Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale

Overview of this form

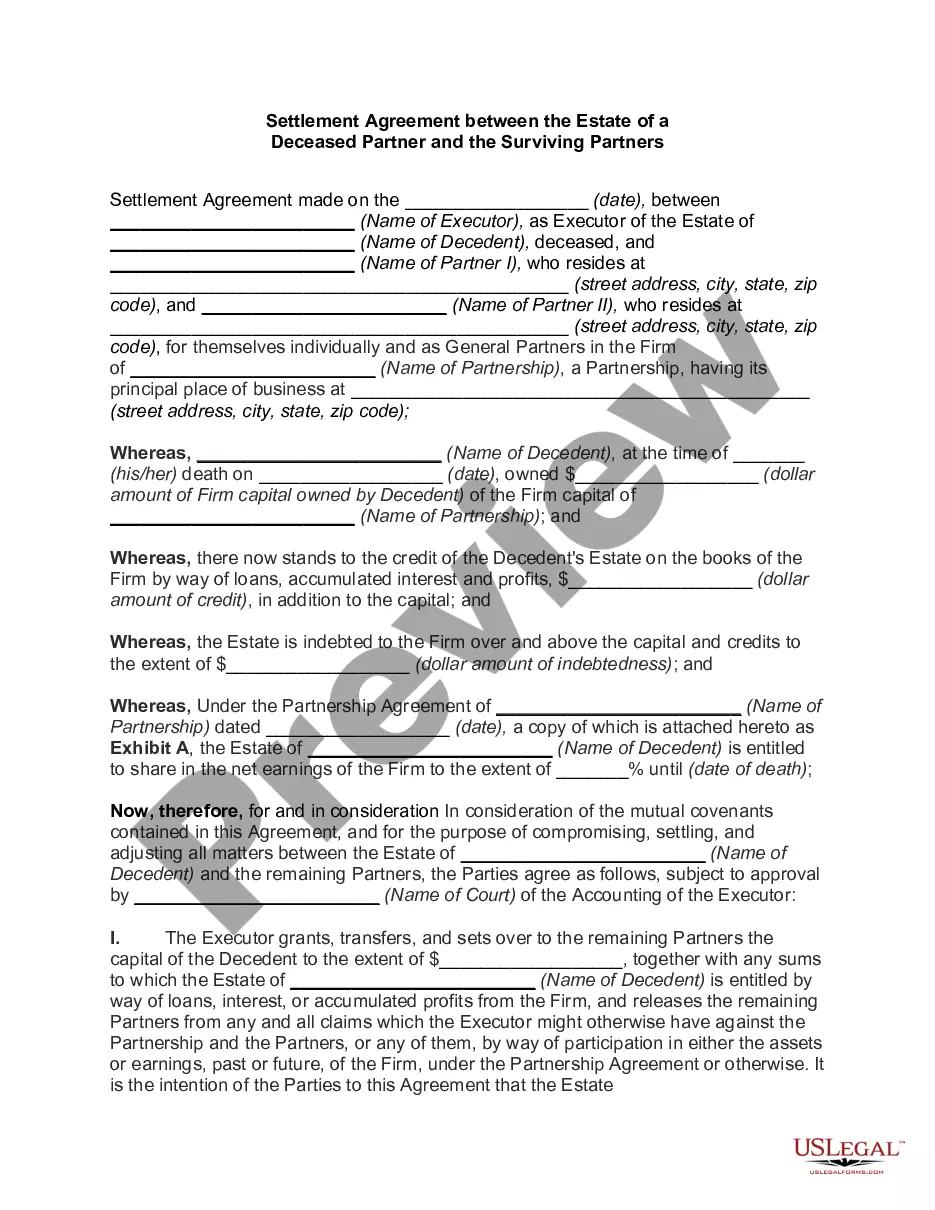

The Sale of Deceased Partner's Interest to Surviving Partner in the form of a Purchase Agreement and Bill of Sale is a legal document used when the estate of a deceased partner sells their share in a partnership to the surviving partner. This form formalizes the transfer of ownership and outlines the obligations of both parties, distinguishing it from other agreements that do not specifically address partnership interests of deceased individuals.

