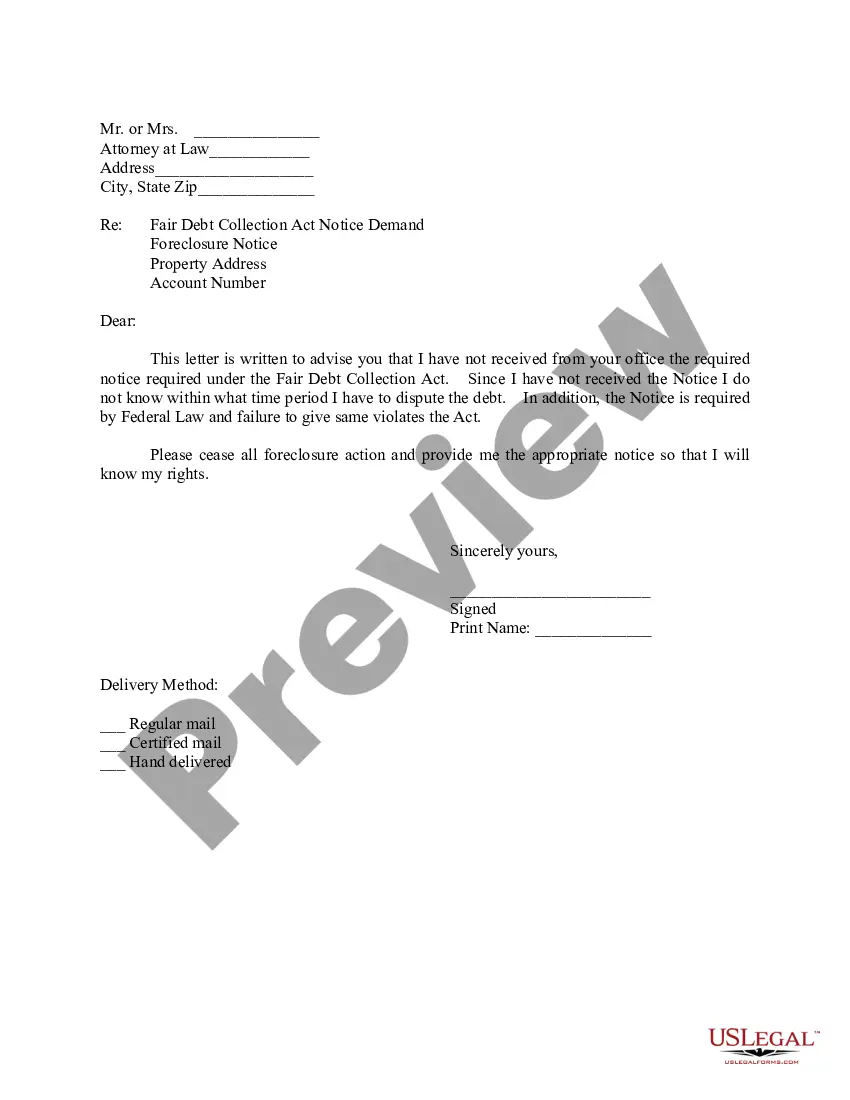

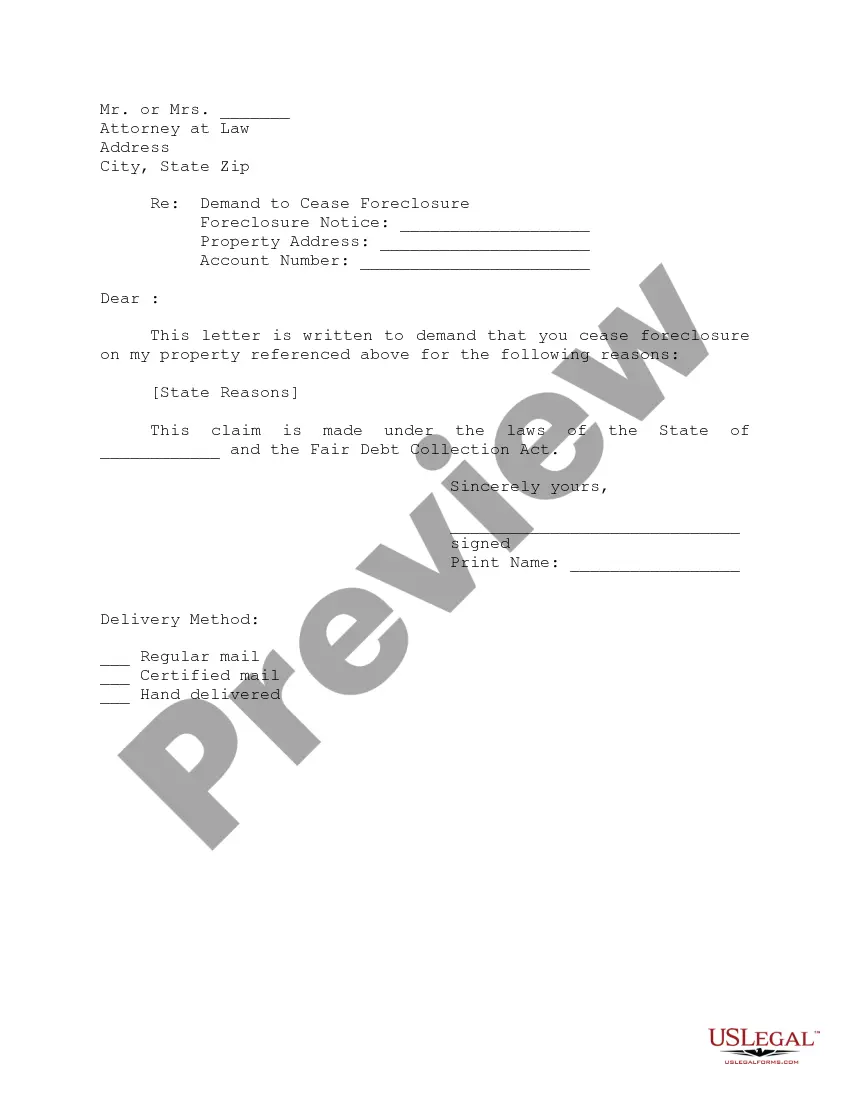

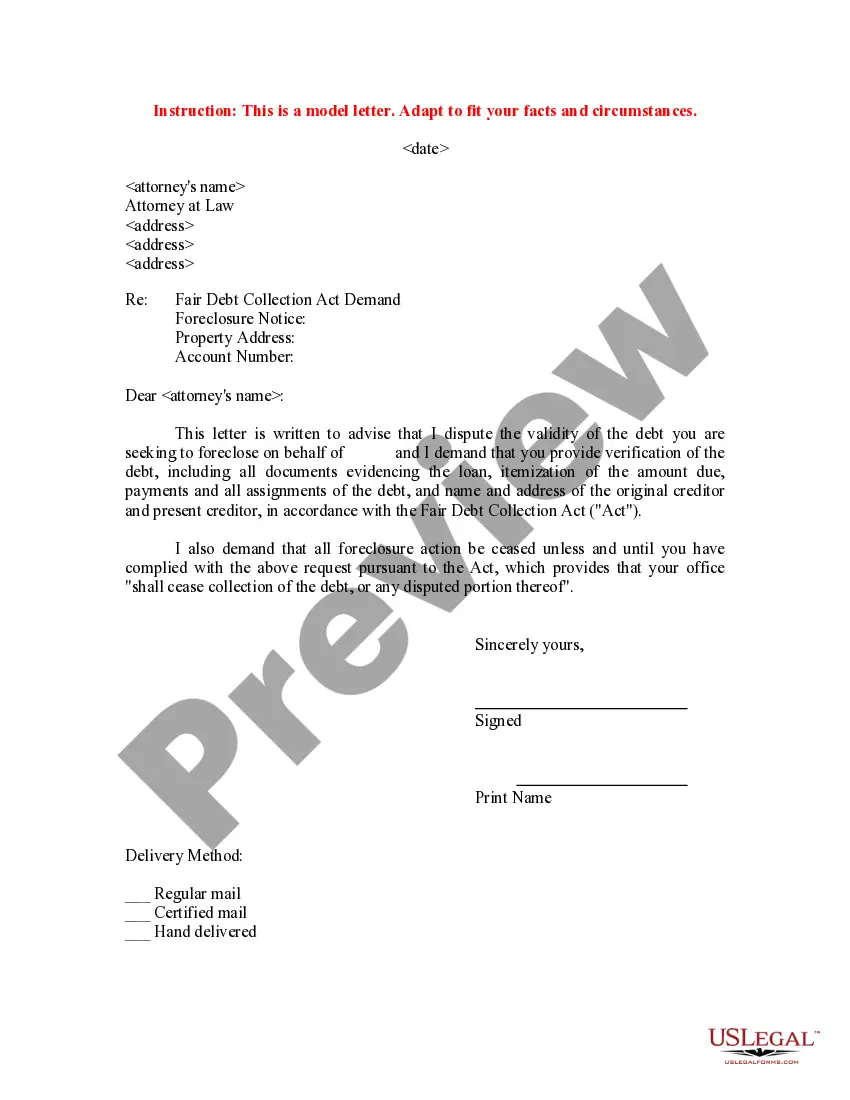

Letter to Foreclosure Attorney to Provide Verification of Debt and Cease Foreclosure

