularity

FAQ

When settling a debt for less than what you owe, you might need to issue a 1099 if the forgiven amount is $600 or greater. The IRS sees this forgiven debt as taxable income, making it essential to keep accurate records. As you navigate the validation of debt with 1099 forms, consider using US Legal Forms to find templates and support for your settlement documentation. This platform can ease the process and ensure you stay compliant.

Yes, you may need to issue a 1099 for a bad debt if it meets specific criteria. If you have canceled or forgiven a debt of $600 or more, the IRS typically requires you to report this on a 1099 form. Thus, if you deal with the validation of debt with 1099 forms, ensuring compliance can save you from potential tax issues. Additionally, it helps maintain clear records for both you and the IRS.

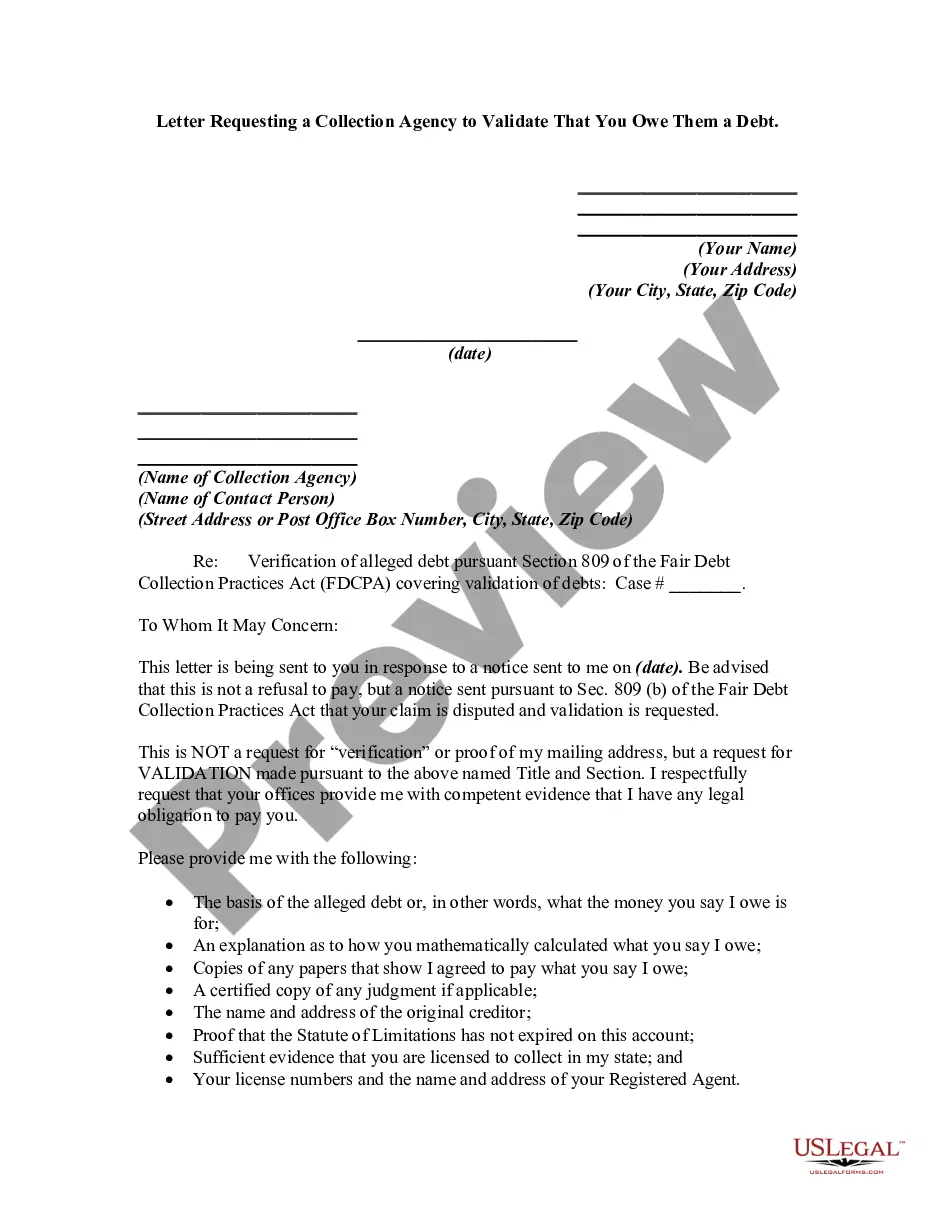

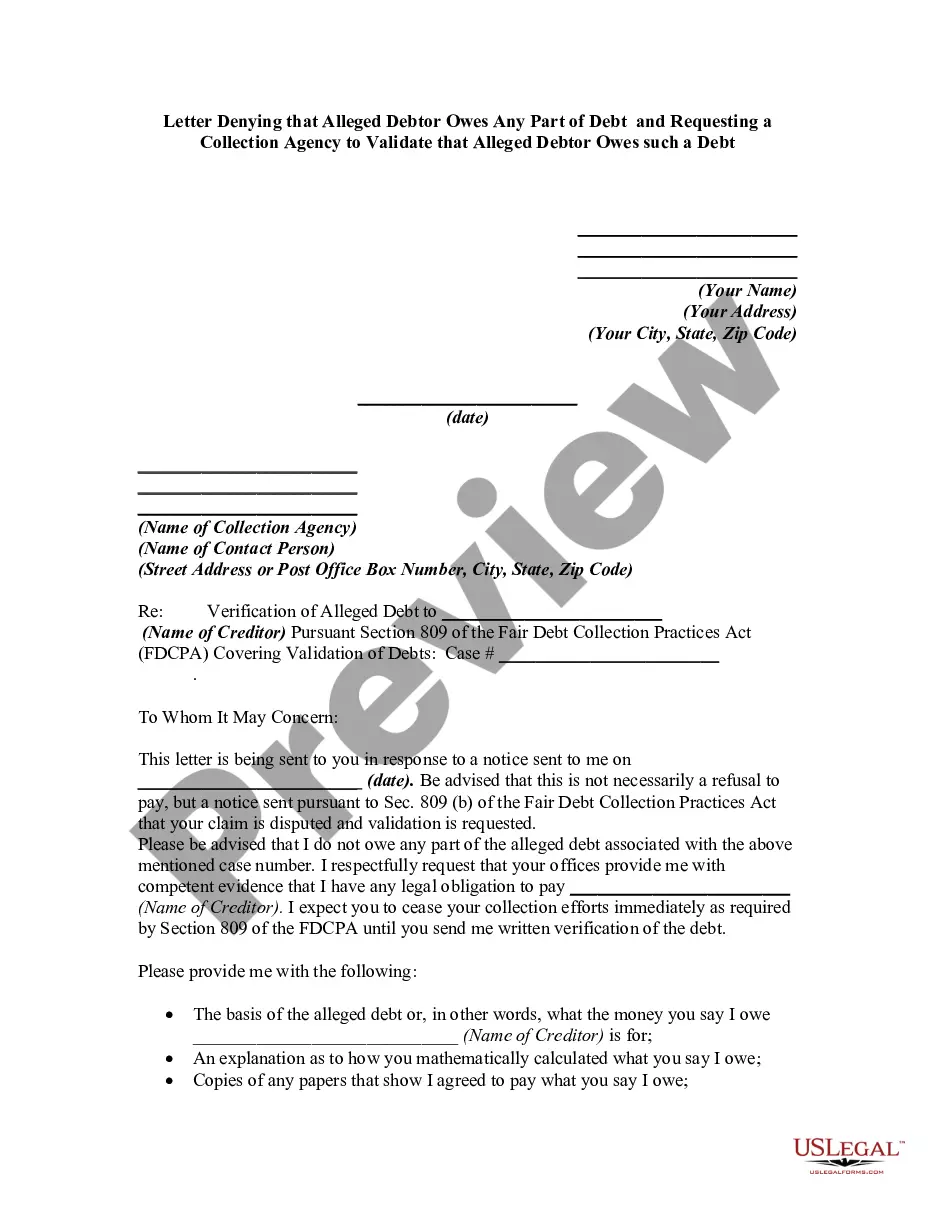

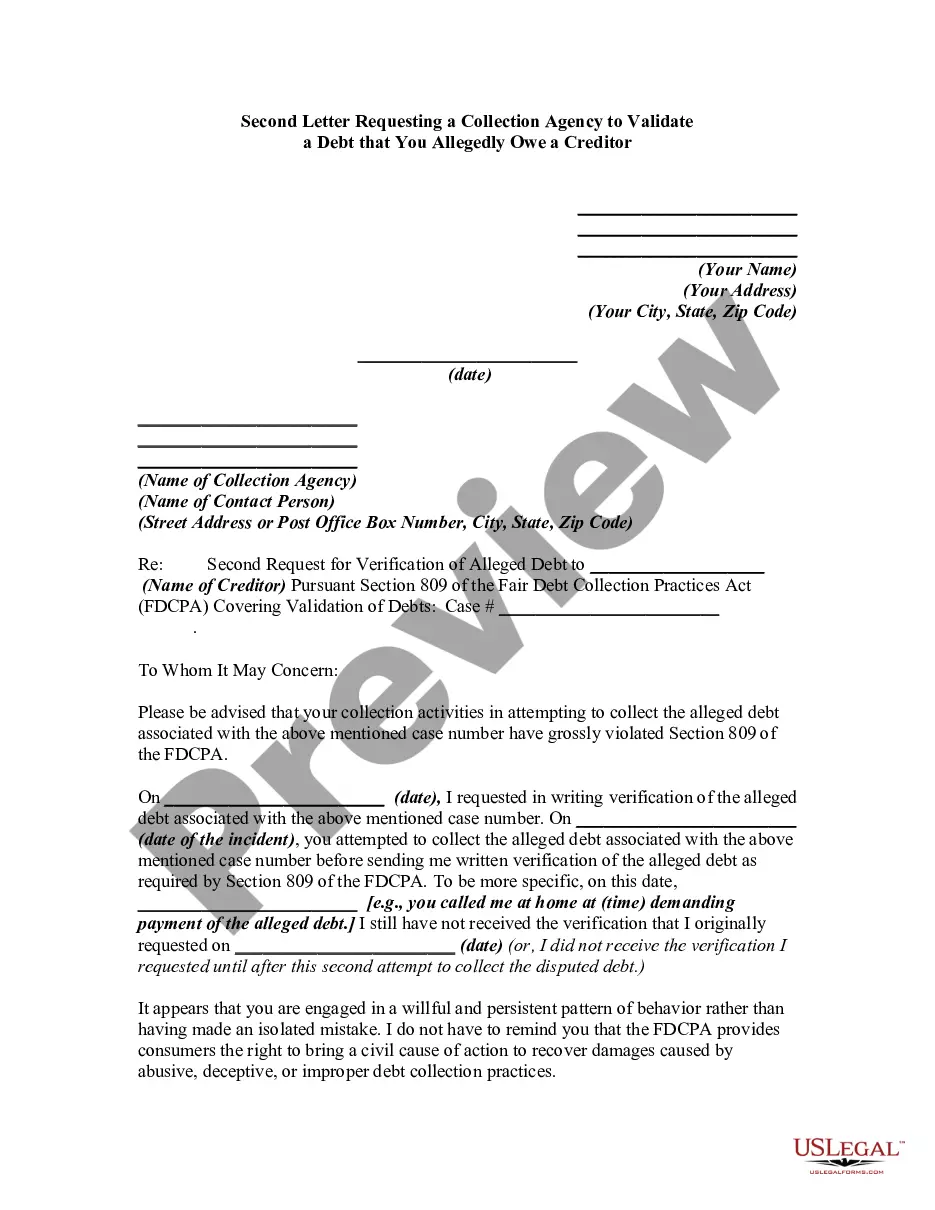

Validation of debt under the Fair Debt Collection Practices Act (FDCPA) means that a consumer has the right to request verification of the debt from the collector. This includes the amount of the debt and the name of the creditor. If you are seeking validation of debt with 1099 forms, it is essential to ensure that any debt claimed aligns with your records. Understanding your rights can help you manage debt more effectively.

