Promissory Note Without Loan Agreement

Description

How to fill out Multistate Promissory Note - Unsecured - Signature Loan?

Utilizing legal templates that comply with federal and local laws is crucial, and the web provides numerous alternatives to select from.

However, what’s the use in spending time searching for the correct Promissory Note Without Loan Agreement example online if the US Legal Forms digital library already assembles such templates in one location.

US Legal Forms is the largest online legal repository featuring over 85,000 editable templates created by attorneys for any professional and personal scenarios.

Explore the template using the Preview feature or via the text description to confirm it meets your requirements.

- They are simple to navigate with all documents organized by state and intended purpose.

- Our specialists keep up with legal updates, ensuring your documentation is always current and compliant when obtaining a Promissory Note Without Loan Agreement from our platform.

- Acquiring a Promissory Note Without Loan Agreement is straightforward and rapid for both existing and new users.

- If you already possess an account with an active subscription, Log In and save the document sample you need in the appropriate format.

- If you're unfamiliar with our site, follow the steps below.

Form popularity

FAQ

A promissory note without loan agreement should include clear terms about repayment schedules, interest rates, and penalties for late payments. It is crucial that both parties understand their obligations and rights under the note. Furthermore, it must be signed by both the borrower and lender to be legally binding. For an organized approach, use uslegalforms to guide you through the process of creating a compliant promissory note.

Banks are not obligated to accept promissory notes without loan agreements as a form of payment or security. Acceptance often depends on the bank's policies, the borrower’s creditworthiness, and the specifics of the note. While some banks may consider promissory notes, others might need additional collateral or a formal loan agreement. Always check with your bank to understand their requirements.

The main disadvantage of a promissory note without loan agreement is the lack of formal structure that typically comes with written contracts. This absence can lead to misunderstandings between parties regarding payment terms or interest rates. Additionally, if proper documentation is not maintained, enforcing the payment can become challenging. Consider using uslegalforms to create formal agreements that minimize risks.

Yes, a promissory note must be signed by both parties to be legally binding and enforceable. The signature is essential as it demonstrates the borrower’s commitment to repay the loan according to the terms outlined in the note. Without signatures, you risk creating ambiguity in your agreement, especially with a promissory note without loan agreement. Using USLegalForms can simplify the process, ensuring that all necessary signatures are gathered correctly.

If there is no promissory note, the terms of the loan may become unclear, leading to disputes between the borrower and lender. Without a written agreement, proving the details of the transaction becomes challenging, and enforcing repayment can be difficult. In situations where a promissory note without loan agreement exists, a lender may struggle to recover their funds. To avoid such complications, consider using USLegalForms to create a clear and enforceable document.

Promissory notes are versatile financial instruments that can be used in various situations, such as securing loans or establishing payment terms for goods and services. When you create a promissory note without a loan agreement, it can act as a formal record of a debt. This ensures transparency and serves as a legal document in case disputes arise. You can find helpful resources on US Legal Forms to tailor a note that fits your needs.

