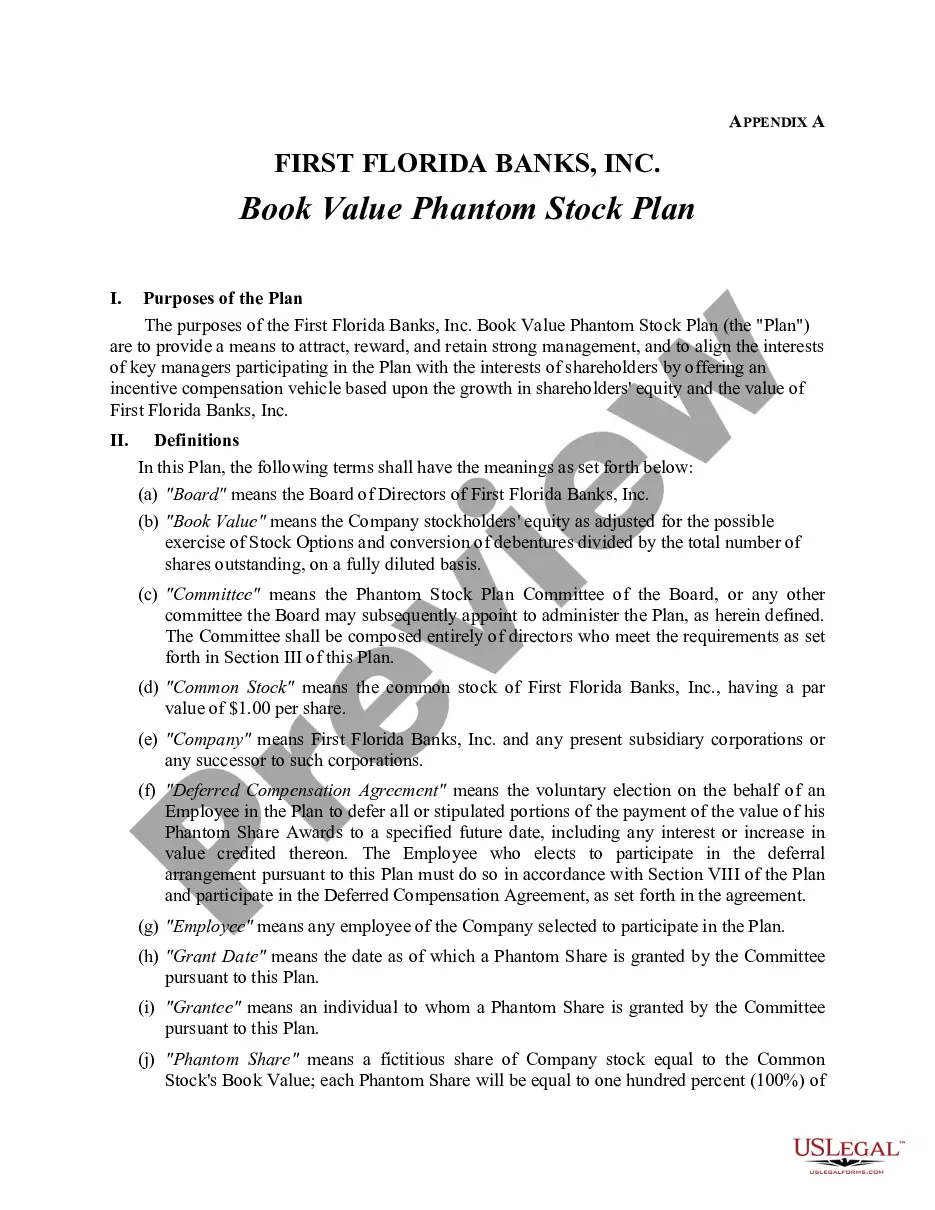

Salt Lake Utah Proposed book value phantom stock plan with appendices for First Florida Bank, Inc.

Description

How to fill out Proposed Book Value Phantom Stock Plan With Appendices For First Florida Bank, Inc.?

Are you aiming to swiftly generate a legally-enforceable Salt Lake Proposed book value phantom stock plan with appendices for First Florida Bank, Inc. or perhaps any other document to manage your personal or business affairs? You have two alternatives: engage a legal professional to compose a valid document for you or produce it entirely by yourself. Fortunately, there's a third option - US Legal Forms. It will assist you in obtaining well-crafted legal documents without incurring exorbitant fees for legal services.

US Legal Forms provides an extensive collection of over 85,000 state-specific document templates, including Salt Lake Proposed book value phantom stock plan with appendices for First Florida Bank, Inc. and form sets. We offer templates for a multitude of purposes: ranging from divorce documentation to real estate document templates. We've been operational for more than 25 years and have established a solid reputation among our clientele. Here's how you can join them and procure the required template without any additional difficulties.

If you've already established an account, you can conveniently Log In to it, locate the Salt Lake Proposed book value phantom stock plan with appendices for First Florida Bank, Inc. template, and download it. To re-download the form, simply navigate to the My documents tab.

It's straightforward to locate and download legal forms if you utilize our services. Moreover, the templates we supply are vetted by industry professionals, which enhances your confidence when managing legal issues. Try US Legal Forms today and experience it for yourself!

- First, carefully confirm if the Salt Lake Proposed book value phantom stock plan with appendices for First Florida Bank, Inc. is suitable for your state's or county's regulations.

- If the document includes a description, ensure to verify what it's intended for.

- Initiate the searching process again if the form isn’t what you were looking for by utilizing the search box in the header.

- Choose the subscription that is most appropriate for your requirements and proceed to the payment.

- Pick the file format you wish to receive your document in and download it.

- Print it, fill it out, and sign on the designated line.

Form popularity

FAQ

The answer involves two variables: (a) the presumed value of the company, and (b) the number of shares to be used in the plan. Once these two answers are known, the phantom share price is calculated as the former (the value) divided by the latter (the number of shares).

Phantom stock can, but usually does not, pay dividends. When the grant is initially made, there is no tax impact. When the payout is made, however, it is taxed as ordinary income to the grantee and is deductible to the employer.

A phantom stock plan is an employee benefit plan that gives selected employees (senior management) many of the benefits of stock ownership without actually giving them any company stock. This type of plan is sometimes referred to as shadow stock. Rather than getting physical stock, the employee receives mock stock.

The phantom stock becomes a liability that the company must eventually convert to either cash or company stock. In privately held businesses, company stock is rarely an option. employees like these plans as any phantom stock they receive is not taxable until converted into cash by the company.

Since phantom shares are not the same as real stock, you don't have to worry about employees voting down key decisions, such as selling the company.

Phantom stock plans do not result in shareholder dilution because actual shares are not being transferred. Employees do not become owners. Instead, they are potential cash beneficiaries in the underlying company value.

A phantom stock plan is a deferred compensation plan that awards the employee a unit measured by the value of a share of a company's common stock, or, in the case of a limited liability company, by the value of an LLC unit. However, unlike actual stock, the award does not confer equity ownership in the company.

Phantom stock is not a good idea if the company is planning on issuing them to most or all employees, especially if the shares will be paid out when the employee leaves the company or retires. In that case, phantom shares may be ruled illegal because of the Employee Retirement Income and Security Act (ERISA).

The answer involves two variables: (a) the presumed value of the company, and (b) the number of shares to be used in the plan. Once these two answers are known, the phantom share price is calculated as the former (the value) divided by the latter (the number of shares).

Phantom stock plans can be a valuable method for companies that seek to tie incentive compensation to increases or decreases in company value without awarding actual shares of company stock.