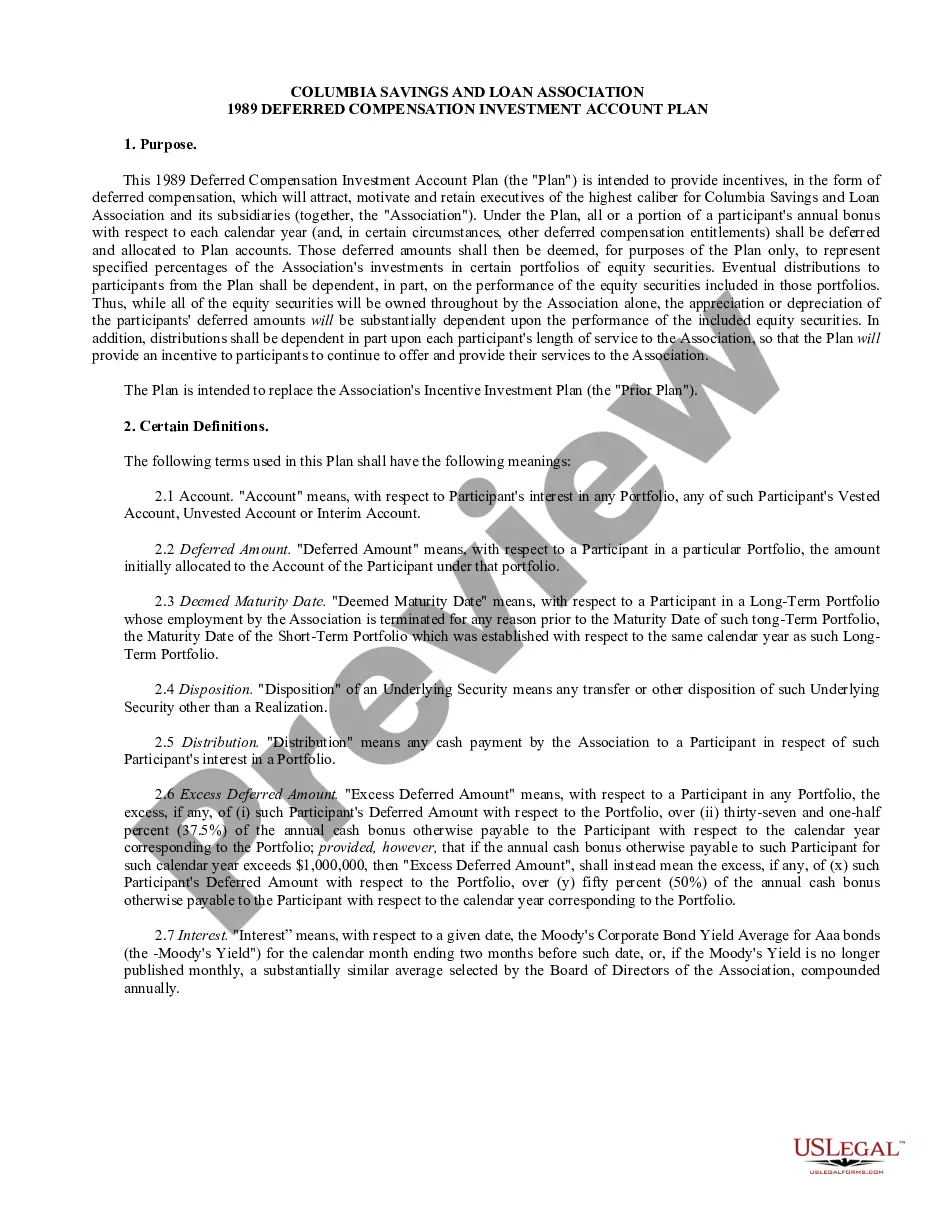

Approval of deferred compensation investment account plan

What this document covers

The Approval of Deferred Compensation Investment Account Plan is a legal document that outlines a compensation strategy aimed at providing tax-deferred incentives to attract and retain top executives. This form differs from other compensation-related forms by focusing specifically on creating a plan that allows executives to allocate a portion of their bonuses into investment portfolios without immediate tax implications. It is designed for organizations looking to enhance their executive compensation offerings in a competitive landscape.