Key components of this form

- Details of the agreement, including the parties involved and the date of the agreement.

- Background information on the partnership and the deceased partner's interest.

- Purchase price and payment terms between the surviving partner and the estate.

- Transfer of partnership assets and right to receive credits.

- Indemnification provisions regarding existing partnership debts.

- Arbitration clause for resolving disputes.

When to use this form

This form is necessary when a partner in a business dies, and their share needs to be sold to the surviving partner. It is particularly relevant when an agreement is required to transfer business interests legally and clearly, ensuring that all financial obligations and rights are documented. This form helps avoid potential conflicts regarding asset distribution and responsibilities after the partner's death.

Intended users of this form

- Executors or administrators of the deceased partner's estate.

- Surviving partners who wish to acquire the deceased partnerâs share in the business.

- Business partners looking to ensure proper legal documentation regarding ownership transitions following a partner's death.

How to complete this form

- Identify the parties involved, including the executor of the estate and the surviving partner.

- Provide the full name of the deceased partner and the details of the partnership agreement.

- Enter the date of the deceased partner's passing and the date of the agreement.

- Specify the purchase price and the payment schedule, including any installment details.

- Ensure all parties sign the agreement to validate the transaction.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, having the signatures notarized can add an additional layer of validity and can help in case of disputes regarding the authenticity of the document.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Not including the date of death of the deceased partner.

- Failing to clearly specify the payment terms and schedules.

- Omitting signatures from critical parties, which can invalidate the agreement.

- Not verifying local laws or regulations that may apply.

Advantages of online completion

- Convenient access to a legally vetted document at any time.

- Editability allows for customization to fit specific partnership situations.

- Reliable framework developed by licensed attorneys to ensure compliance with legal standards.

Legal use & context

- This form is legally binding once completed and signed by all relevant parties.

- It helps clarify the transfer of partnership interest and financial obligations following the death of a partner.

- Ensures that the surviving partner can manage the partnership without interference from the estate.

Key takeaways

- The form formalizes the sale of a deceased partner's interest in a business.

- It is essential for avoiding disputes regarding the partnership after a partner's death.

- Proper completion and execution of the form are crucial for legal enforceability.

Looking for another form?

Form popularity

FAQ

This will produce a capital gain under IRC Section 741. While there are Code sections that could convert the capital gain into ordinary income on the sale of the partnership interests, there is no look through rule that would convert a capital gain into a Section 1231 gain.

The decedent's estate (or other successor, such as a living/revocable trust, depending upon how the deceased partner held their partnership interest; the Estate), will take such interest with an adjusted basis equal to the fair market value of such interest at the date of the partner's death, increased by the

2012 Review Schedule D, Form 8949 and Form 4797 to determine the amount of gain or loss the partner reported on the sale of the partnership interest. After determining a partner sold its interest in the partnership, establish other relevant facts that can impact the tax treatment of this transaction.

Because tax law views a partnership both as an entity and as an aggregate of partners, the sale of a partnership interest may result either in a capital gain or loss or all or a portion of the gain may be taxed as ordinary income.

The simple answer is to debit the selling partner's equity account to zero balance. The selling price would be a credit to the buying partner's equity account. This assumes the buying partner is financing the buyout personally.

To take a loss for abandonment of a partnership interest, a taxpayer must show that in the year the loss deduction was claimed, the taxpayer intended to abandon the partnership interest and that there was an affirmative act of abandonment of the interest.

That could mean the partnership agreement is dissolved immediately upon their death. You will then owe your partner's estate a debt for their share of the partnership that accrues at the date of their death.

Complete Part I and Part II, Items E through I, on each partner's K-1. This is used to provide personal information. Complete Part III of each partner's K-1. Complete the selling partner's K-1. Complete the remaining partners' K-1s.

If a partner's entire interest in a partnership is liquidated or redeemed, he or she recognizes gain to the extent any money or marketable securities received exceeds his or her basis in the partnership interest immediately before the distribution ( Code Sec.