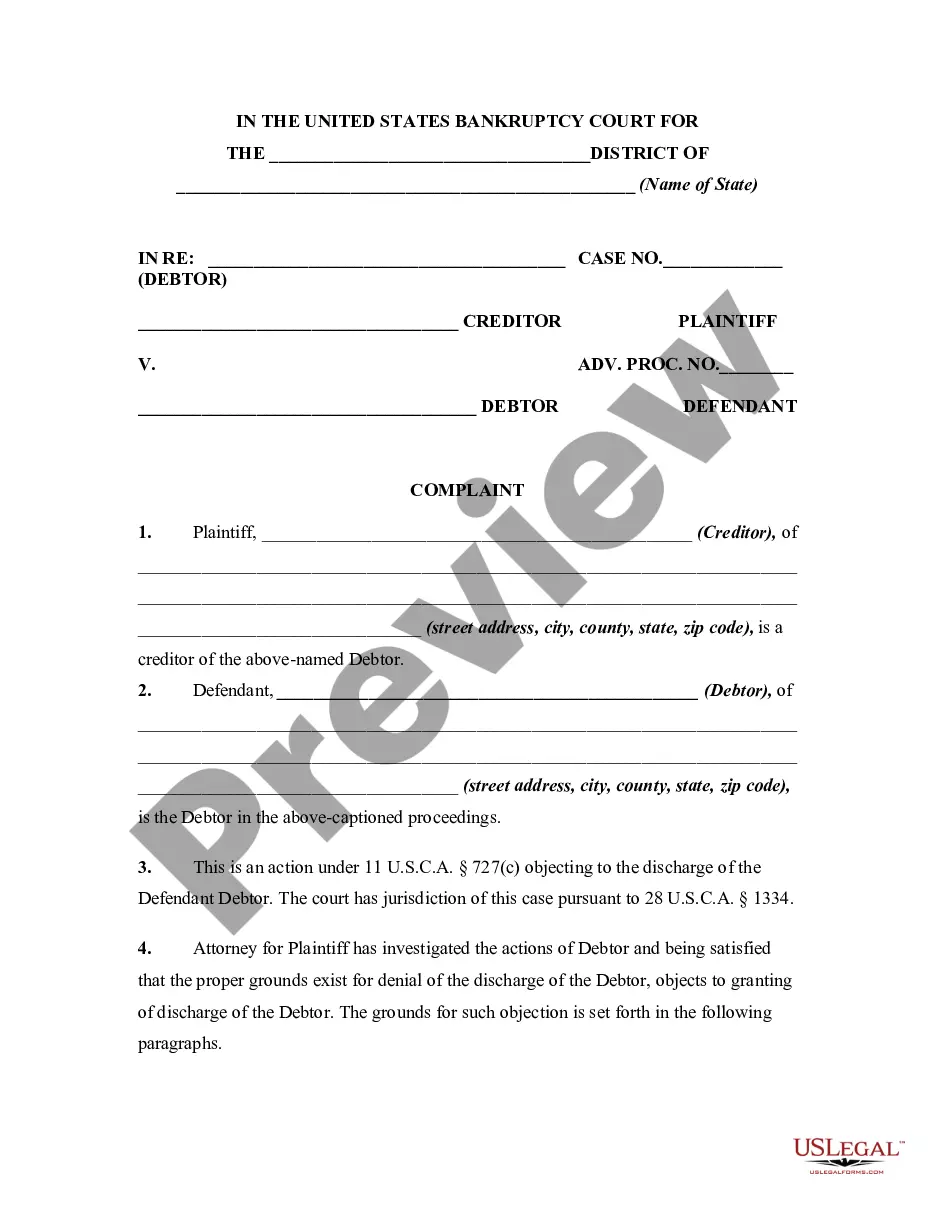

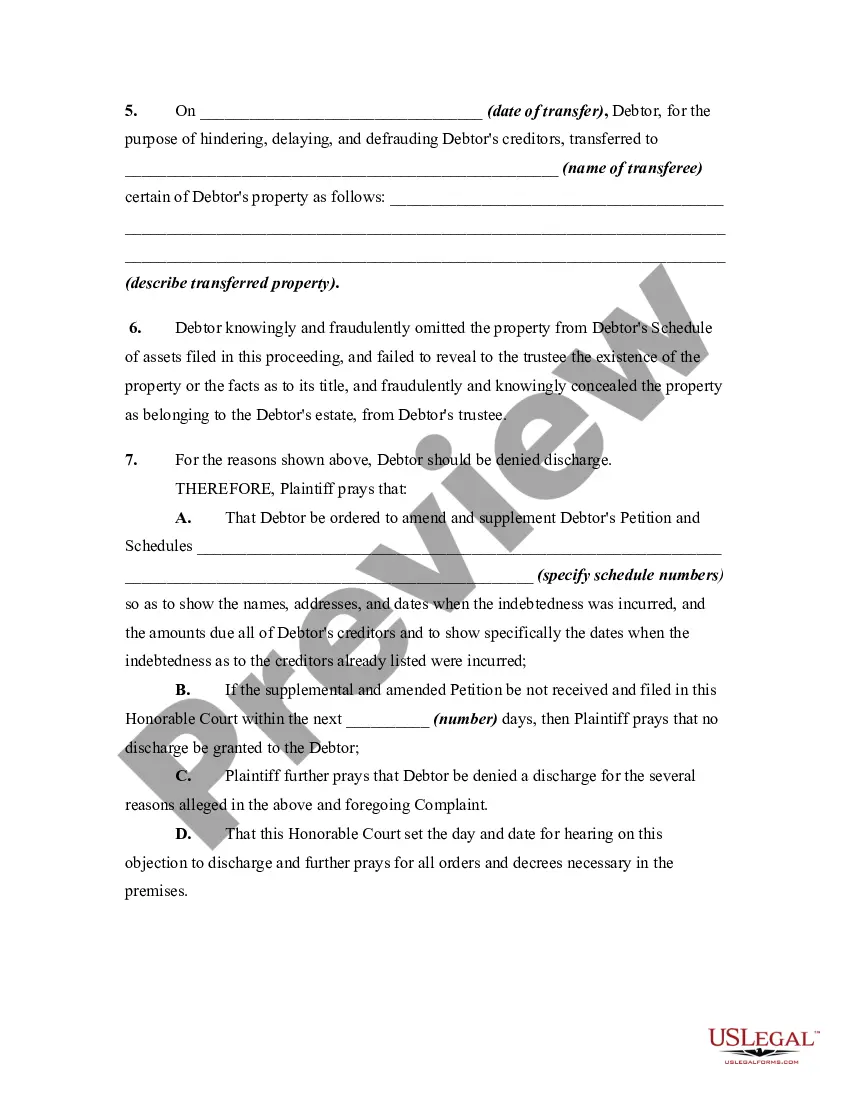

The decree of the bankruptcy court which terminates the bankruptcy proceedings is generally a discharge that releases the debtor from most debts. A bankruptcy court may refuse to grant a discharge under certain conditions.

Bankruptcy Schedules

State:

Multi-State

Control #:

US-01087BG

Format:

Word;

Rich Text

Instant download

Description Bankruptcy Discharge Lawyer

Free preview What Bankruptcy Discharge

How to fill out Objecting Discharge?

Aren't you tired of choosing from numerous templates each time you want to create a Complaint Objecting to Discharge in Bankruptcy Proceedings for Concealment by Debtor and Omitting from Schedules? US Legal Forms eliminates the wasted time millions of Americans spend exploring the internet for suitable tax and legal forms. Our skilled team of lawyers is constantly changing the state-specific Forms catalogue, so it always provides the appropriate files for your scenarion.

If you’re a US Legal Forms subscriber, just log in to your account and click on the Download button. After that, the form may be found in the My Forms tab.

Users who don't have an active subscription should complete simple actions before having the ability to get access to their Complaint Objecting to Discharge in Bankruptcy Proceedings for Concealment by Debtor and Omitting from Schedules:

- Make use of the Preview function and look at the form description (if available) to make sure that it is the appropriate document for what you’re trying to find.

- Pay attention to the applicability of the sample, meaning make sure it's the correct sample for the state and situation.

- Use the Search field at the top of the web page if you want to look for another file.

- Click Buy Now and choose a preferred pricing plan.

- Create an account and pay for the services using a credit card or a PayPal.

- Download your template in a required format to finish, create a hard copy, and sign the document.

Once you have followed the step-by-step instructions above, you'll always have the ability to log in and download whatever document you will need for whatever state you want it in. With US Legal Forms, completing Complaint Objecting to Discharge in Bankruptcy Proceedings for Concealment by Debtor and Omitting from Schedules samples or other legal paperwork is not hard. Get started now, and don't forget to double-check your samples with certified lawyers!