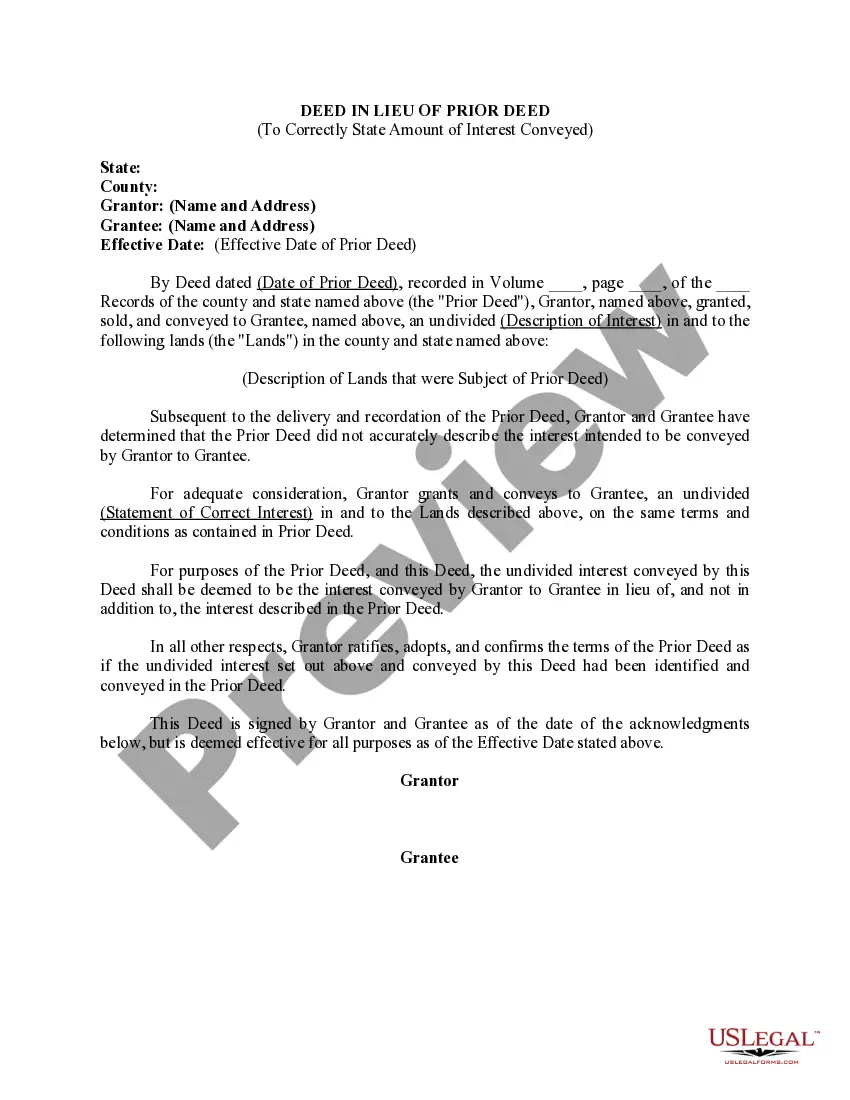

Queens New York Deed in Lieu of Prior Deed to Correctly Identify the Amount of Interest intended to Be Conveyed

Description

How to fill out Queens New York Deed In Lieu Of Prior Deed To Correctly Identify The Amount Of Interest Intended To Be Conveyed?

Preparing legal documentation can be burdensome. Besides, if you decide to ask a lawyer to write a commercial agreement, documents for proprietorship transfer, pre-marital agreement, divorce paperwork, or the Queens Deed in Lieu of Prior Deed to Correctly Identify the Amount of Interest intended to Be Conveyed, it may cost you a fortune. So what is the most reasonable way to save time and money and draft legitimate documents in total compliance with your state and local laws? US Legal Forms is a great solution, whether you're searching for templates for your personal or business needs.

US Legal Forms is the most extensive online collection of state-specific legal documents, providing users with the up-to-date and professionally verified templates for any scenario gathered all in one place. Therefore, if you need the current version of the Queens Deed in Lieu of Prior Deed to Correctly Identify the Amount of Interest intended to Be Conveyed, you can easily find it on our platform. Obtaining the papers takes a minimum of time. Those who already have an account should check their subscription to be valid, log in, and pick the sample by clicking on the Download button. If you haven't subscribed yet, here's how you can get the Queens Deed in Lieu of Prior Deed to Correctly Identify the Amount of Interest intended to Be Conveyed:

- Glance through the page and verify there is a sample for your area.

- Check the form description and use the Preview option, if available, to make sure it's the sample you need.

- Don't worry if the form doesn't suit your requirements - search for the correct one in the header.

- Click Buy Now when you find the required sample and choose the best suitable subscription.

- Log in or register for an account to purchase your subscription.

- Make a transaction with a credit card or via PayPal.

- Opt for the file format for your Queens Deed in Lieu of Prior Deed to Correctly Identify the Amount of Interest intended to Be Conveyed and save it.

Once done, you can print it out and complete it on paper or upload the template to an online editor for a faster and more convenient fill-out. US Legal Forms enables you to use all the documents ever purchased multiple times - you can find your templates in the My Forms tab in your profile. Try it out now!

Form popularity

FAQ

Disadvantages to Lender A lender should also hesitate before accepting a lieu deed where there are outstanding subordinate liens or judgments against the property. In such a situation, the lender will have to foreclose its mortgage, with the attendant expense and time involved to obtain clear title.

At closing, the seller signs a deed transferring title to the buyer/borrower. The buyer/borrower signs a promissory note, which obligates him or her to make payments to the lender, and a security instrument, such as a deed of trust, which conveys an interest in the property to the lender.

Your Credit Score Will Drop While it's a commonly-held belief that short sales and deeds in lieu of foreclosure have less of a negative impact on credit scores than foreclosure, in reality, the effect is basically the same.

inlieu of foreclosure is an arrangement where you voluntarily turn over ownership of your home to the lender to avoid the foreclosure process. inlieu of foreclosure may help you avoid being personally liable for any amount remaining on the mortgage.

It costs more to the lender to go through the foreclosure process. During a short sale, the lender shares the cost with the homeowner to quickly sell the home. From a financial standpoint, many lenders prefer a short sale if the home is not expected to sell for more than the balance due at the foreclosure auction.

Less damage to your credit: A deed in lieu agreement stays on your credit report for 4 years while a foreclosure sticks around for 7 years. Taking a deed in lieu agreement can allow you to buy a new home sooner than if you were to go through a foreclosure.

After a deed-in-lieu of foreclosure, your credit score may drop by a range of 50 to 125 points, depending on where it stood before the deed-in-lieu, according to FICO data. The impact isn't as severe as a foreclosure filing, though, which may drop your credit score by as much as 160 points.

A deed in lieu can eliminate your deficiency if you owe more on your home than the home is worth. In exchange for giving the lender your deed voluntarily and keeping the home in good condition, your lender may agree to forgive your deficiency or greatly reduce it.

A deed in lieu of foreclosure still has a negative impact on the borrower's total credit rating. The greatest risk to a lender making a real estate loan is that a property pledged as collateral will be abandoned by the borrower.

If you're behind in your mortgage payments and facing a foreclosure, you might be thinking about different options, like giving up your home with a deed in lieu of foreclosure or filing for bankruptcy. With either one of these options, your credit scores will drop.