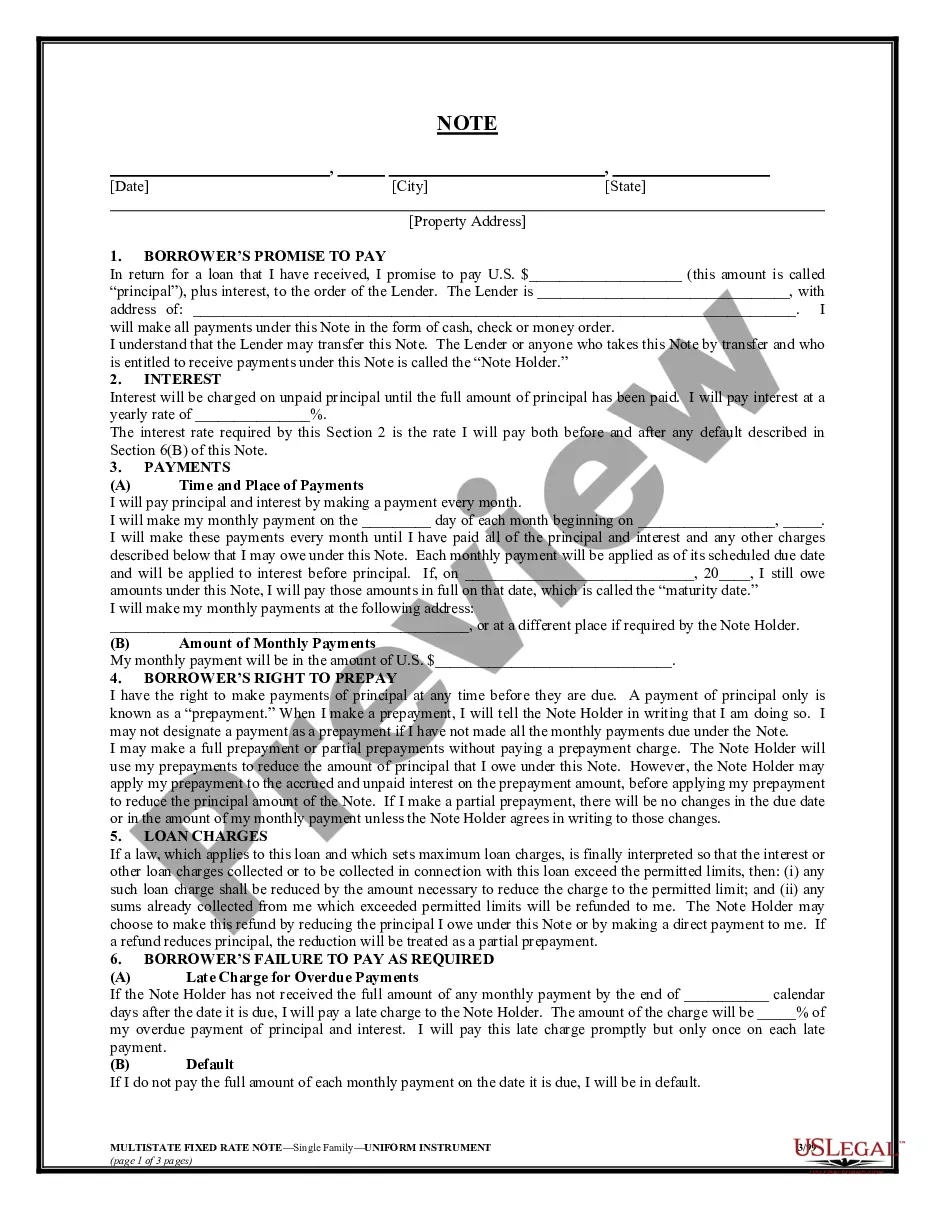

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.

A promissory note is generally sufficient if the amount of money is relatively small and there is a great deal of trust between the lender and the borrower (or debtor). In contrast, a loan agreement is more appropriate if the two parties do not know one another well and have substantial debt.

