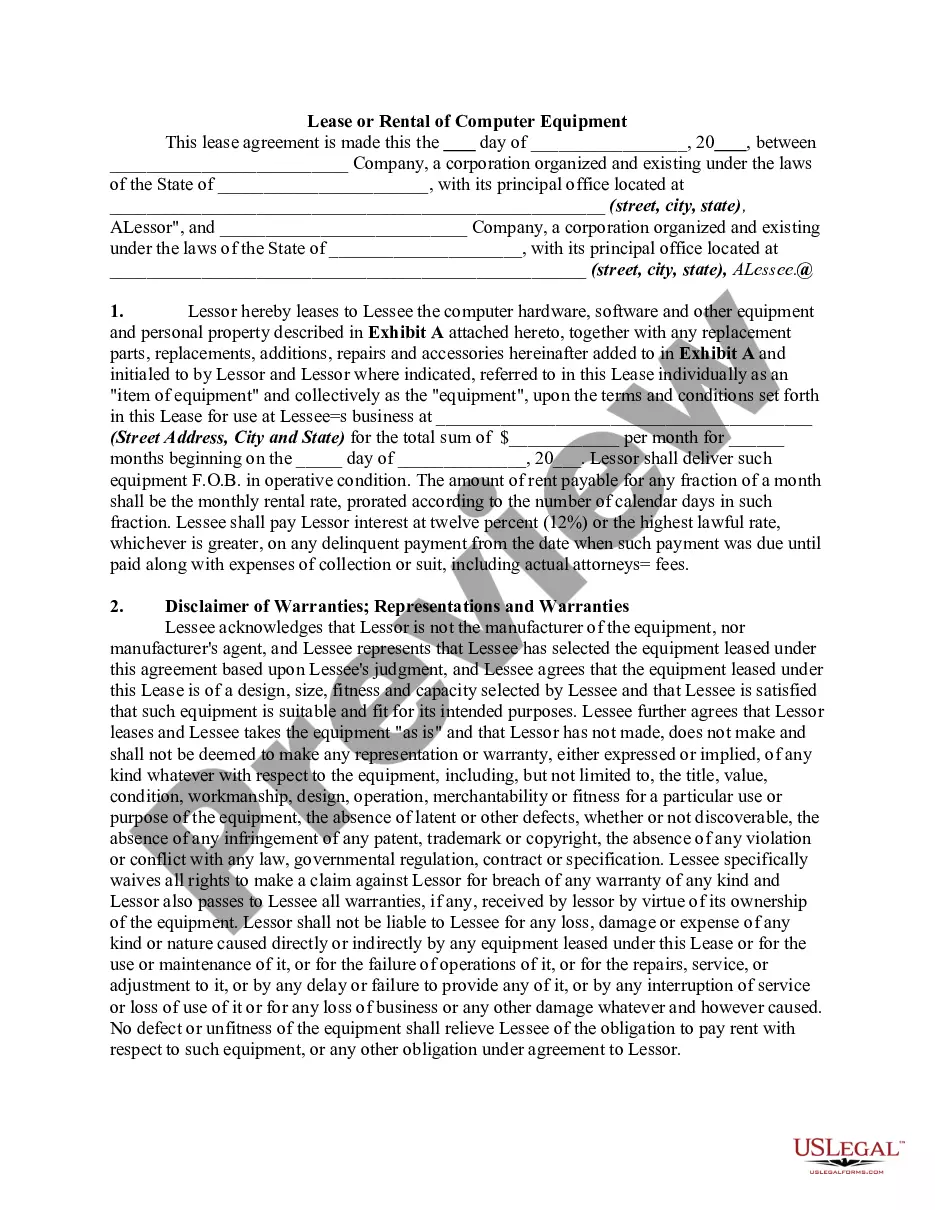

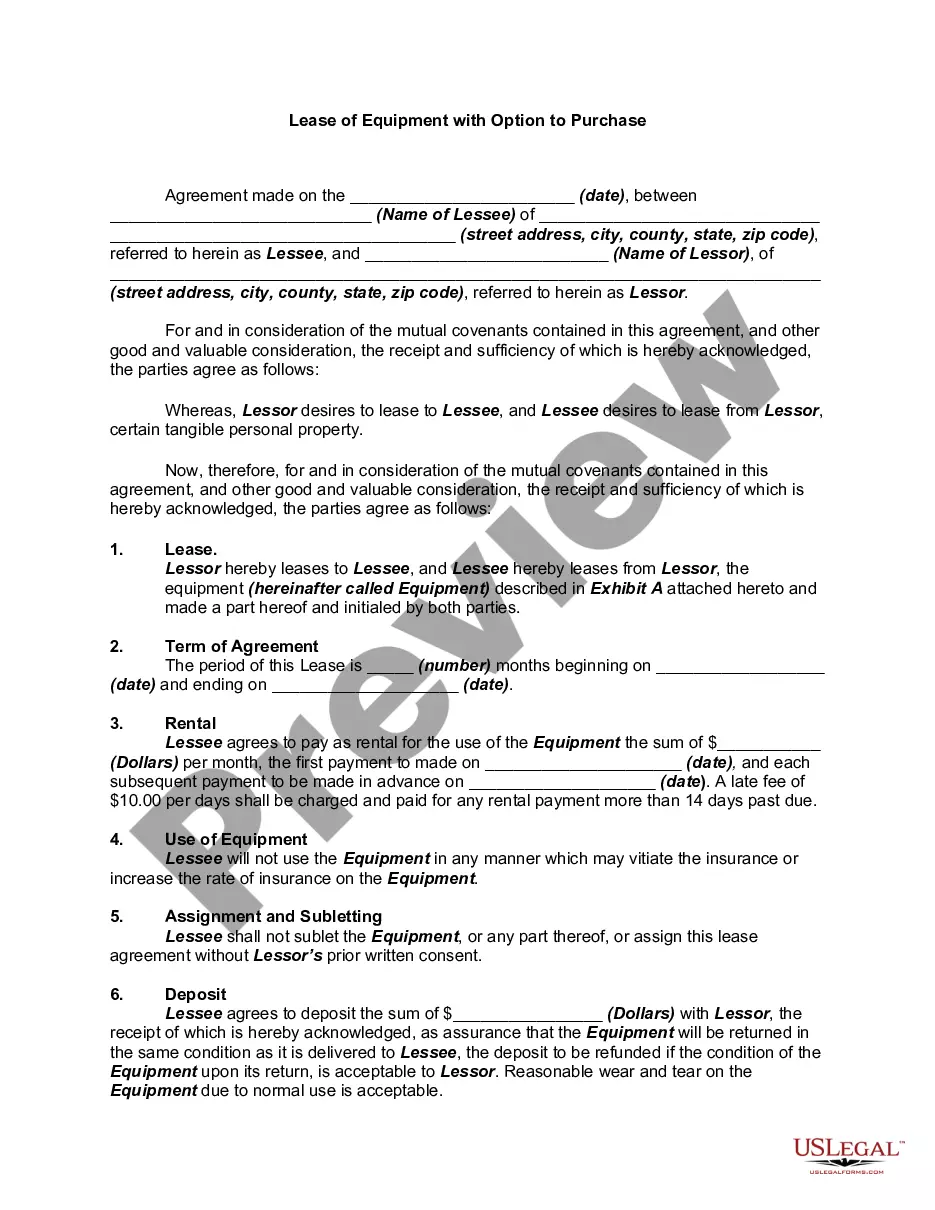

Equipment Lease All With Amortization Schedule

Description

How to fill out Lease Of Computer Equipment With Equipment Schedule And Option To Purchase?

The Equipment Lease All With Amortization Schedule presented on this site is a versatile legal template crafted by expert lawyers in accordance with federal and local statutes and guidelines.

For over 25 years, US Legal Forms has supplied individuals, companies, and legal experts with more than 85,000 authentic, state-specific forms for any business and personal requirement. It is the quickest, most direct, and most reliable method to acquire the documents you need, as the service ensures top-tier data security and anti-malware safeguards.

Register with US Legal Forms to have certified legal templates for all of life's circumstances at your fingertips.

- Search for the document you require and verify it.

- Browse through the file you sought and preview it or review the form description to ensure it meets your requirements. If it doesn't, use the search feature to locate the appropriate one. Click Buy Now once you've identified the template you need.

- Select and Log In.

- Choose the pricing plan that fits you and set up an account. Use PayPal or a credit card for a swift payment. If you already possess an account, Log In and verify your subscription to proceed.

- Acquire the editable template.

- Pick the format you desire for your Equipment Lease All With Amortization Schedule (PDF, Word, RTF) and save the document on your device.

- Fill out and sign the document.

- Print the template to fill it out manually. Alternatively, utilize an online multifunctional PDF editor to quickly and accurately complete and sign your form with an eSignature.

- Redownload your paperwork as needed.

