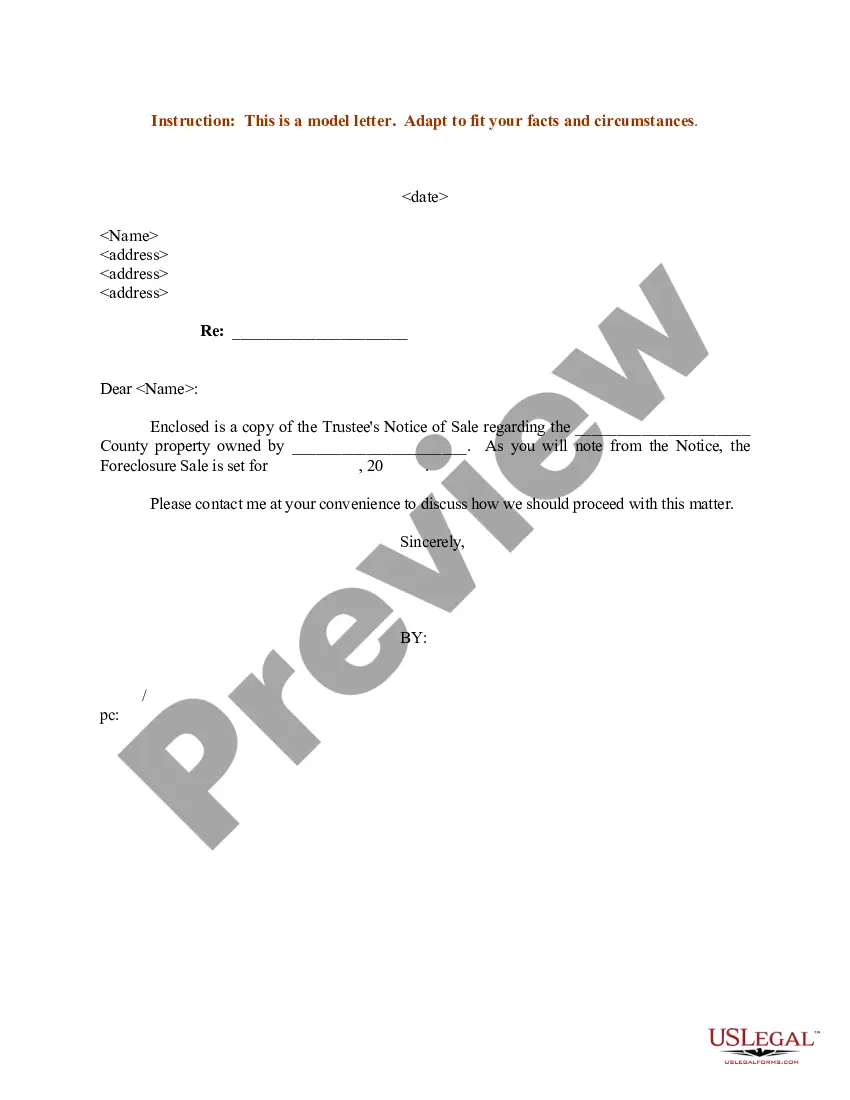

Sample Letter for Notice of Sale to Junior Lien Holder

What this document covers

The Sample Letter for Notice of Sale to Junior Lien Holder is a document that serves as a formal notice to junior lien holders regarding the impending sale of a property. This letter is essential for ensuring all parties with an interest in the property are informed about the foreclosure sale date and the ongoing legal proceedings. Unlike other notices, this specific letter targets junior lien holders, ensuring they are aware of their position and rights before a foreclosure sale occurs.

Main sections of this form

- Date of the notice

- Recipient information (name and address of the junior lien holder)

- Description of the property referenced

- Details of the foreclosure sale (including the sale date)

- Enclosure of the Substitute Trustees Notice of Sale

When this form is needed

This form is used when a property is going to foreclosure, and the lender must notify junior lien holders. It's crucial in situations where a lien holderâs financial interest might be affected by the sale of the property. For instance, if there are existing loans secured by the property, this notice ensures that junior lien holders are made aware of the sale, allowing them the opportunity to protect their interests.

Who can use this document

- Lenders or mortgage servicers initiating a foreclosure

- Real estate attorneys representing the lender

- Individuals working in property management

- Any entity holding a junior lien against the property

Completing this form step by step

- Identify the date of the notice to ensure timely communication.

- Complete the recipient information with the junior lien holder's name and address.

- Specify the property in question, using the full address.

- Insert the foreclosure sale date, providing clear information on when the sale is set to occur.

- Ensure that any necessary enclosures, such as the Substitute Trustees Notice of Sale, are included with the letter.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. It is recommended to check the specific legal requirements in your area before sending the letter.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include the correct address of the junior lien holder.

- Omitting the foreclosure sale date or providing incorrect details.

- Not enclosing the necessary documentation, leading to confusion.

- Sending the notice too late to protect the junior lien holders' interests.

Benefits of using this form online

- Convenient access to a legally drafted document that saves time.

- Editability allows users to customize the letter for their specific situation.

- Reliable templates drafted by licensed attorneys ensure legal compliance.

Summary of main points

- This form is essential for notifying junior lien holders of foreclosure sales.

- Complete the form with accurate information to avoid legal complications.

- Use this letter as part of your legal obligations in the foreclosure process.

Looking for another form?

Form popularity

FAQ

When a junior lienholder forecloses, a senior lienholder recovers nothing from the sale proceeds. But the senior lien remains intact and the foreclosure buyer takes title to the property subject to the senior lien.

Junior Lienholder Foreclosures For example, if your home is worth much more than its mortgage balance a junior lienholder might foreclose in expectation of receiving significant sale proceeds. Also, a junior lienholder might buy your first mortgage loan, become the new lienholder and then foreclose that lien.

A junior mortgage is a mortgage that is subordinate to a first or prior (senior) mortgage. A junior mortgage often refers to a second mortgage, but it could also be a third or fourth mortgage (e.g. home equity loans or lines of credit (HELOCs)).

When a junior mortgage holder has been sold-out in a first-mortgage foreclosure, that junior mortgage holder usually can, depending on state law, sue you personally on the promissory note to recover the money it loaned you.

Following a first-mortgage foreclosure, all junior liens (including a second mortgage and any junior judgment liens) are extinguished and the liens are removed from the property title. But the second-mortgage debt and creditor's judgment remain, even though they're no longer attached to the foreclosed property.

Once a non-mortgage lien is placed on your home, the holder of the lien can choose to take one of two routes.For example, property tax liens may sometimes be foreclosed outside of court, while the holder of a mechanics' liens must typically sue the homeowner in court in order to foreclose.

Following a first-mortgage foreclosure, all junior liens (including a second mortgage and any junior judgment liens) are extinguished and the liens are removed from the property title. But the second-mortgage debt and creditor's judgment remain, even though they're no longer attached to the foreclosed property.

In short, consensual liens do not adversely affect your credit as long as repayment terms are satisfied. Statutory and judgment liens have a negative impact on your credit score and report, and they impact your ability to obtain financing in the future.

A second mortgage or junior-lien is a loan you take out using your house as collateral while you still have another loan secured by your house.The term second means that if you can no longer pay your mortgages and your home is sold to pay off the debts, this loan is paid off second.