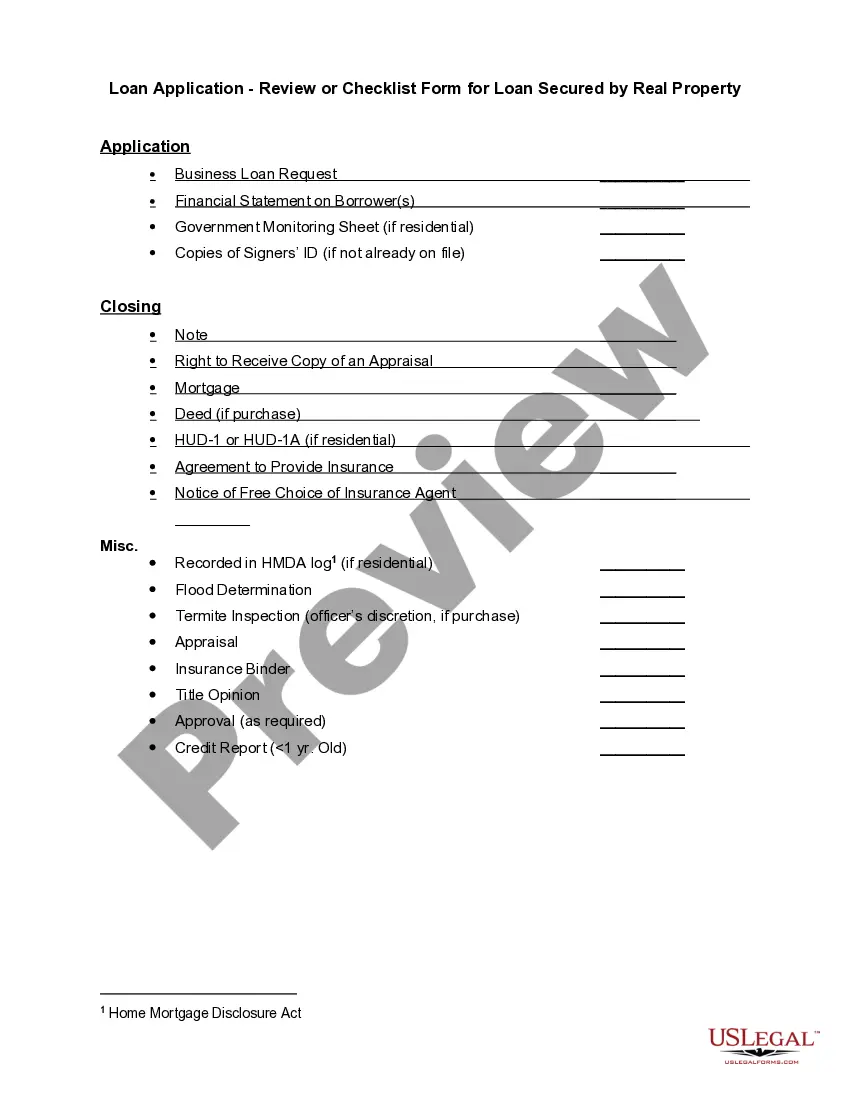

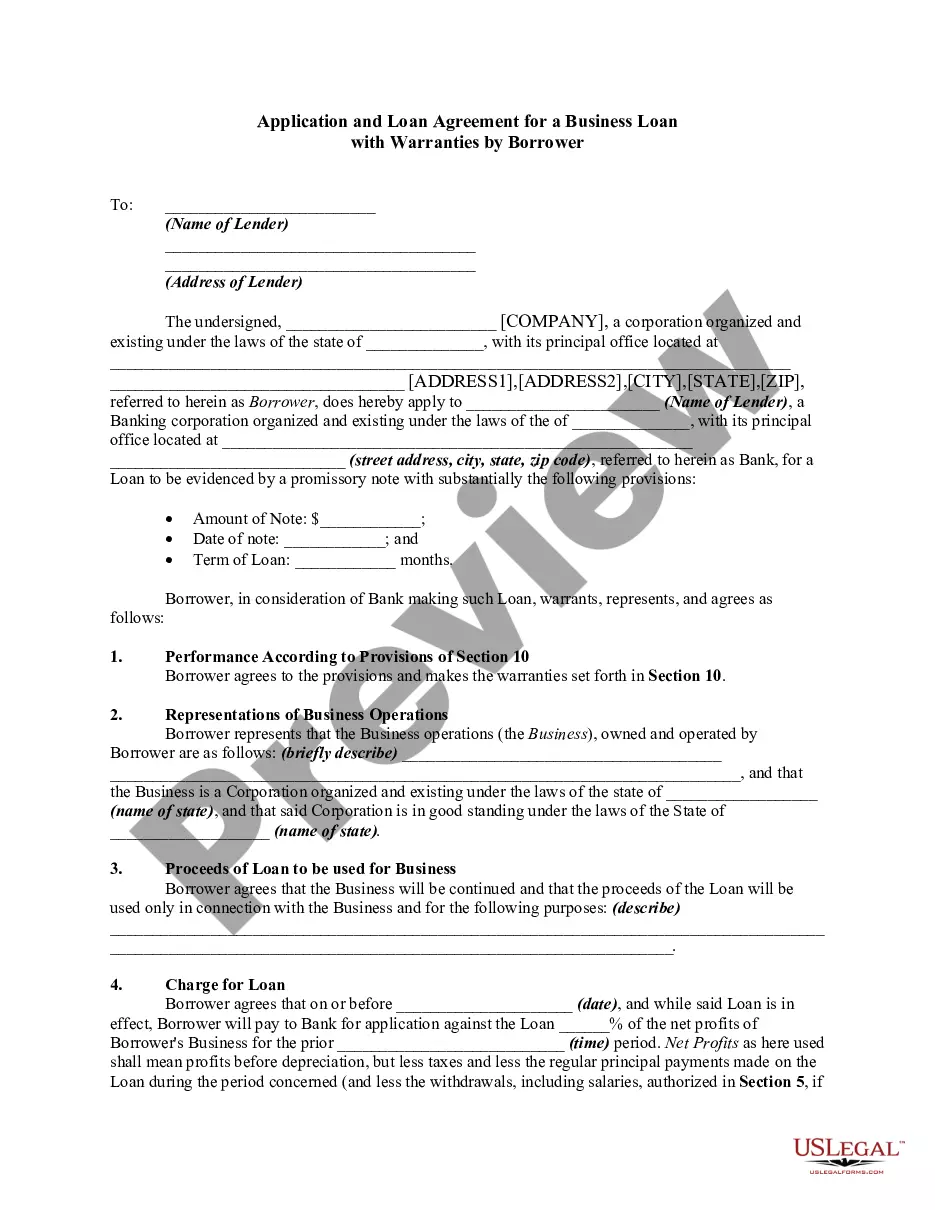