- Reutilize the same document at any time. Access the My documents tab in your profile to retrieve any previously downloaded forms.

Form popularity

FAQ

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

A promissory note could become invalid if: It isn't signed by both parties. The note violates laws. One party tries to change the terms of the agreement without notifying the other party.

The Loan shall be evidenced and governed by a new promissory note (the ?New Note?) which amends and restates in its entirety, but does not extinguish, the Note. Anything to the contrary notwithstanding, if any inconsistency exists between the Loan Agreement and the New Note, the New Note shall control.

For example, you might agree to change the interest rate or the length of the loan. Always put promissory note changes in writing and have the borrower sign off on them, as oral changes can't be enforced in court. Changing a note without the borrower's written agreement makes a promissory note invalid.

In ance with the common law ?best evidence rule,? a party seeking to prove the disputed contents of the promissory note, such as the amount owed on said note, must produce the original document because it is the ?best evidence? of the terms of the note itself.

Once both the promissory note and the deed of trust are signed, the borrower and lender have evidence of this legally binding agreement. Your lender will typically provide you with a copy of the promissory note, along with several other documents, when you close on your home purchase.

If the borrower isn't meeting the original payment plan, the lender and borrow may need to rework the terms -- for example, lower payments, agree to interest-only payments, or lower the interest rate. This will allow you to modify your promissory note (IOU form).

Promissory notes have a statute of limitations. Depending on which U.S. state you live in, a written loan agreement may expire 3?15 years after creation.