Cuyahoga Ohio Qualified Written RESPA Request to Dispute or Validate Debt

Description

How to fill out Qualified Written RESPA Request To Dispute Or Validate Debt?

Drafting legal documents can be challenging.

Moreover, if you opt to hire a lawyer to create a business agreement, ownership transfer paperwork, prenuptial contract, divorce documents, or the Cuyahoga Qualified Written RESPA Request to Challenge or Verify Debt, it might cost you a significant sum.

Browse the page to confirm there is a sample for your location.

- What is the most effective way to conserve time and finances while generating valid documents that comply with state and local laws.

- US Legal Forms is a superb option, whether you require templates for personal or commercial purposes.

- US Legal Forms boasts the largest online collection of state-specific legal documents, offering users the latest and professionally reviewed templates for any situation, all conveniently located in one place.

- Consequently, if you're in need of the updated version of the Cuyahoga Qualified Written RESPA Request to Challenge or Verify Debt, you can readily find it on our platform.

- Acquiring the documents takes minimal time.

- Users who already possess an account should ensure their subscription is active, Log In, and select the sample using the Download button.

- If you have not yet subscribed, here’s how you can obtain the Cuyahoga Qualified Written RESPA Request to Challenge or Verify Debt.

Form popularity

FAQ

If you don't receive a validation notice within 10 days of the first contact, request one from the debt collector the next time you're contacted. Ask for the debt collector's mailing address at this time as well, in case you decide to request a debt verification letter.

Debt collectors are legally required to send one within five days of first contact. You have within 30 days from receiving a debt validation letter to send a debt verification letter. Here's the important part: You have just 30 days to respond to a debt validation letter with your debt verification letter.

What Happens Now? If a debt collector can't verify your debt, then they must stop contacting you about it. And they have to let credit bureaus know so they can remove the debt from your credit report.

Failing to respond to a Debt Validation Letter while continuing to collect on the debt is a direct violation of the FDCPA. You can report a debt collector's failure to respond to your state's attorney general, the Consumer Financial Protection Bureau (CFPB), or the FTC.

If a debt collector fails to verify the debt but continues to go after you for payment, you have the right to sue that debt collector in federal or state court. You might be able to get $1,000 per lawsuit, plus actual damages, attorneys' fees, and court costs.

If a debt collector fails to verify the debt but continues to go after you for payment, you have the right to sue that debt collector in federal or state court. You might be able to get $1,000 per lawsuit, plus actual damages, attorneys' fees, and court costs.

If you get a summons notifying you that a debt collector is suing you, don't ignore it. If you do, the collector may be able to get a default judgment against you (that is, the court enters judgment in the collector's favor because you didn't respond to defend yourself) and garnish your wages and bank account.