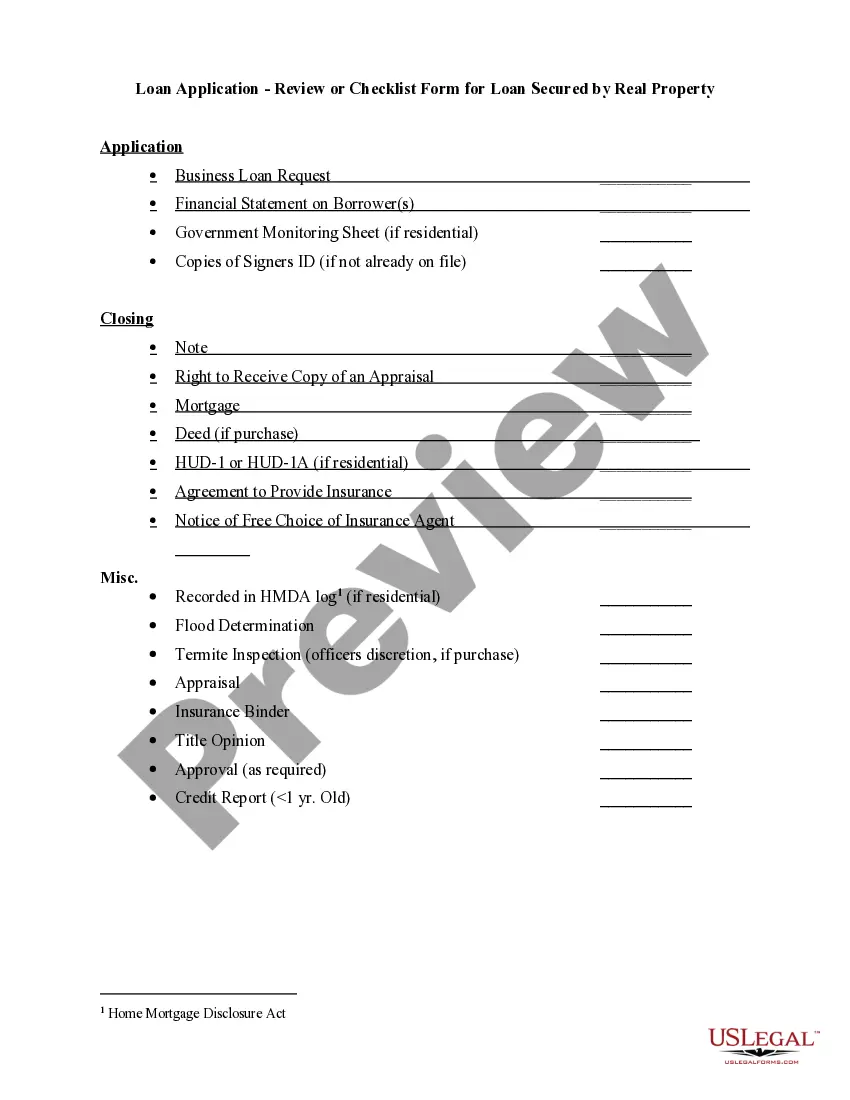

Review of Loan Application

What is this form?

