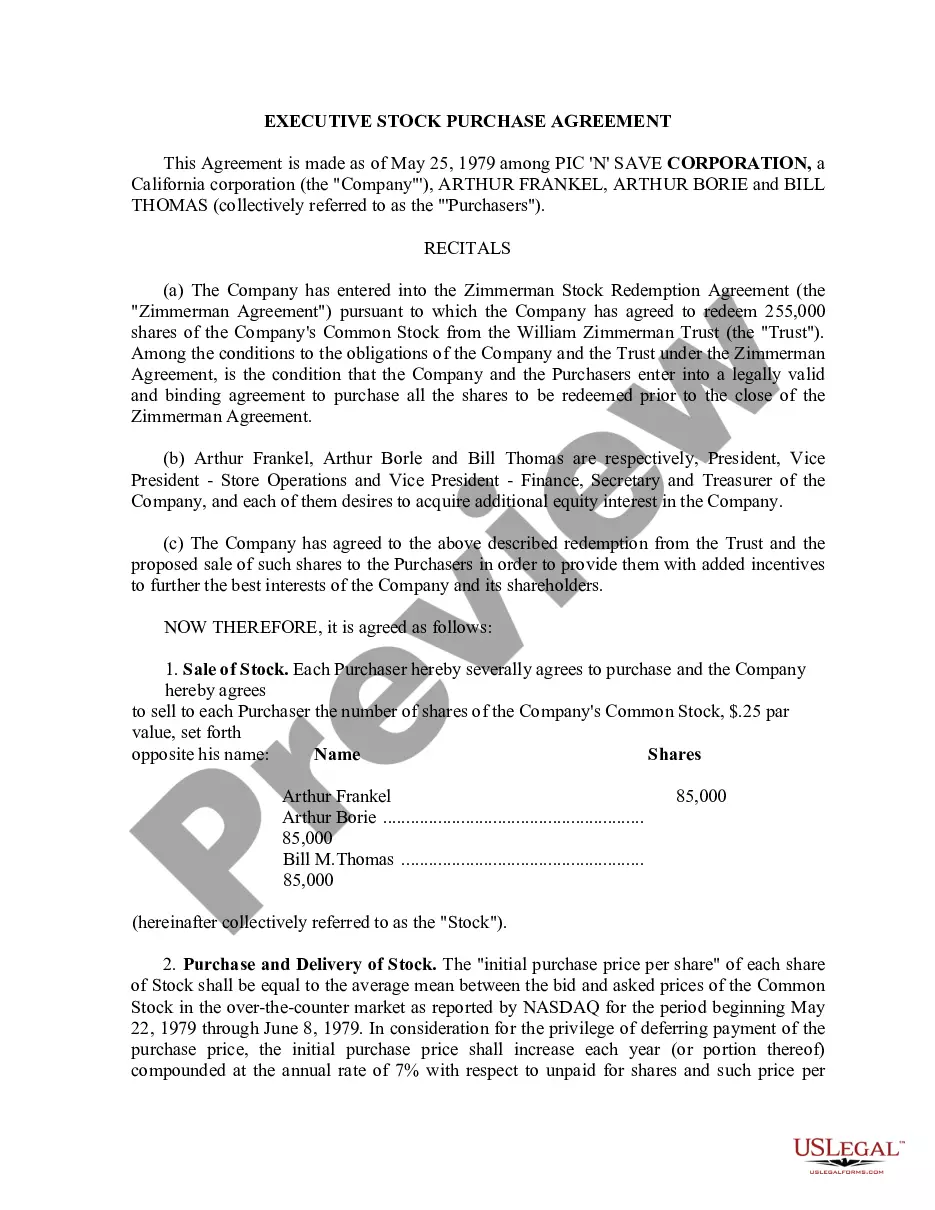

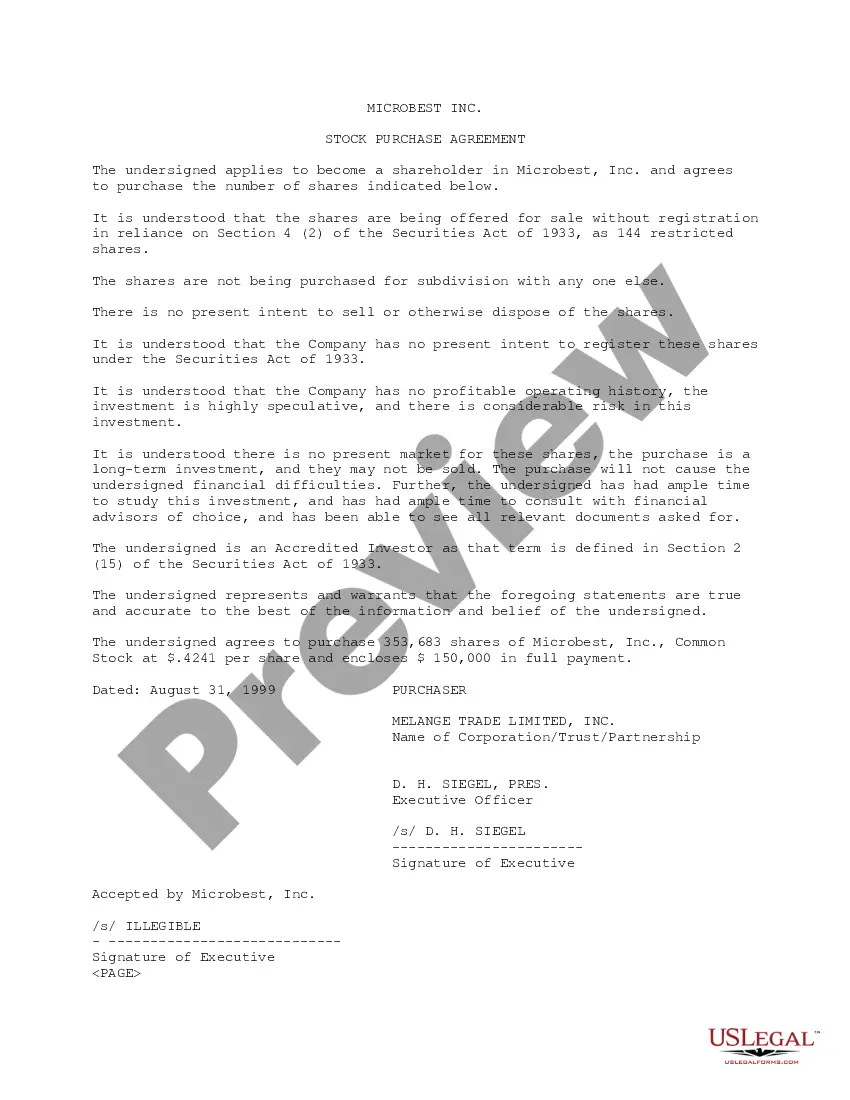

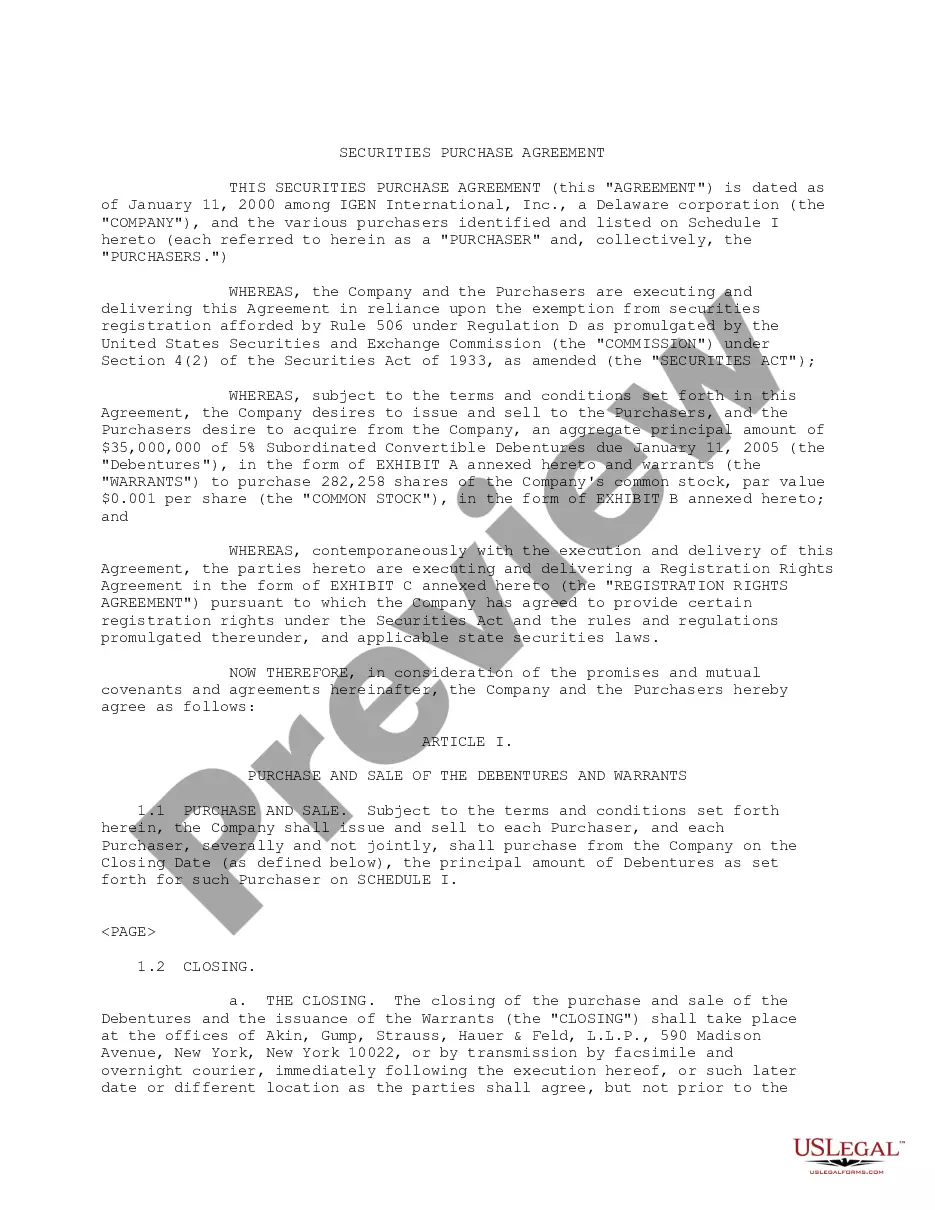

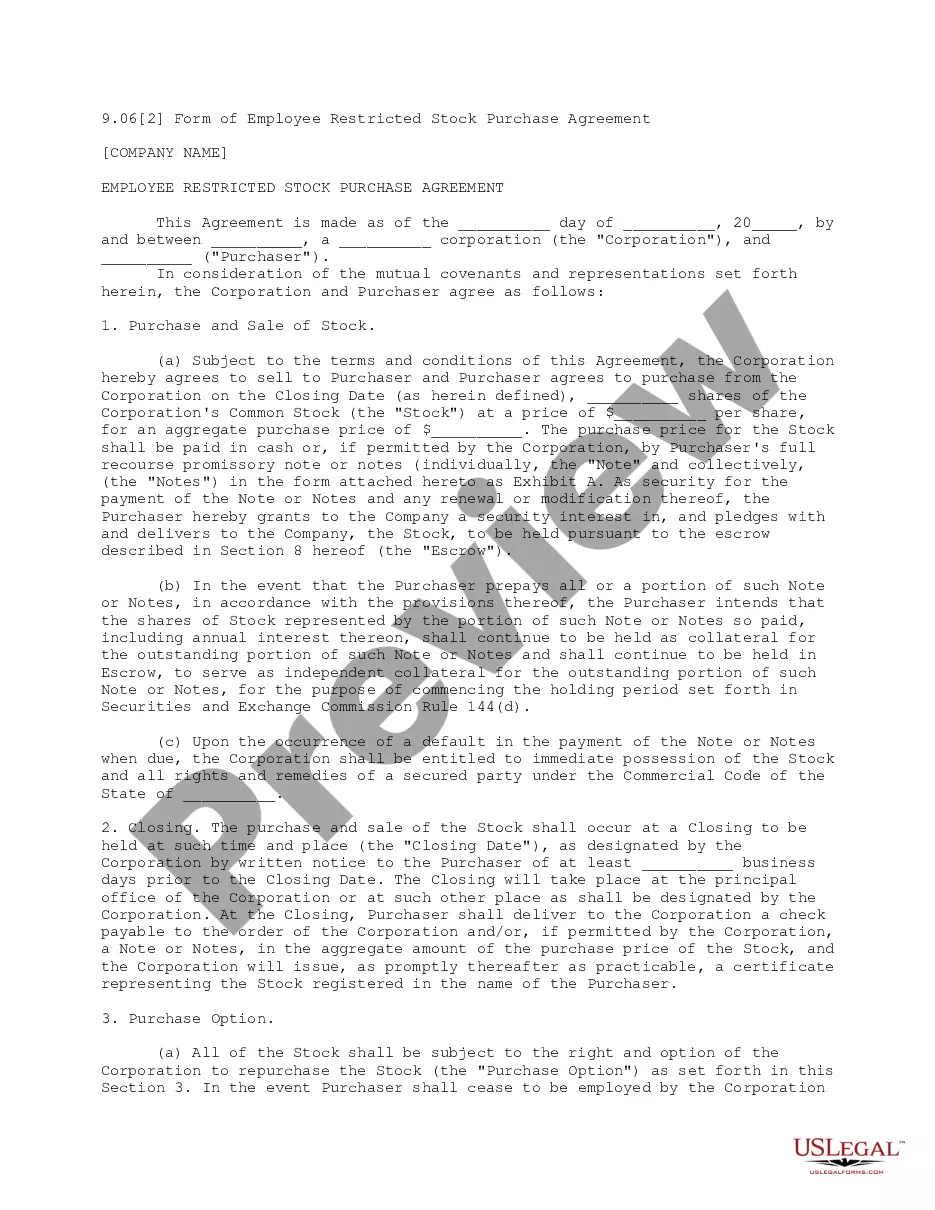

Restricted Stock Between Forfeiture

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Sample Restricted Stock Purchase Agreement Between Intermark, Inc. And Purchasers?

Finding a reliable location to obtain the most up-to-date and suitable legal templates is a significant part of navigating bureaucracy.

Selecting the appropriate legal documents requires precision and carefulness, which highlights the importance of sourcing Restricted Stock Between Forfeiture samples exclusively from trustworthy providers, such as US Legal Forms. An incorrect form can squander your time and hinder your current situation. With US Legal Forms, there’s little to be concerned about. You can access and review all the specifics regarding the document’s applicability and relevance to your situation and your locality.

