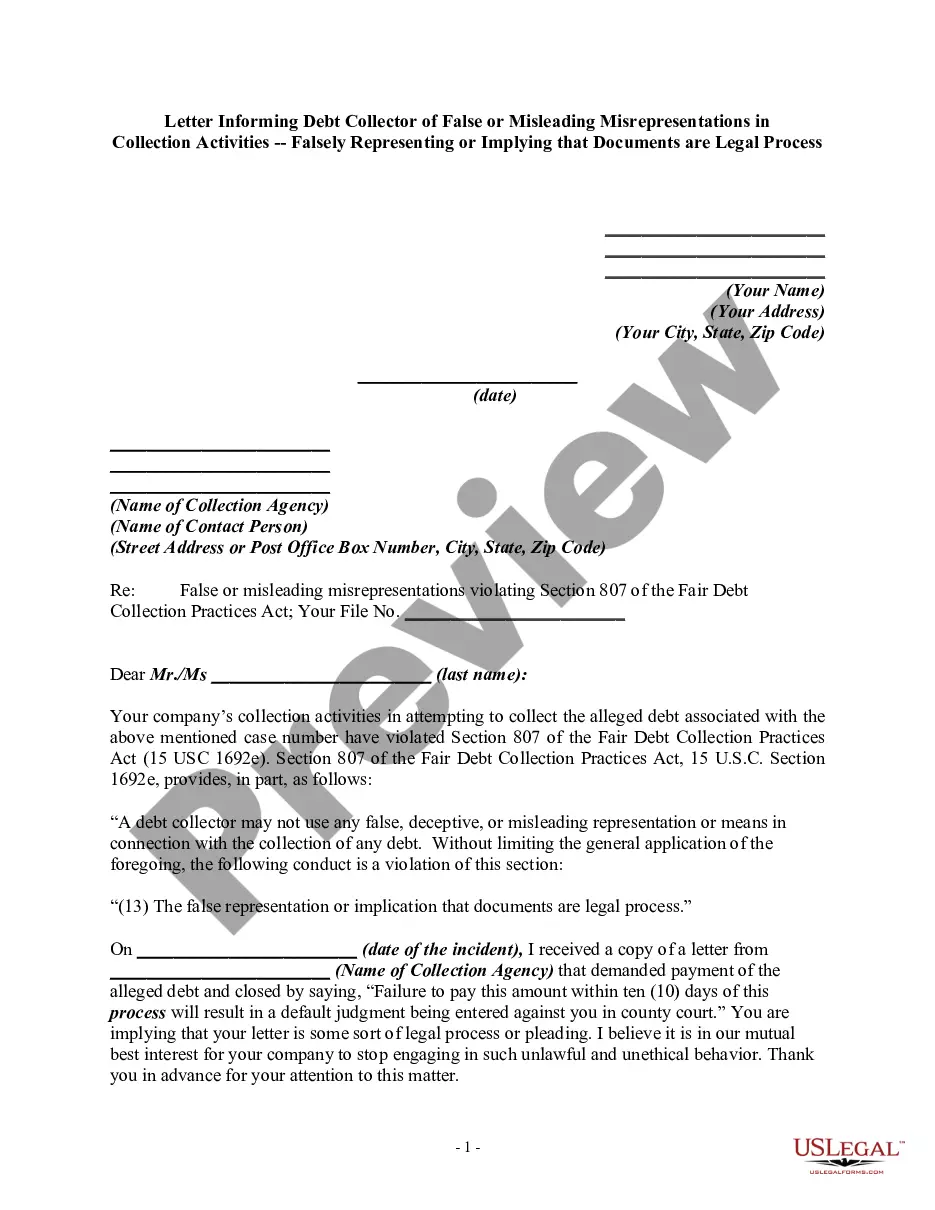

A debt collector may not use any false, deceptive, or misleading representation or means in connection with the collection of a debt. This includes falsely representing or implying that documents are legal process.

Dallas Texas Notice to Debt Collector - Falsely Representing a Document is Legal Process

Category:

State:

Multi-State

County:

Dallas

Control #:

US-DCPA-40

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Falsely Representing A Document Is Legal Process?