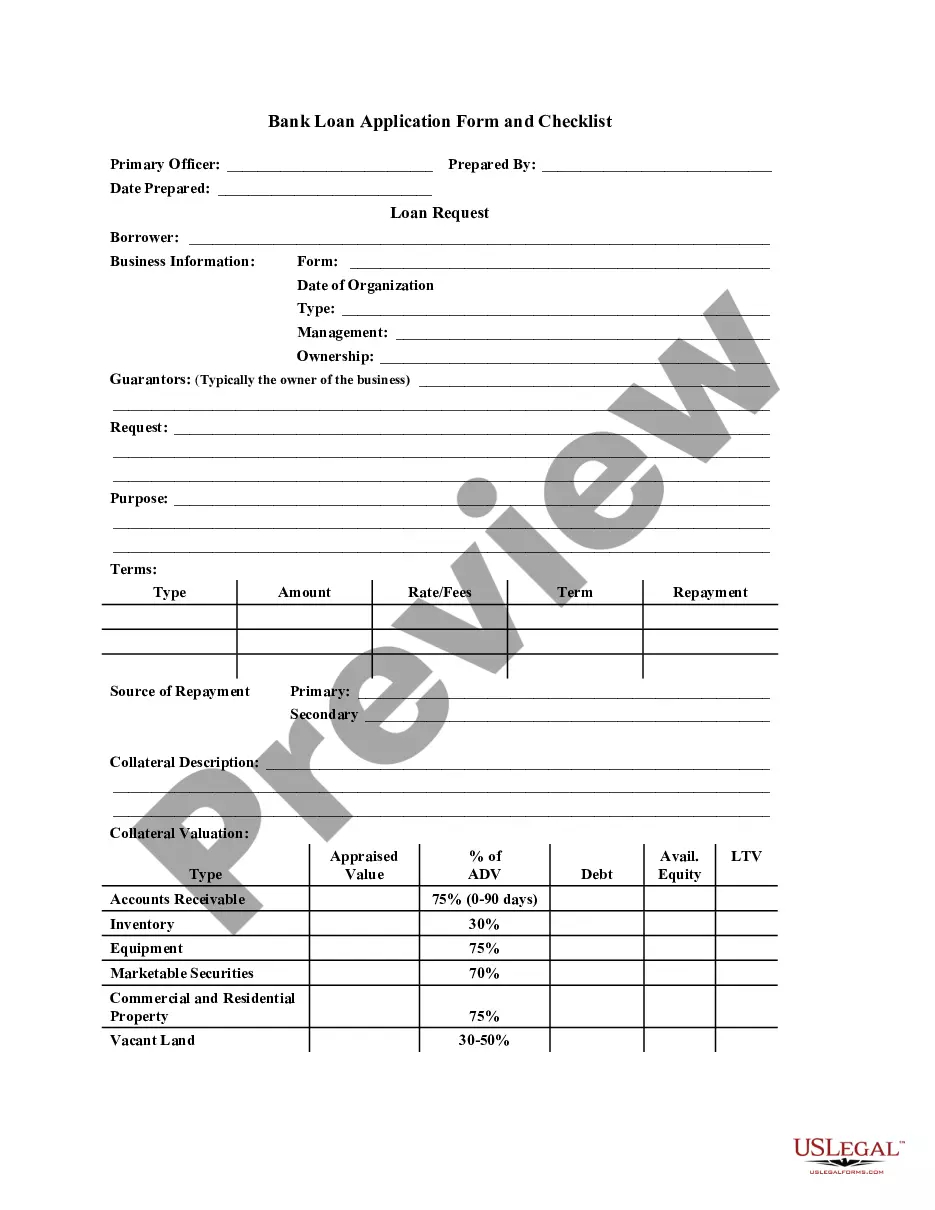

The Review of Loan Application is a template used by banks and financial institutions to evaluate a borrower's eligibility for a loan. It helps assess the borrower's financial background, business structure, and specific loan requirements. This form streamlines the application review process and distinguishes itself by focusing on the comprehensive financial standing and collateral of the applicant, unlike simpler loan application forms that may lack detailed analysis.

Key components of this form

- Name and business information of the borrower

- Loan request specifics, including amount and purpose

- Details about loan terms, rates, and payment options

- Collateral description and valuation details

- Credit history and payment history evaluation

- Financial statements and background information requirements

Common use cases

This form is necessary when a bank official needs to assess a loan application comprehensively. It should be used when evaluating a business or individual seeking a loan, ensuring all financial and collateral details are thoroughly documented. This is particularly useful when the loan amount is significant, or the borrower's financial history requires detailed examination.

Who this form is for

This form is intended for bank officials or lending agents involved in the loan approval process. Additionally, it can be helpful for business owners applying for loans to understand the information required for the assessment.

- Bank officials and loan underwriters

- Financial institutions reviewing loan applications

- Business owners seeking funding

How to prepare this document

- Enter the name of the borrower and the primary officer prepared to assess the loan.

- Provide the business information, including the form of business and date of formation.

- Specify the loan request details, including amount, purpose, and terms.

- Document the collateral details and its valuation.

- Include the financial statements from the last three years along with relevant tax returns.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. However, verifying with local regulations is advisable to ensure compliance with specific lending requirements.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failure to provide complete financial statements or required documents.

- Incorrectly assessing the value of collateral.

- Omitting details about the source of repayment.

- Leaving out critical information about business structure.

- Not updating payment history or loan terms adequately.