Once you have the document on your device, you can modify it using the editor or print it and fill it out by hand. Eliminate the complications associated with your legal paperwork. Explore the extensive US Legal Forms catalog where you can discover legal templates, assess their relevance to your case, and download them instantly.

- Utilize the library navigation or search bar to find your document.

- Examine the form’s summary to verify if it aligns with the needs of your region.

- Check the form preview, if available, to ensure the template is indeed what you need.

- Return to the search to locate the right template if the Restricted Stock Between Forfeiture does not meet your requirements.

- If you are confident about the document’s relevance, proceed to download it.

- If you have clearance, click Log in to verify and gain access to your selected templates in My documents.

- If you do not possess an account yet, click Buy now to acquire the template.

- Choose the pricing option that meets your needs.

- Proceed to register to complete your transaction.

- Finalize your purchase by selecting a payment option (credit card or PayPal).

- Choose the file format for downloading the Restricted Stock Between Forfeiture.

Form popularity

FAQ

Income in the form of RSUs will typically be listed on the taxpayer's W-2 in the ?Other? category (Box 14). Taxpayers will simply translate the figure listed in Box 14 to their federal tax return and, if applicable, state tax return(s).

With restricted stock and RSUs, you almost always forfeit whatever stock has not vested at the time of your termination, unless your grant specifies another treatment or the company decides to continue or accelerate vesting.

Restricted stock is, by definition, a stock that has been granted to an executive that is nontransferable and subject to forfeiture under certain conditions, such as termination of employment or failure to meet either corporate or personal performance benchmarks.

Accounting for Restricted Stock/RSU Grants In general, future compensation expense related to restricted stock grants is based on the fair value of the stock on the grant date. The compensation expense is then recognized over the employees' service/vesting period.

Restricted stock awards are typically taxed using their value on the vest date, but you can opt to use the value on the grant date instead. Here's what to consider before you perform a so-called Section 83(b) election.