Understanding this form

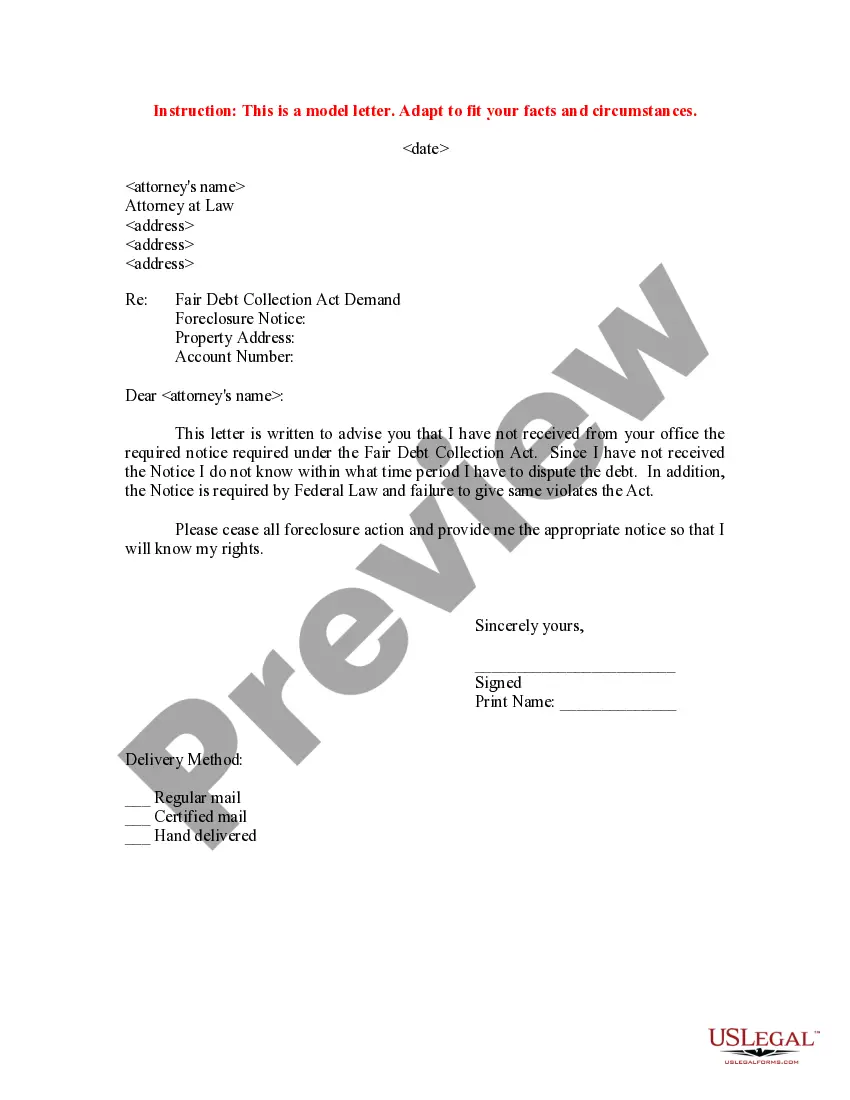

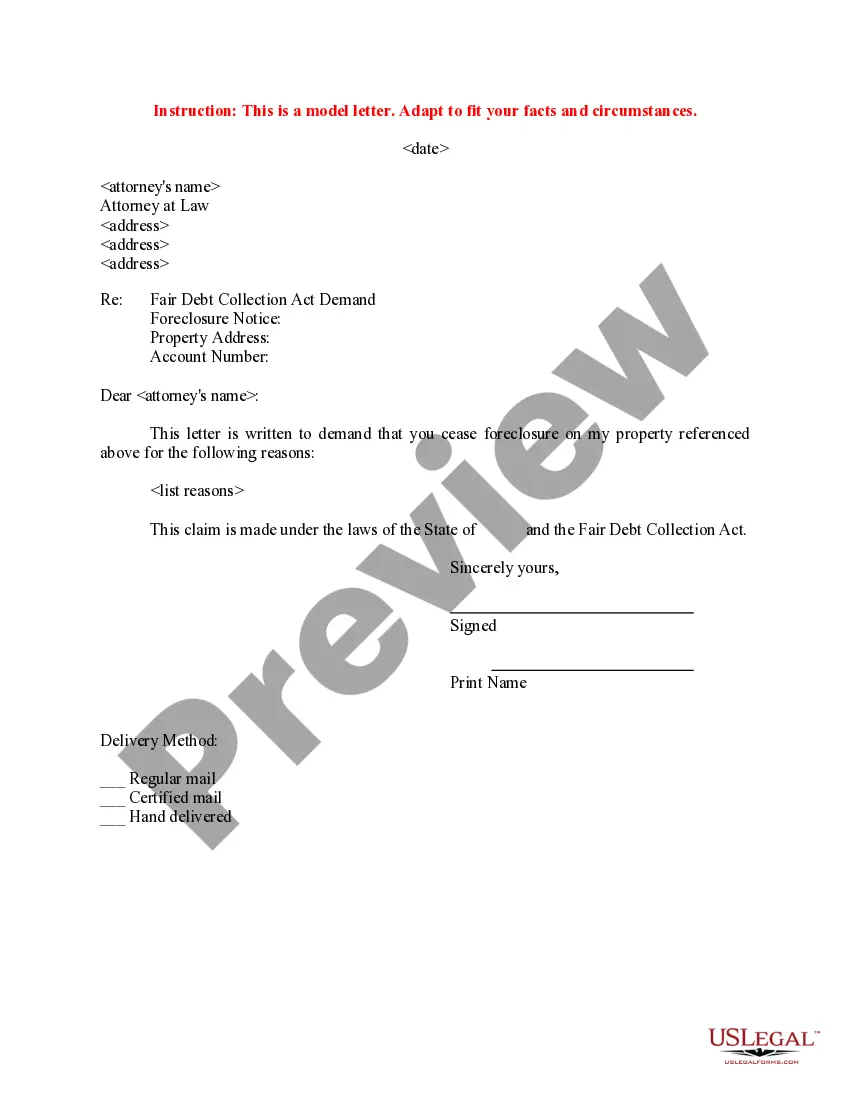

This form, titled Letter to Foreclosure Attorney to Provide Verification of Debt and Cease Foreclosure, is designed for individuals who are disputing a debt associated with a foreclosure. By using this form, the petitioner requests verification of the debt from the foreclosure attorney and demands that all foreclosure actions be halted until the request is resolved. This form helps protect the petitioner's rights under the Fair Debt Collection Act, ensuring that they receive proper documentation regarding the debt before any further action is taken.