Advantages of online completion

- Easy access to a professionally drafted form created by licensed attorneys.

- Immediate download allows for quick completion and submission.

- Editable format enables users to customize the form as needed.

- Reliability from a trusted source ensures legal accuracy.

Looking for another form?

Form popularity

FAQ

When you apply for a loan, lenders assess your credit risk based on a number of factors, including your credit/payment history, income, and overall financial situation.The credit score serves as a risk indicator for the lender based on your credit history. Generally, the higher the score, the lower the risk.

Credit. An underwriter will assess a borrower's credit score and history to predict the borrower's ability to make their payments on time and in full. Capacity. Collateral. Protect Your Credit. Lower your Debt-to-Income Ratio. Ensure Employment Stability.

The answer is that it depends. Some banks have longer processes than others, but it should not take more than one or two business days. Once your loan has been approved, you'll need to wait for the funds to become available. Some banks can make the funds available the same day, but others take longer.

Loan review refers to the examination of outstanding loans to make sure borrowers are adhering to their credit agreements and the bank is following its own loan policies.Carrying out reviews of all types of loans on a periodic basis for example, every 30, 60, or 90 days.

If your credit is unblemished and you do provide all the necessary paperwork to your lender when you submit your loan application, your lender might be able to give you a type of approval quickly, often within 72 hours.

Loan Approval After the application and supporting documents are analyzed by the lender and Credit Administration, it is presented for review and approval. A decision will be made to reject the loan request, table the discussion pending more information, or approve the loan, generally with conditions.

How long does underwriting take? Underwritingthe process by which mortgage lenders verify your assets, and check your credit scores and tax returns before you get a home loancan take as little as two to three days. Typically, though, it takes over a week for a loan officer or lender to complete.

Initial criteria. We review the application to make sure that the borrower meets the initial criteria. Financial information. We first request the last two years' accounts and this provides us with a three-year history. Credit checks. Risk Band. Security. Identification.