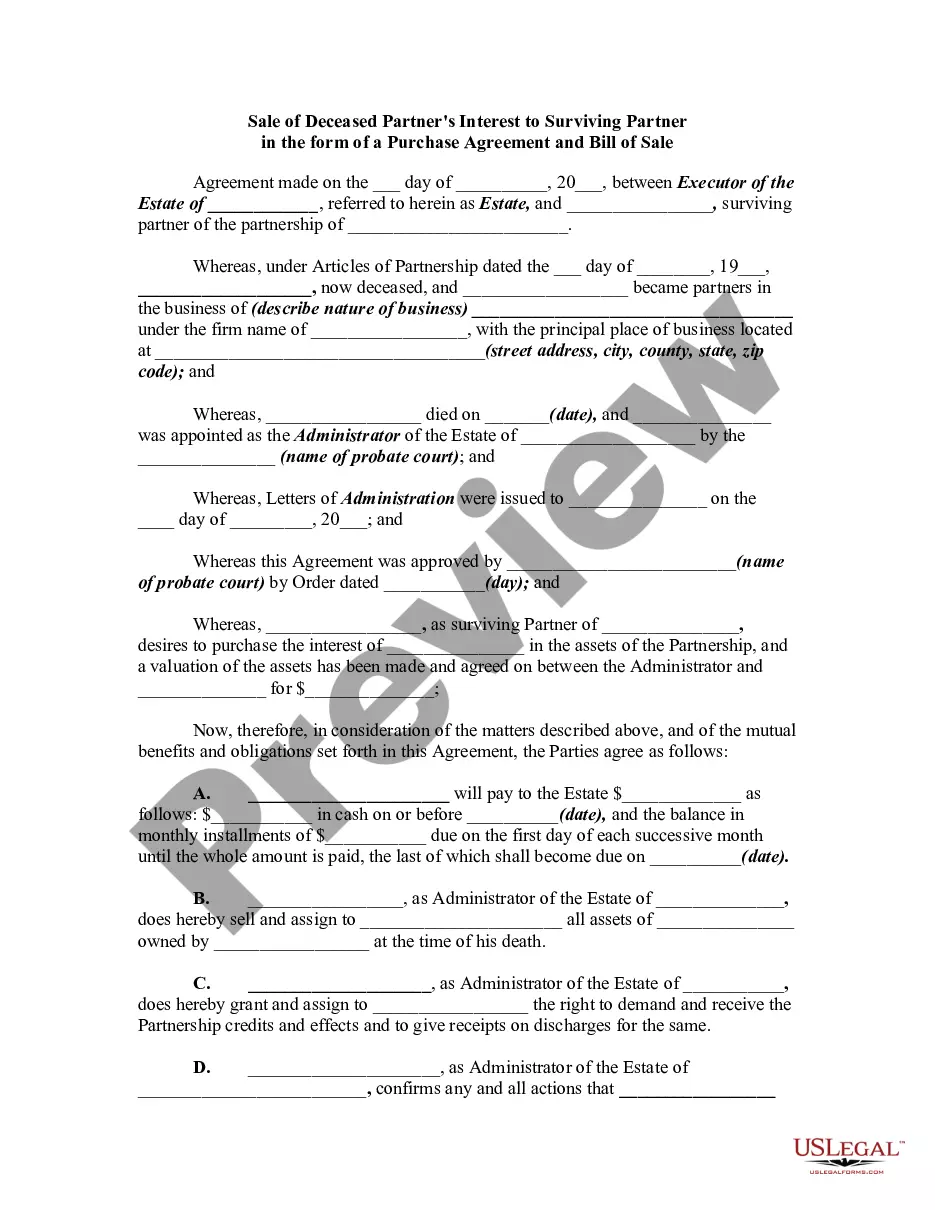

Sale of Deceased Partner's Interest

What this document covers

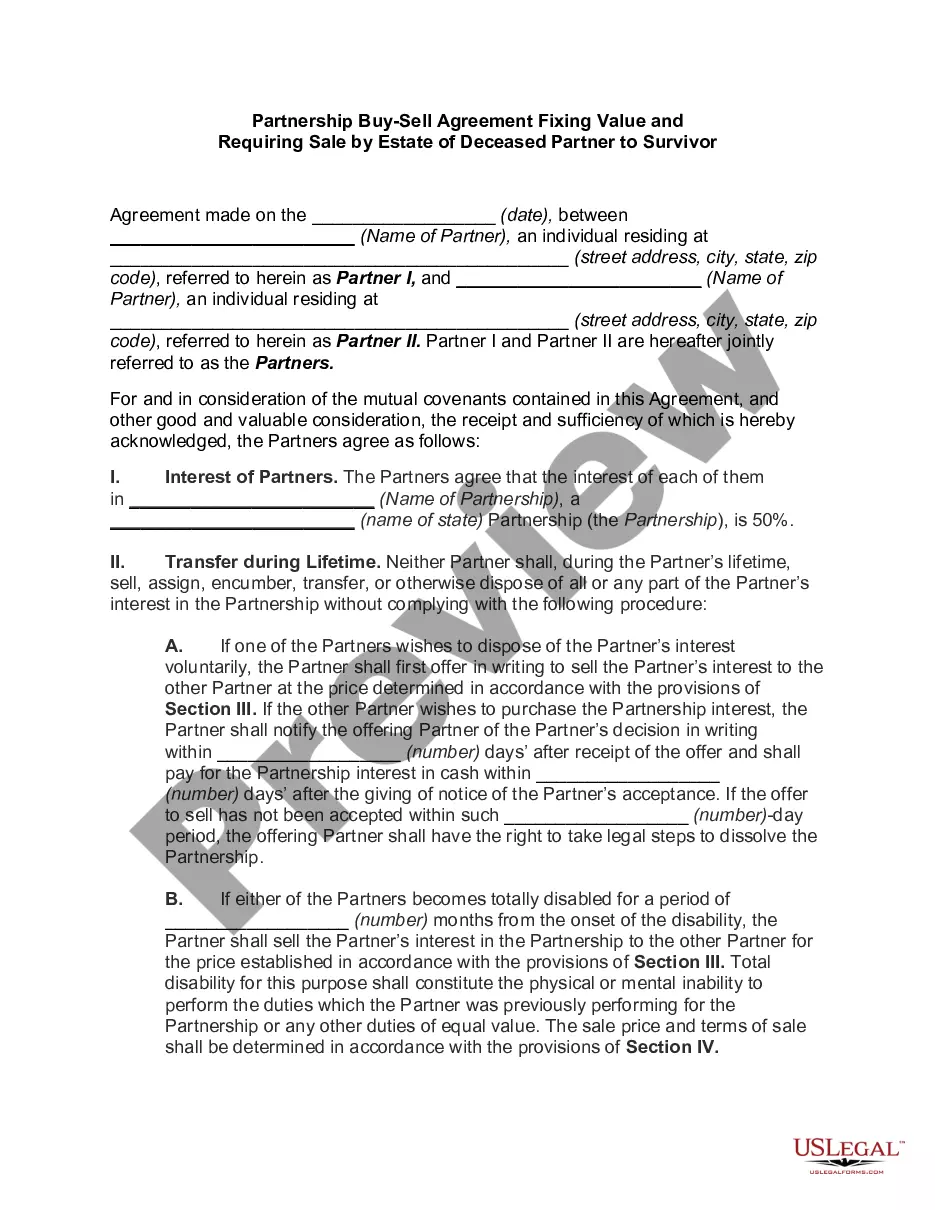

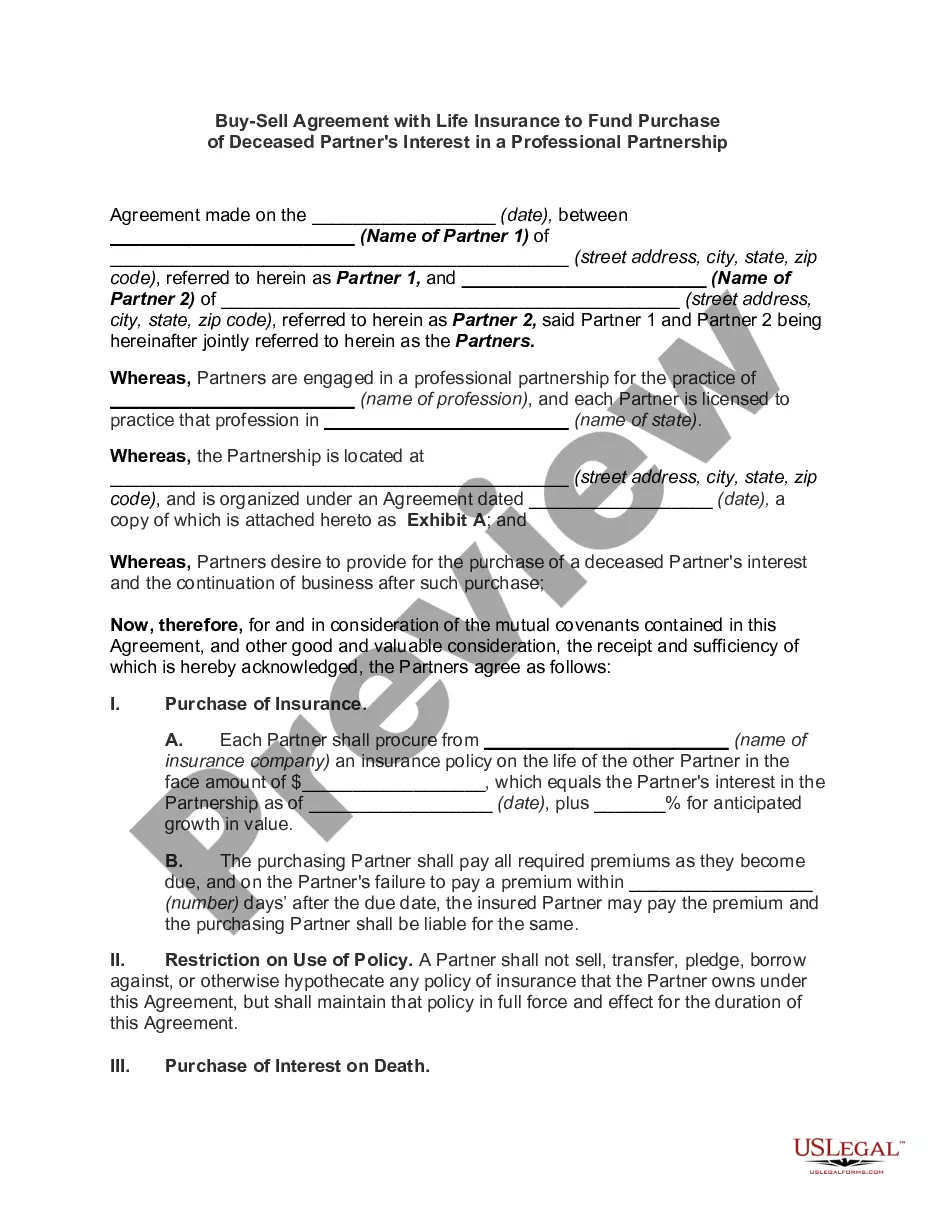

The Sale of Deceased Partner's Interest form is an agreement designed to ensure the continuation of a partnership business following the death or retirement of a partner. Unlike standard partnership agreements, this specific form outlines the procedures for purchasing a deceased partner's interest in the partnership, which is essential for maintaining business stability during transitional periods. It streamlines the process of valuing the departed partner's stake and sets forth the rights of surviving partners in this situation.