Drafting legal documents can be tedious. Additionally, if you opt to hire a lawyer to create a business contract, paperwork for ownership transfer, prenuptial agreement, divorce documents, or the Dallas Notice to Debt Collector - Misrepresenting a Document as Legal Process, it may be very expensive. So, what is the most sensible way to conserve time and funds while preparing valid forms in complete accordance with your state and local regulations.

US Legal Forms is a superb answer, whether you are looking for templates for personal or commercial purposes.

Don't fret if the form doesn’t meet your needs - search for the appropriate one in the header. Click Buy Now when you find the necessary template and select the most suitable subscription. Log In or create an account to purchase your subscription. Complete the transaction using a credit card or via PayPal. Choose the document format for your Dallas Notice to Debt Collector - Misrepresenting a Document as Legal Process and download it. After that, you can print it out and fill it out by hand or upload the samples to an online editor for a quicker and more convenient completion. US Legal Forms allows you to utilize all documents previously obtained multiple times - you can access your templates in the My documents section in your profile. Try it out today!

- US Legal Forms is the largest online repository of state-specific legal documents, offering users the latest and professionally confirmed forms for any situation all in one location.

- Consequently, if you require the latest edition of the Dallas Notice to Debt Collector - Misrepresenting a Document as Legal Process, you can quickly find it on our platform.

- Acquiring the documents takes minimal time.

- Users with an existing account should confirm their subscription is active, Log In, and select the template via the Download button.

- If you haven’t signed up yet, here is how you can obtain the Dallas Notice to Debt Collector - Misrepresenting a Document as Legal Process.

- Browse the page and ensure there is a template for your region.

- Review the form description and utilize the Preview option, if available, to make sure it’s the template you are looking for.

Form popularity

FAQ

Can You Sue a Company for Sending You to Collections? Yes, the FDCPA allows for legal action against certain collectors that don't comply with the rules in the law. If you're sent to collections for a debt you don't owe or a collector otherwise ignores the FDCPA, you might be able to sue that collector.

The answer is yes, but the process is not as simple as collection agencies make it seem. Collection agencies have the right to take you to court if you haven't paid your overdue bills, but the likelihood of them acting on that right is low, especially if you don't have an income that can be garnished or own any assets.

Debt collectors are generally prohibited under federal law from using any false, deceptive, or misleading misrepresentation in collecting a debt. The federal law that prohibits this is called the Fair Debt Collection Practices Act (FDCPA).

Here are a few suggestions that might work in your favor: Write a letter disputing the debt. You have 30 days after receiving a collection notice to dispute a debt in writing.Dispute the debt on your credit report.Lodge a complaint.Respond to a lawsuit.Hire an attorney.

Once you're on a debt collector's radar, it can become a full-time job trying to dodge them. Yes, debt collectors have a right to their money. But they don't have a right to harass you or your family, garnish your wages, arrest you, threaten you, or break the law in any way to get what they're due.

By law, a debt collector is not allowed to threaten or use physical force of any kind towards you, any member of your family or a third party connected to you to try and collect your debt. They can, however, contact a family member, friend of third party to obtain location information on you.

You may bring a lawsuit against the debt collector in state court. In the lawsuit, you must prove that the debt collector violated the FDCPA. If successful, you might be able to collect $1,000 in statutory damages, and possibly more if you suffered harm from the violations.

Debt collectors have restrictions on how they can pursue you for payment, but they are allowed to sue you....2. Harass you Repeated calls. Threats of violence. Publishing information about you. Abusive or obscene language.

Plan and modify arrangements with them and the creditor. Organise a settlement offer with you that may make it easier to pay off the debt. Sell your debt to another company who will have the same arrangements and powers as the original creditor. Obtain an order from a court to repossess some of your property.

Ignoring or avoiding the debt collector may cause the debt collector to use other methods to try to collect the debt, including a lawsuit against you. If you are unable to come to an agreement with a debt collector, you may want to contact an attorney who can provide you with legal advice about your situation.