What’s included in this form

- Contact information for the petitioner and the attorney.

- Reference to the Fair Debt Collection Act.

- Demand for verification of the debt, including detailed documentation.

- Instructions to cease all foreclosure actions until the verification is provided.

- Signature line for the petitioner and delivery method options.

When this form is needed

This form should be used when you are facing foreclosure and believe that the validity of the debt in question is disputed. It is particularly relevant if you have not received sufficient information about the debt or are unsure about the identity of the creditors involved. Using this letter requests the necessary documentation to verify the debt and pauses the foreclosure process until this information is provided.

Intended users of this form

- Homeowners facing foreclosure proceedings.

- Individuals who dispute the validity of their mortgage debt.

- Anyone seeking clarification and verification from a foreclosure attorney.

Steps to complete this form

- Enter your name and contact information at the top of the letter.

- Identify the attorney's name and address to whom the letter is directed.

- Clearly state the property address and account number related to the foreclosure.

- Detail your dispute and request for verification of the debt, citing the Fair Debt Collection Act.

- Sign the letter and choose your preferred delivery method.

Does this form need to be notarized?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include complete contact information.

- Not citing the Fair Debt Collection Act correctly.

- Overlooking the requirement to specify the property address and account number.

- Neglecting to sign the letter before sending it.

Benefits of completing this form online

- Easy access to a legally sound template created by licensed attorneys.

- Convenient downloadable format that allows for quick completion.

- Editable fields make it simple to customize the letter to your specific situation.

Summary of main points

- This form is essential for disputing a foreclosure-related debt.

- It ensures that you receive verification of the debt before further legal action.

- Understanding how to complete this form accurately is vital for protecting your rights.

Looking for another form?

Form popularity

FAQ

A statement that if you write to dispute the debt or request more information within 30 days, the debt collector will verify the debt by mail. A statement that if you request information about the original creditor within 30 days, the collector must provide it.

If the collector completely fails to respond to the validation letter, again they have 30 days to do so, then legally they must cease collection efforts, and remove negative items placed by them on your credit report.That way, you can have the items removed by contacting the credit bureaus.

It is the purpose of this subchapter to eliminate abusive debt collection practices by debt collectors, to insure that those debt collectors who refrain from using abusive debt collection practices are not competitively disadvantaged, and to promote consistent State action to protect consumers against debt collection

Fair Debt Collection Practices Act (FDCPA) Validation Letter The Fair Debt Collection Practices Act (FDCPA) is a federal law that protects consumers from abusive collection practices by debt collectors and collection agencies.

Under the FDCPA, a debt collector must respond to a request for a debt validation letter. If they don't, they're in violation of the act. You can report them to your state's attorney general, the FTC or the Consumer Financial Protection Bureau (CFPB). You can also sue for up to $1,000, plus damages.

Like the credit bureaus, the collection agency has 30 days to investigate and respond to your dispute. Most disputes dealing with removing inaccurate information get resolved smoothly. Make sure you follow the steps and provide all the necessary documentation to back your claim.

This is important: You have just 30 days to respond to a debt validation letter. If you don't dispute the debt within 30 days, the debt is assumed valid. That means the debt collector can continue to contact you. You can send a dispute after 30 days.

For the name and contact information of the original creditor. why the collector believes you own the debt in the first place. for a record of all owners of the debt. the amount and age of the debt (including an account number if you're able). under what authority the collector has to collect.

You have the right to force the debt collector to prove you owe the money. Debt validation is your federal right granted under the Fair Debt Collection Practices Act (FDCPA). To request debt validation, you must send a written request to the debt collector within 30 days of being contacted by the collection agency.