Key parts of this document

- Objectives of the deferred compensation plan and its relevance to executive retention.

- Details on the allocation of equity securities and the method of determining their value.

- Vesting schedule based on the length of service within the organization.

- Distribution methods and timelines for participants once they reach maturity dates.

- Provisions regarding the management and administration of the plan by the Board of Directors.

When this form is needed

This form should be used when an organization seeks to implement a deferred compensation plan aimed at its executives. It is particularly relevant in situations where the organization aims to revise or replace an existing compensation plan that may not align with current market conditions or company objectives. Additionally, use this form when needing to establish clear guidelines for compensation deferrals and investment allocations to ensure compliance with tax regulations.

Who this form is for

- Organizations looking to implement or revise an executive compensation plan.

- Board members responsible for executive compensation packages.

- Human resources professionals involved in compensation strategy development.

- Financial officers overseeing compliance with tax regulations related to deferred compensation.

Instructions for completing this form

- Identify the organization and its participants, including executives eligible for the plan.

- Specify the percentage of annual bonuses to be deferred into the investment accounts.

- Detail the portfolios made up of underlying securities that will be used for this plan.

- Determine the vesting schedule and conditions for distributions of the investments.

- Have the Board of Directors review and approve the plan before implementing it.

Does this form need to be notarized?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to clearly outline the vesting schedule, leading to confusion among participants.

- Not adequately aligning the compensation plan with market standards, which might hinder recruitment efforts.

- Overlooking state-specific tax implications that could affect the plan's effectiveness.

Benefits of using this form online

- Convenience of completing the form at any time and from anywhere.

- Ability to easily edit and update information as needed without difficulty.

- Reliability of having a legally sound document drafted by licensed attorneys.

Looking for another form?

Form popularity

FAQ

How deferred compensation is taxed. Generally speaking, the tax treatment of deferred compensation is simple: Employees pay taxes on the money when they receive it, not necessarily when they earn it.The year you receive your deferred money, you'll be taxed on $200,000 in income10 years' worth of $20,000 deferrals.

Deferred compensation plans are an incentive that employers use to hold onto key employees. Deferred compensation can be structured as either qualified or non-qualified. The attractiveness of deferred compensation is dependent on the employee's personal tax situation. These plans are best suited for high earners.

Qualified plans include 401(k) plans, 403(b) plans, profit-sharing plans, and Keogh (HR-10) plans. Nonqualified plans include deferred-compensation plans, executive bonus plans, and split-dollar life insurance plans.

Depending on the terms of your plan, you may end up forfeiting all or part of your deferred compensation if you leave the company early. That's why these plans are also used as golden handcuffs to keep important employees at the company.They can't be transferred or rolled over into an IRA or new employer plan.

A deferred compensation plan allows employees to place income into a retirement account where it sits untaxed until they withdraw the funds. After withdrawal, the funds become subject to taxes, although this is usually much less if payment is deferred until retirement.

The short answer is yes. You can defer a significant portion of your compensation under a non-qualified retirement or deferred compensation plan. Deferred compensation plans are safe from your own creditors, but not the claims of your employer's creditors.

Deferred compensation plans don't have required minimum distributions, either. Based upon your plan options, generally, you may choose 1 of 2 ways to receive your deferred compensation: as a lump-sum payment or in installments.However, you will owe regular income tax on the entire lump sum upon distribution.

Your company will designate an amount you may defer and for how long you may defer that amountusually five years, 10 years or until you retire.In some cases, the company may make the choice for you by offering a guaranteed rate of return on the compensation, but this is rare.