Directors and officers liability insurance

Understanding this form

The Directors and Officers Liability Insurance form is a legal document designed for corporations seeking to protect their directors and officers from personal liability in certain situations. This insurance policy covers legal fees, judgments, and indemnification costs related to actions taken by the company's management. Unlike general liability insurance, this form specifically addresses the needs of corporate leaders, helping to ensure their financial protection in cases where the company cannot indemnify them under applicable law.

Main sections of this form

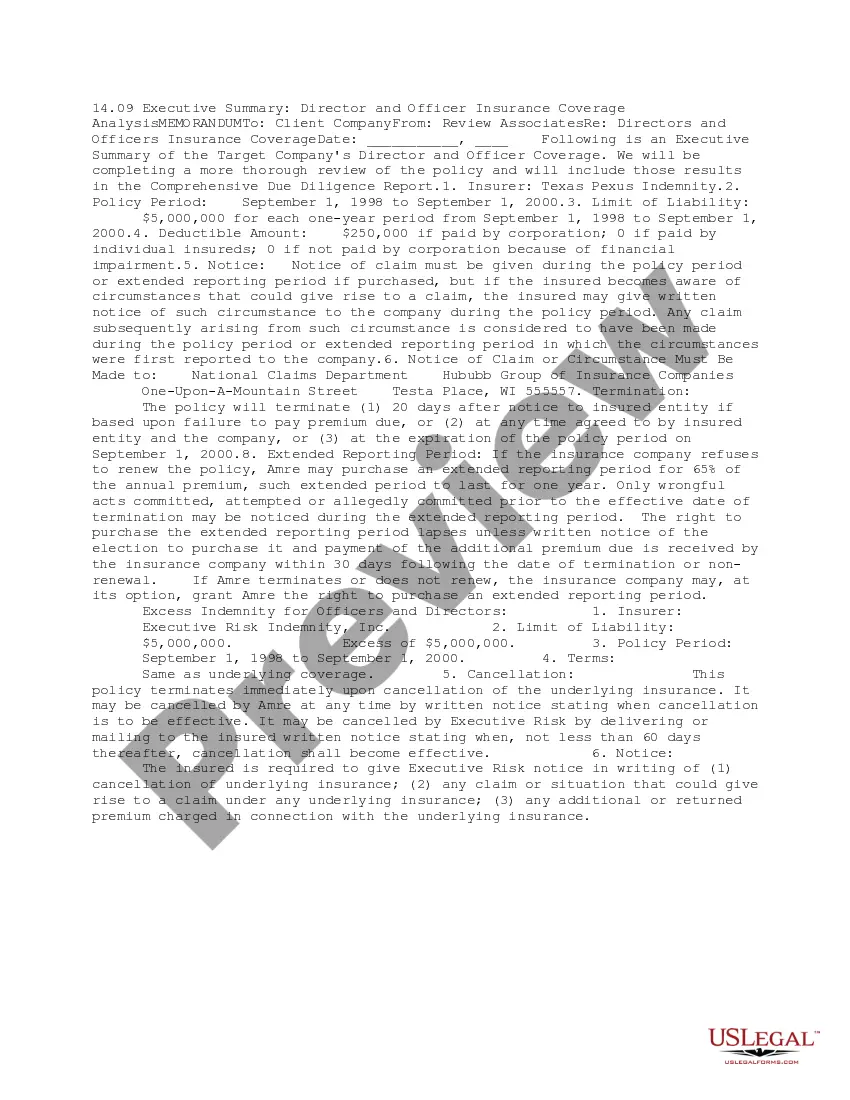

- Policy coverage details, specifying the protection offered to directors and officers.

- Inception date and duration of the insurance policies.

- Excess coverage information and the insurers involved.

- Indemnification provisions according to the companyâs By-Laws.

- Annual premiums and their allocation among major subsidiaries.

When to use this document

This form is essential when a corporation seeks to secure liability insurance for its directors and officers. Companies commonly use this form during the formation of their insurance policies or when renewing existing policies to ensure comprehensive coverage for executive leadership. It is also applicable during times when the company is facing potential legal actions that could involve their management, hence requiring clarification on indemnification rights.

Who needs this form

- Corporate entities looking to provide liability protection for their directors and officers.

- Business leaders seeking to understand the scope of coverage available under their insurance policies.

- Legal teams drafting or revising insurance agreements for corporate governance.

Steps to complete this form

- Identify the corporation and its major subsidiaries involved in the insurance coverage.

- Specify the details of the insurance policies, including coverage limits and insurers.

- Enter the inception date of the insurance policies and the duration of coverage.

- Detail the indemnification provisions as outlined in the companyâs By-Laws.

- Provide information about annual premiums and their distribution among the subsidiaries.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. However, always check with legal counsel to ensure compliance with any specific requirements applicable to your jurisdiction.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include all relevant subsidiaries under the policy.

- Not updating the policy upon renewal to reflect changes in law or company structure.

- Overlooking specific indemnification provisions that may differ by state.

Benefits of completing this form online

- Easy access to downloadable templates drafted by licensed attorneys.

- Editable formats that allow tailoring to specific corporate needs.

- Quick updates and revisions to stay compliant with changing laws.

Legal use & context

- This form serves to formalize the insurance arrangements for directors and officers.

- It helps mitigate risk for individuals in leadership positions against lawsuits or claims arising from their corporate duties.

- Adhering to the indemnification provisions allows the company to comply with corporate governance standards.

Main things to remember

- Essential for protecting corporate leaders from personal liability.

- Details the coverage terms and conditions of the insurance policy.

- Should be reviewed and customized per company and jurisdiction needs.

- Helps ensure compliance with legal obligations surrounding indemnification.

Looking for another form?

Form popularity

FAQ

D&O insurance will not provide coverage for what many would consider the worst acts of the directors or officers; dishonesty, fraud, criminal or malicious acts committed deliberately.D&O insurance will not provide coverage for bodily or personal injury of a person or physical damage to a third person's property.

Q: How much does D&O insurance typically cost? Pamela: Organizations with no employees can purchase $1 million in D&O limits for around $600 per year. Organizations with employees can expect to pay anywhere from about $1,200 for those with just a few employees, to around $4,000 to $5,000 for 50 employees.

Directors and officers (D&O) liability insurance covers directors and officers and/or their company or organization if sued. D & O insurance claims are paid to cover losses associated with the lawsuit, including legal defense fees. Most policies exclude fraud and criminal offenses.

D&O insurance will not provide coverage for what many would consider the worst acts of the directors or officers; dishonesty, fraud, criminal or malicious acts committed deliberately.D&O insurance will not provide coverage for bodily or personal injury of a person or physical damage to a third person's property.

D&O liability insurance policy, while it is not mandatory, is an important and integral part of corporate governance, as it protects the directors and officers against personal liabilities and also may ensure relief to the victims of corporate governance breakdowns.

D&O insurance helps protect nonprofit directors, officers and managers against exposures ranging from fiduciary malfeasance to wrongful termination claims. It helps cover the defense costs, settlements and judgments that could arise for allegations brought against a nonprofit organization.

Directors and officers (D&O) liability insurance protects the personal assets of corporate directors and officers, and their spouses, in the event they are personally sued by employees, vendors, competitors, investors, customers, or other parties, for actual or alleged wrongful acts in managing a company.

Over the last decade, LLC's have become one of the most preferred forms of business entities through which to hold investment real estate properties. However, LLC's do not qualify for coverage under a standard D&O policy.