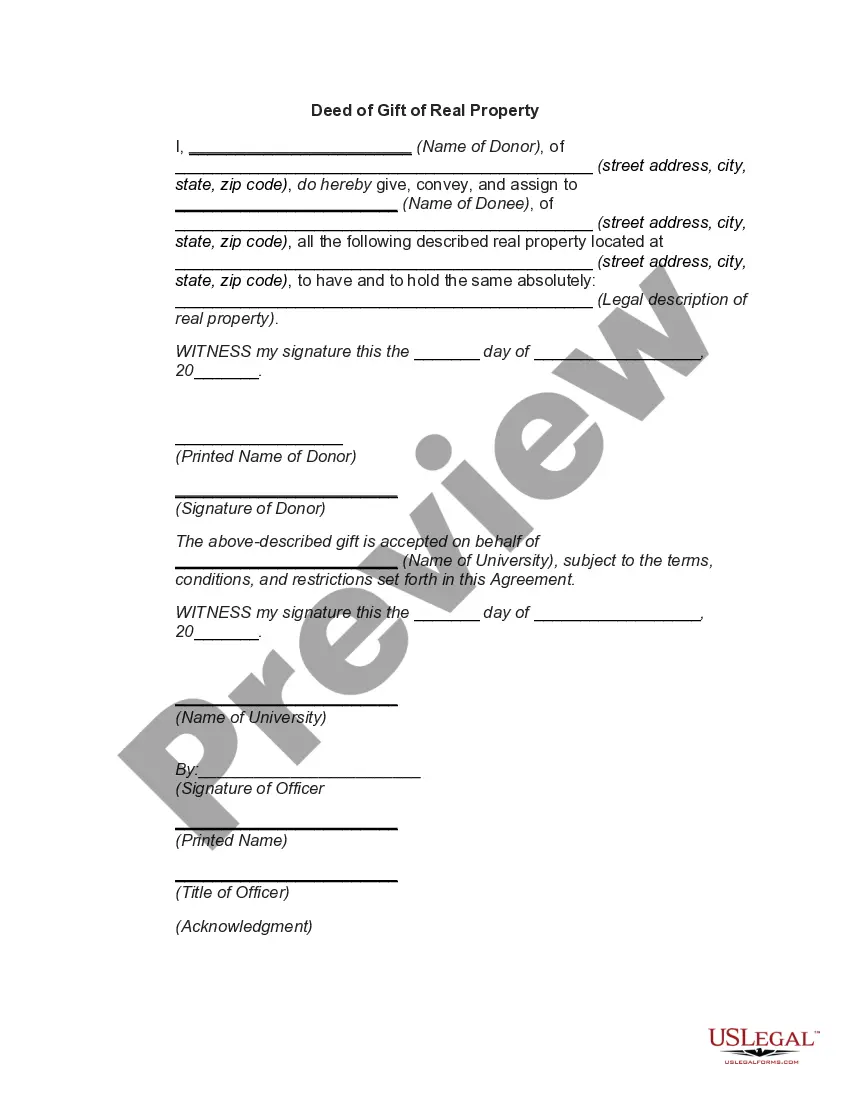

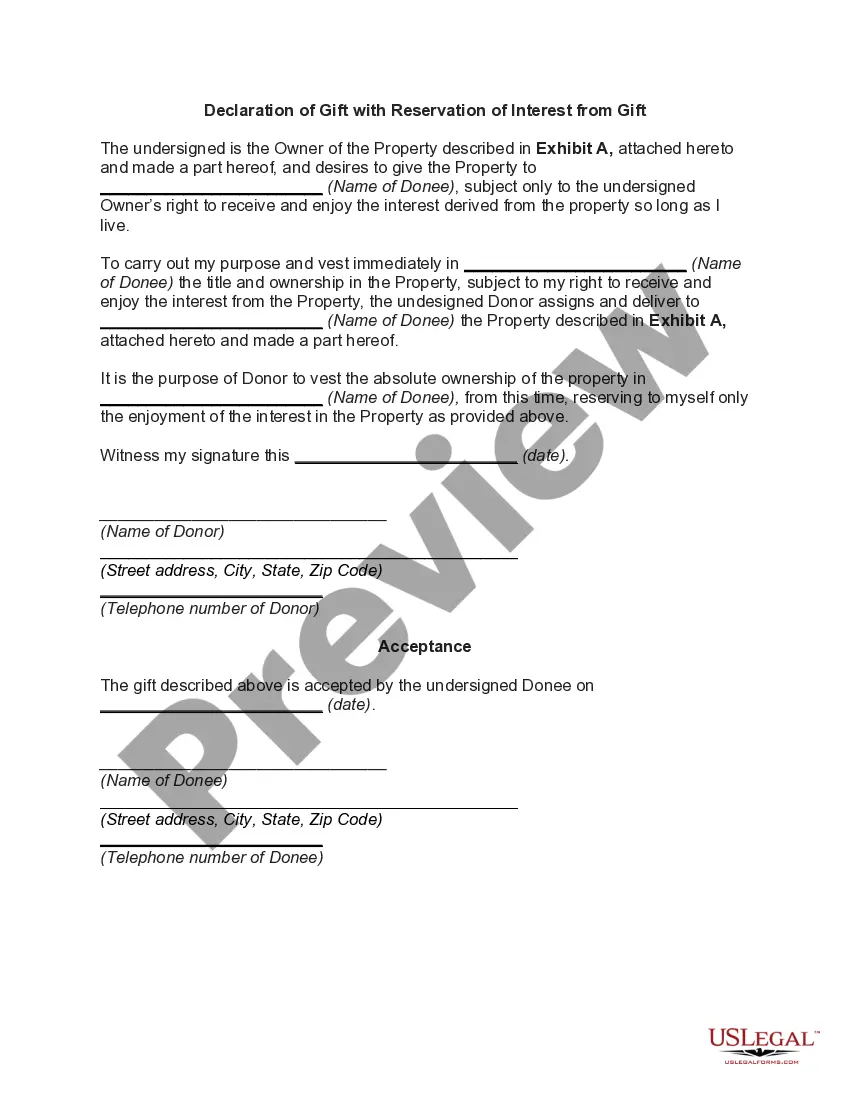

Gift of Entire Interest in Literary Property

Overview of this form

The Gift of Entire Interest in Literary Property is a legal document that formalizes the transfer of all rights, title, and ownership of a literary work from one party (the donor) to another (the donee). Unlike similar forms, this document ensures that the donee gains full copyright over the manuscript, which can include books, articles, or other written content. This form is essential for authors or copyright holders wishing to transfer their rights completely and irrevocably.

Form components explained

- Name and address of the donor

- Name and address of the donee

- Title of the literary work being transferred

- Irrevocable assignment of all rights and ownership

- Signature of the donor with date of execution

Common use cases

This form should be utilized when an author or copyright holder wishes to gift their entire interest in a literary work to another individual or entity. It is ideal for situations such as passing on rights to a family member, transferring ownership to a publisher, or fulfilling contractual obligations. Using this form ensures that the transaction is documented legally and that all rights are transferred smoothly.

Who can use this document

- Authors or creators of literary works

- Individuals wishing to gift their rights to a literary work

- Estates managing the interests of deceased authors

- Publishers acquiring rights to literary properties

Instructions for completing this form

- Identify and enter the name and address of the donor.

- Specify the name and address of the donee.

- Provide the title of the literary work being transferred.

- Clearly state the irrevocable nature of the transfer.

- Have the donor sign and date the form to validate the transfer.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. Always check applicable regulations in your state to confirm whether notarization is needed for the gift of literary property.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to provide complete addresses for both parties.

- Not clearly indicating the title of the literary work being transferred.

- Omitting the date of the donor's signature.

- Using unclear language that may cause ambiguity about the rights being transferred.

Benefits of completing this form online

- Convenient access to legally vetted forms that can be downloaded instantly.

- Editable templates, allowing users to input their specific information easily.

- Reliable resources that ensure compliance with general legal standards.

- Time-saving options to prepare legal documentation from the comfort of your home.

Legal use & context