Yes, you may receive a 1099 form if your debt is settled for less than what you owe, typically Form 1099-C. This is issued by the creditor when they cancel part of your debt. Smoothly handling the validation of debt with 1099 can help you comprehend your financial position and prepare your taxes accordingly.

The 1099 form specifically used for the forgiveness of debt is the Form 1099-C. This form provides necessary details about the amount of debt forgiven and can impact your taxable income. Knowing how to navigate the validation of debt with 1099 will support you in understanding your tax obligations.

To request validation of a debt, send a written request to the creditor within 30 days of being notified of the debt. Be sure to include your account information and state your desire for them to validate the debt. Properly documenting this interaction helps protect your rights and aligns with practices around validation of debt with 1099.

When settling a debt for less than the full amount owed, creditors typically issue Form 1099-A, Acquisition or Abandonment of Secured Property. This form is crucial for reporting the amount of debt canceled during the settlement. Being informed about validation of debt with 1099 can help you manage your tax implications effectively.

Form 1099-C is used for reporting cancellation of debt. When a creditor forgives or cancels a debt of $600 or more, they must issue this form. It’s essential for you to understand how this impacts your taxes. The process of validation of debt with 1099 is important to ensure that the debt cancellation is legitimate.

C is the IRS form used to report the cancellation of a debt. When a creditor forgives or cancels a debt amount of $600 or more, this form helps in the validation of debt with 1099 by notifying the IRS about the forgiven amount. It is important to report this correctly, as it may result in taxable income for the borrower.

Generally, you do not issue a 1099 for bad debt since it represents a loss rather than a payment made. However, if the debt is canceled, you might report it using a 1099-C to document the discharge. This process is paramount to the validation of debt with 1099, ensuring that your records accurately reflect your financial situation.