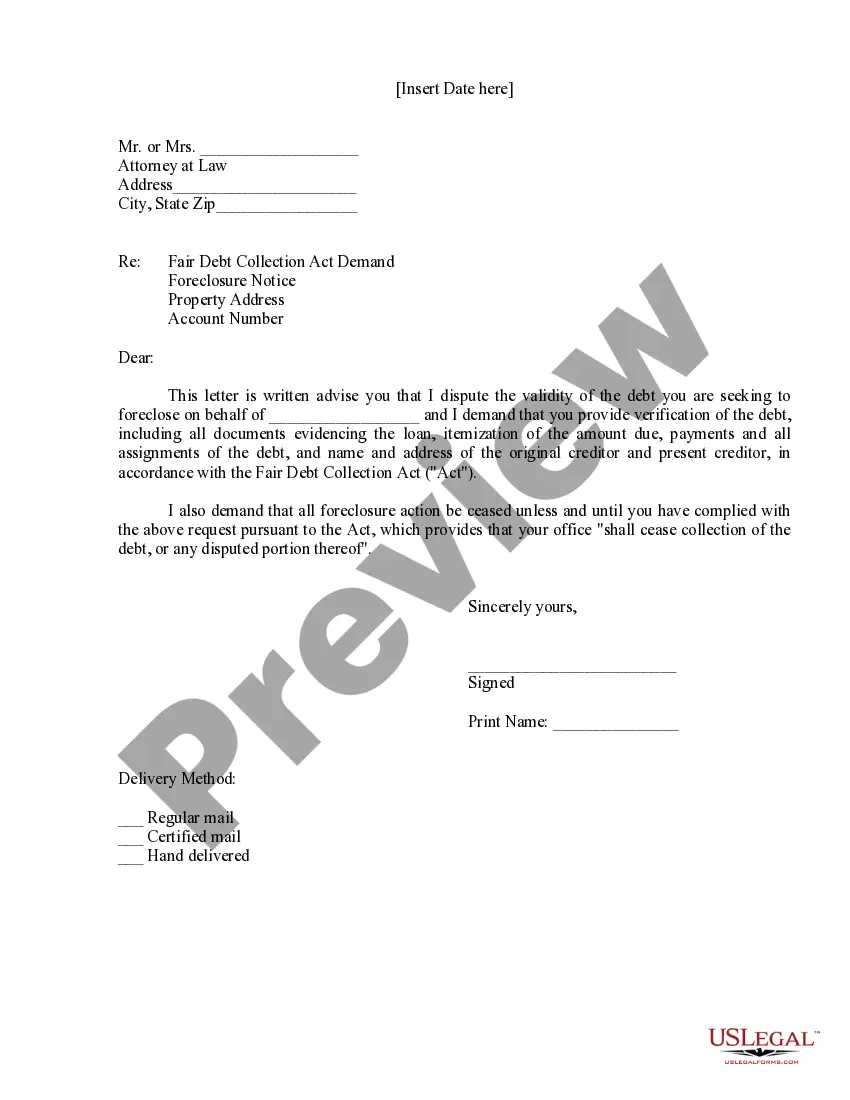

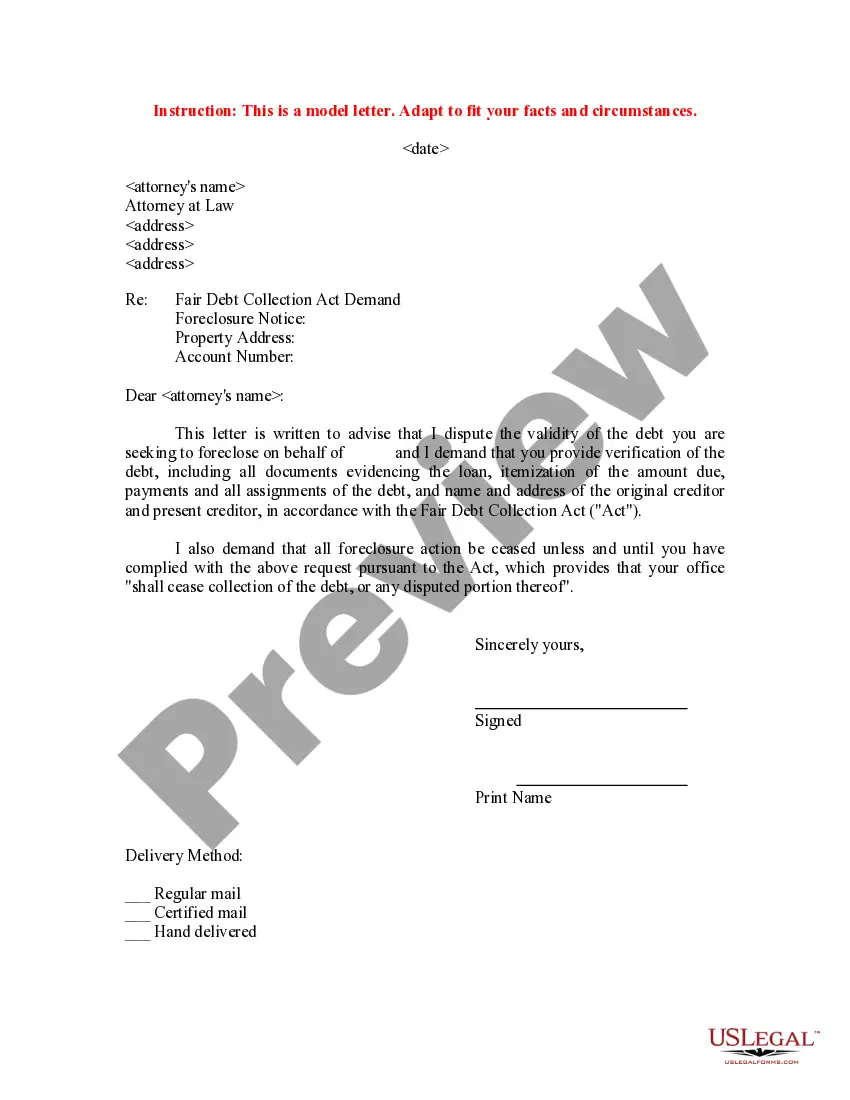

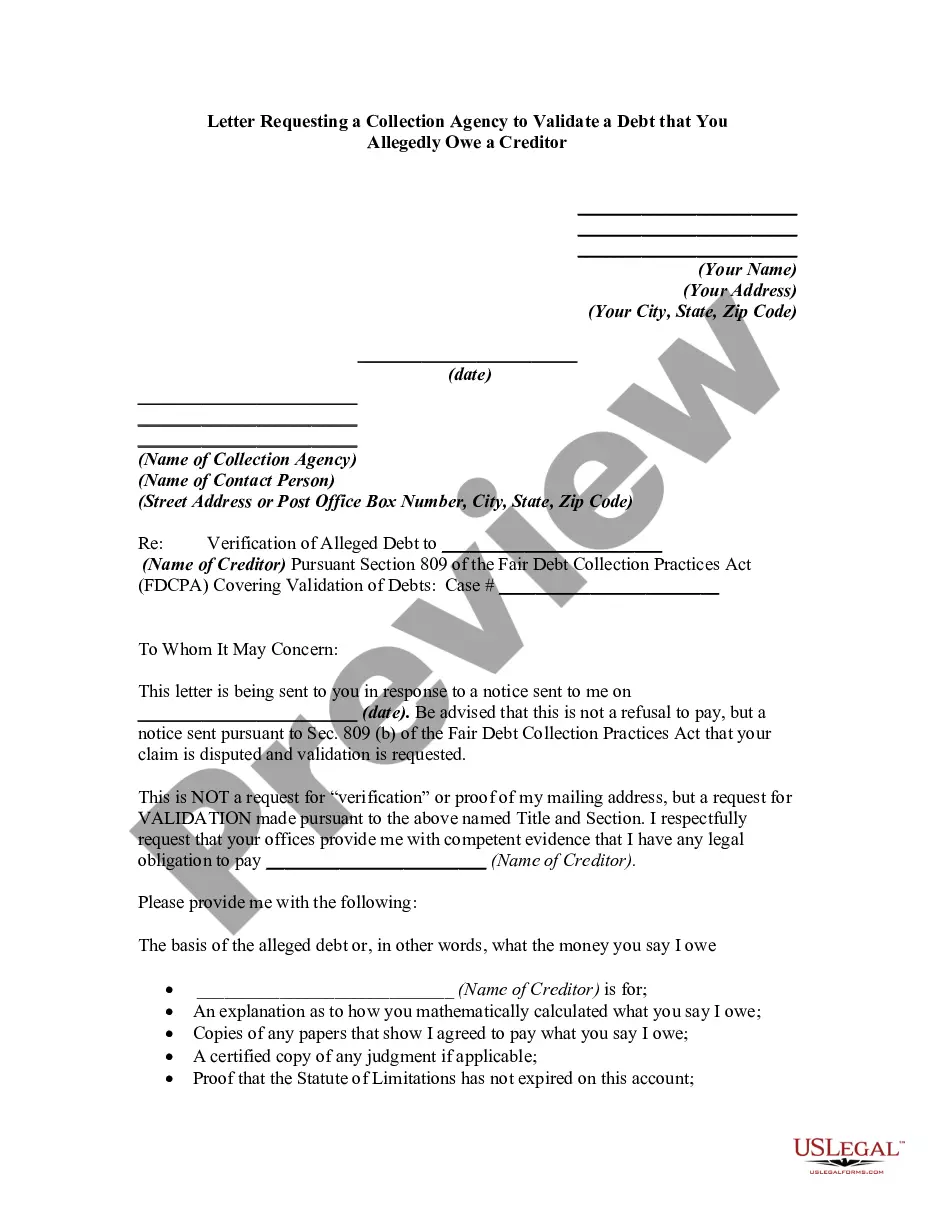

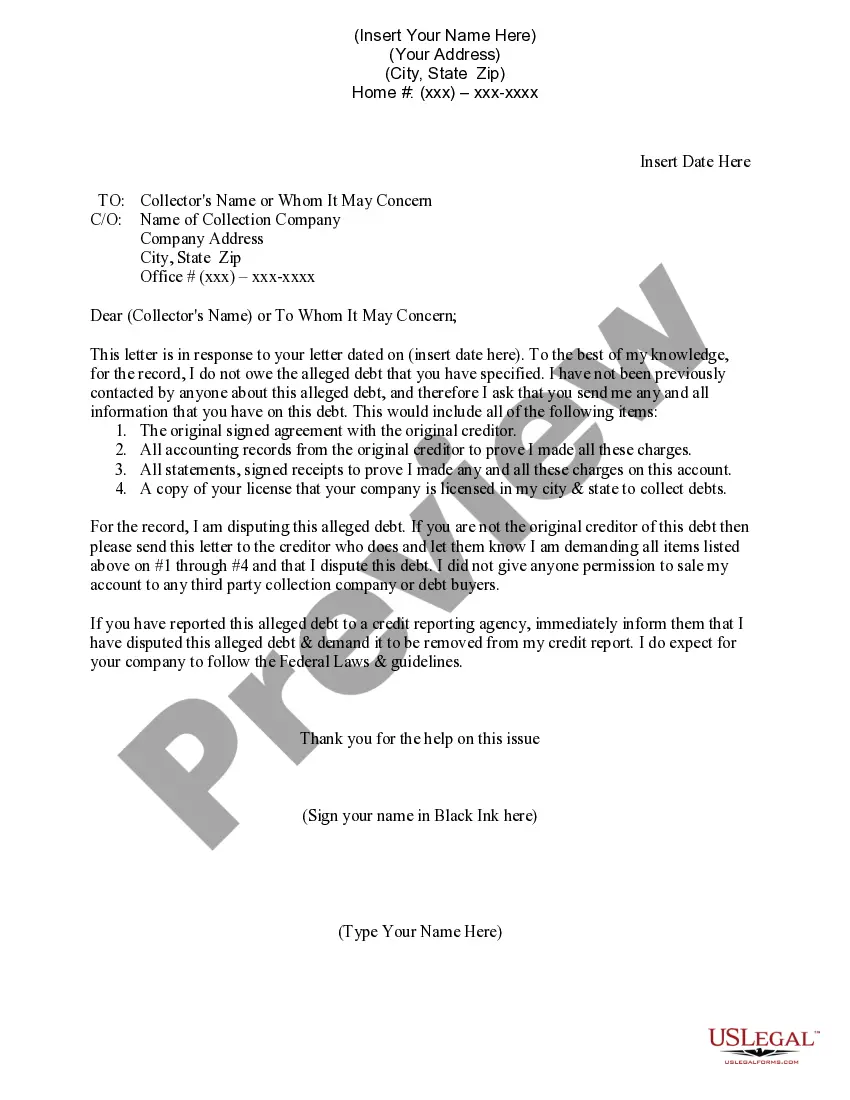

You can request that a collection agency verify the amount and validity of a debt. But you must act quickly. One of the most powerful tools you have under the federal Fair Debt Collection Practices Act (FDCPA) is to require that a debt collector verify the amount and validity of the debt it's trying to collect.