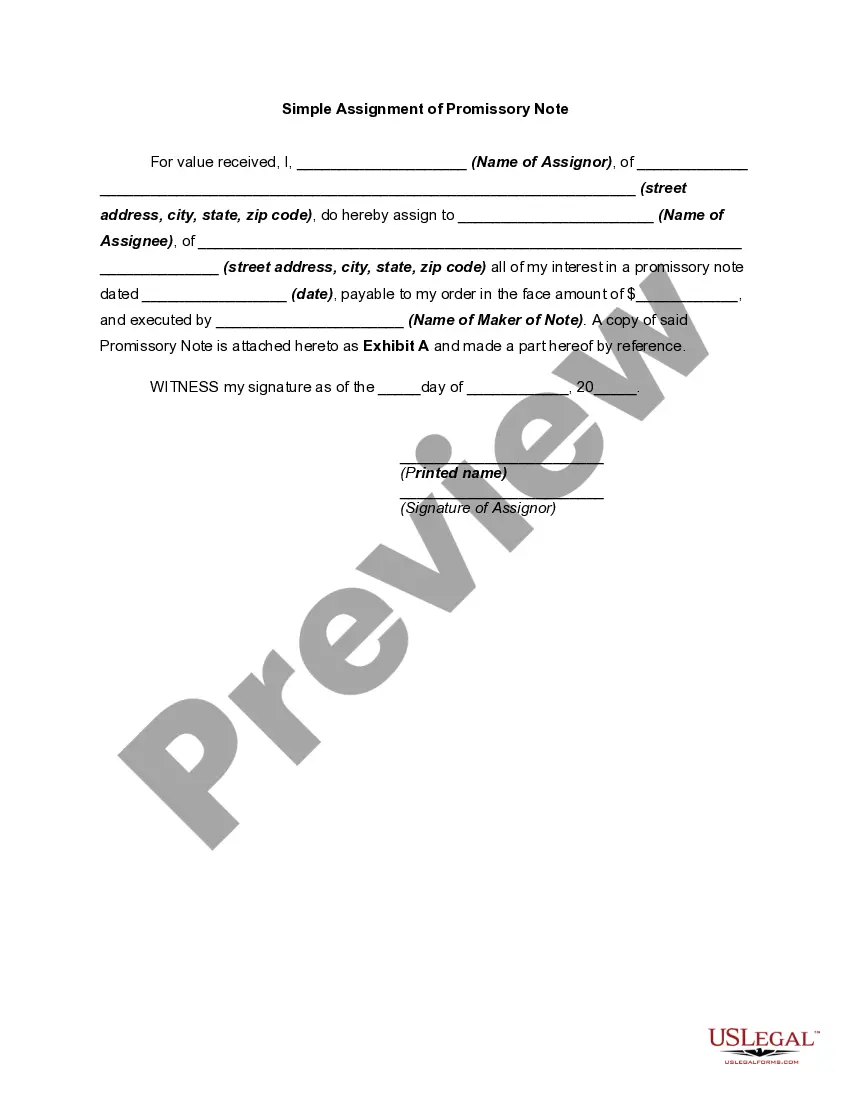

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

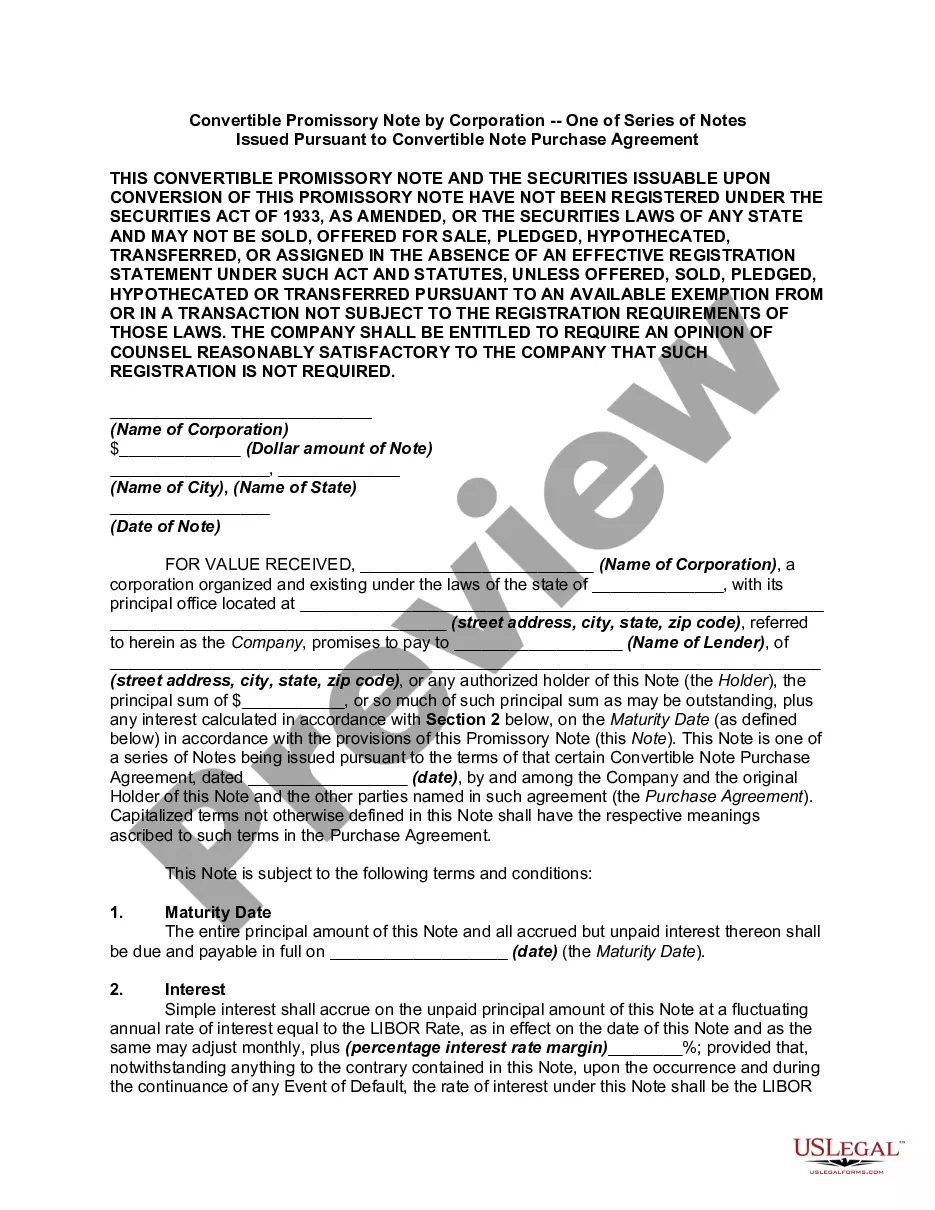

A promissory note must include the date of the loan, the dollar amount, the names of both parties, the rate of interest, any collateral involved, and the timeline for repayment. When this document is signed by the borrower, it becomes a legally binding contract.