Key components of this form

- Identification of all partners involved in the agreement.

- Specifics about the principal place of business of the partnership.

- Details regarding life insurance policies benefiting the partnership.

- Agreement on the purchase rights of the partnership for a deceased partner's interest.

- Procedure for determining the purchase price of the deceased partner's interest.

- Provisions outlining the payment process to the deceased partner's estate.

When to use this document

This form should be utilized when a partner in a partnership has passed away or is retiring, and there's a need to facilitate the transfer of their partnership interest. It's crucial in situations where partners wish to ensure continuity of business operations and funding remains available to buy out the deceased or retiring partner's stake. This form is also beneficial for solidifying ownership rights and the financial responsibilities of the remaining partners.

Who should use this form

This form is intended for:

- Partnerships with multiple partners, particularly those involving general partners.

- Surviving partners needing to formalize the purchase of a deceased partner's interest.

- Executors or administrators of a deceased partnerâs estate tasked with managing the partnership interest.

Instructions for completing this form

- Identify the partners involved by entering their names and the partnership name.

- Indicate the principal place of business of the partnership.

- List all relevant life insurance policies and specify the amount and insured person.

- Complete the purchase price determination section by referencing partnership books.

- Ensure all partners sign the form for it to be valid and effective.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, verifying local requirements is essential to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include all partners in the agreement.

- Not accurately documenting life insurance policy details.

- Omitting signatures or dates, which can invalidate the agreement.

- Incorrectly calculating the purchase price based on outdated partnership records.

Why use this form online

- Convenience of downloading and editing the form as needed.

- Access to attorney-drafted templates ensures legal compliance.

- Time-saving compared to traditional methods of form creation.

Legal use & context

- The Sale of Deceased Partner's Interest is legally enforceable if properly executed according to state laws.

- This agreement helps prevent disputes among surviving partners and the estate of the deceased partner.

- Clear delineation of terms can significantly facilitate estate settlements and transfers.

Key takeaways

- The form is essential for managing a partnership in the event of a partner's death or retirement.

- It outlines the process for purchasing a deceased partner's interest, ensuring transparency.

- Signing all partners can avoid future conflicts and clarify rights and obligations.

Looking for another form?

Form popularity

FAQ

2012 Review Schedule D, Form 8949 and Form 4797 to determine the amount of gain or loss the partner reported on the sale of the partnership interest. After determining a partner sold its interest in the partnership, establish other relevant facts that can impact the tax treatment of this transaction.

The decedent's estate (or other successor, such as a living/revocable trust, depending upon how the deceased partner held their partnership interest; the Estate), will take such interest with an adjusted basis equal to the fair market value of such interest at the date of the partner's death, increased by the

Because tax law views a partnership both as an entity and as an aggregate of partners, the sale of a partnership interest may result either in a capital gain or loss or all or a portion of the gain may be taxed as ordinary income.

Complete Part I and Part II, Items E through I, on each partner's K-1. This is used to provide personal information. Complete Part III of each partner's K-1. Complete the selling partner's K-1. Complete the remaining partners' K-1s.

The federal income tax rules for partnership payments to buy out an exiting partner's interest are tricky, but they also open up tax planning opportunities. Payments made by a partnership to liquidate (or buy out) an exiting partner's entire interest are covered by Section 736 of the Internal Revenue Code.

This will produce a capital gain under IRC Section 741. While there are Code sections that could convert the capital gain into ordinary income on the sale of the partnership interests, there is no look through rule that would convert a capital gain into a Section 1231 gain.

To take a loss for abandonment of a partnership interest, a taxpayer must show that in the year the loss deduction was claimed, the taxpayer intended to abandon the partnership interest and that there was an affirmative act of abandonment of the interest.

That could mean the partnership agreement is dissolved immediately upon their death. You will then owe your partner's estate a debt for their share of the partnership that accrues at the date of their death.