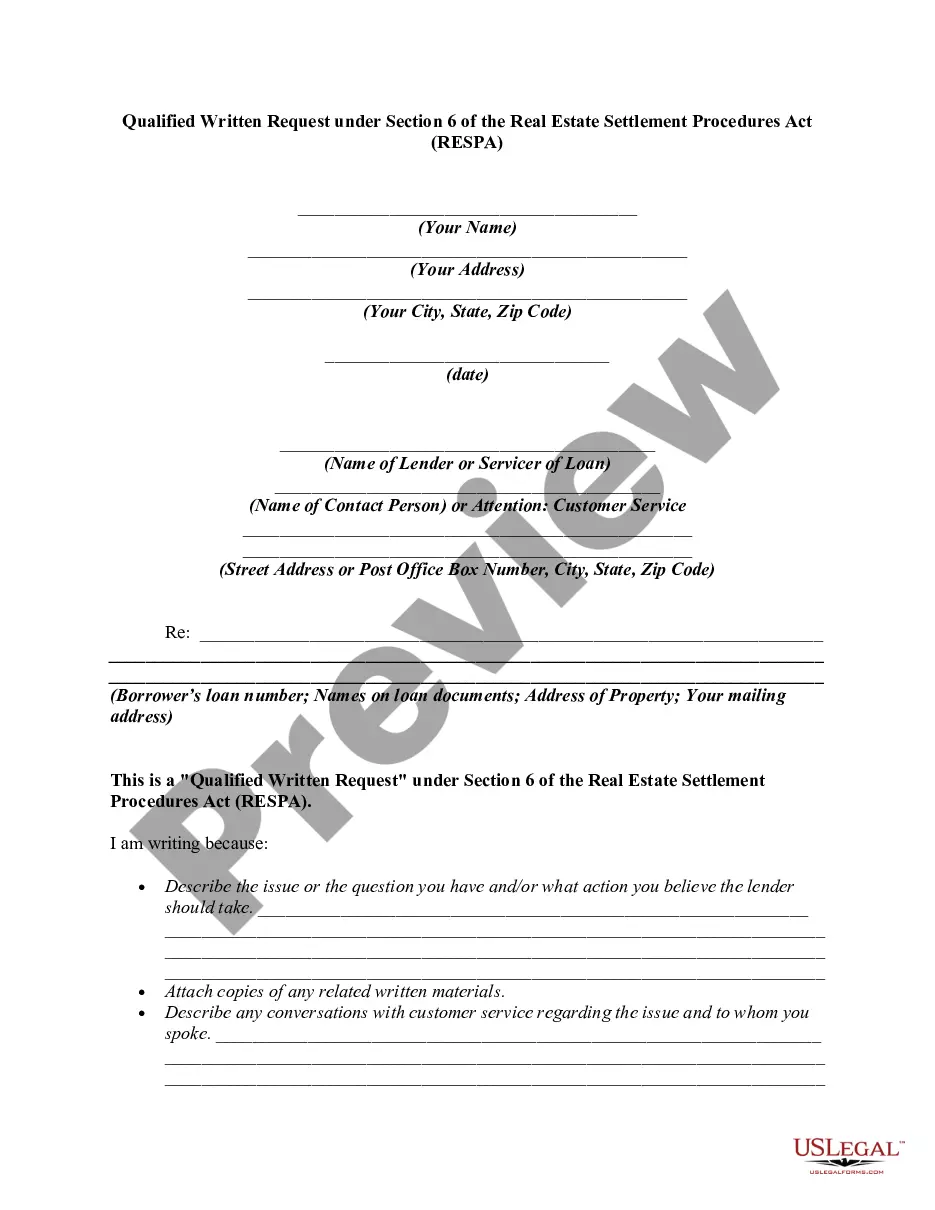

A qualified written request, or QWR, is a written letter sent to the servicer that: requests information about the loan (called a "request for information" under RESPA), and/or. asks that the servicer correct an error (a "notice of error").

I am requesting that you provide verification of this debt. Please send the following information: The name and address of the original creditor, the account number, and the amount owed. Verification that there is a valid basis for claiming I am required to pay the current amount owed.