- A properly executed gift of literary property ensures that the donee has complete rights to the work.

- Failure to use this form may result in disputes regarding ownership rights in the future.

- Legally documenting the transfer protects both parties under copyright law.

Main things to remember

- The Gift of Entire Interest in Literary Property form is essential for transferring full ownership rights of a manuscript.

- Ensure all required fields are accurately completed to avoid legal issues.

- Consult local laws to confirm the necessary steps for your jurisdiction.

Looking for another form?

Form popularity

FAQ

To transfer a property as a gift, you need to fill in a TR1 form and send it to the Land Registry, along with an AP1 form. If either side is not using a Solicitor or Conveyancer, an ID1 form will also be needed.

The owner should be of sound mind and acting of their own free will. Independent legal advice should be sought before commencing with a deed of gift. The property in question should have no outstanding debts secured against it.

While you can leave real estate as a gift to a family member as part of your estate plan, you can also give your home or property as a gift in other ways. When you're transferring property as a gift to a family member or friend, generally a document such as a Quitclaim Deed is used.

One may be to sell your property and gift the proceeds to your children, although you would need to bear in mind that this would still be subject to Inheritance Tax if you were to pass away within seven years of the gift. The main alternative to gifting property is to create a Life Interest Trust Will.

While you may not have to pay gift taxes on the gift, if your children sell the house right away, they may be facing steep taxes. The reason is that when you give away your property, the tax basis (or the original cost) of the property for the giver becomes the tax basis for the recipient.

It is possible to transfer the ownership of a property to a family member as a gift, meaning no money exchanges hands. This differs to a Transfer of Equity, where the owner remains on the title and simply adds someone else to it.

Other tax implications But if you are gifting a property which is not your principle residence, such as a buy-to-let flat or a holiday home, the gift could incur capital-gains tax (CGT). This would be calculated on the difference between the purchase price and the property's value at the time of the gift.

If you gift your home to family members or someone else while you're alive there will be no inheritance tax payable as long as you move out or at least pay rent and live for seven years after the handover.If this happens, inheritance tax will still be payable on the property, even if you live for seven years.