Suffolk New York Statement of Current Monthly Income and Disposable Income Calculation for Use in Chapter 13 - Post 2005

Description

How to fill out Statement Of Current Monthly Income And Disposable Income Calculation For Use In Chapter 13 - Post 2005?

Navigating legal documents is essential in the modern era. However, you don't always have to seek expert help to generate some of them from scratch, such as the Suffolk Statement of Current Monthly Income and Disposable Income Calculation for Use in Chapter 13 - Post 2005, utilizing a service like US Legal Forms.

US Legal Forms boasts over 85,000 templates to choose from across various categories, including living wills, real estate documents, and divorce papers. All templates are categorized by their appropriate state, simplifying the search process. Additionally, you can find educational materials and guides on the site to facilitate any tasks related to completing documents.

Here’s how to acquire and download the Suffolk Statement of Current Monthly Income and Disposable Income Calculation for Use in Chapter 13 - Post 2005.

If you're already a subscriber to US Legal Forms, you can find the required Suffolk Statement of Current Monthly Income and Disposable Income Calculation for Use in Chapter 13 - Post 2005, Log In to your account, and download it. Naturally, our platform cannot fully substitute for an attorney. If you’re faced with a particularly complex situation, we recommend seeking the assistance of a lawyer to review your form before signing and filing it.

With over 25 years in the industry, US Legal Forms has become a preferred resource for numerous legal forms among millions of clients. Join them today and effortlessly obtain your state-compliant documents!

- Review the document's preview and description (if available) to gather general information on what you’ll receive after downloading the template.

- Confirm that the form you choose is tailored to your state/county/area since state regulations can influence the validity of certain records.

- Consider similar forms or restart your search to find the correct document.

- Click Buy now and create your account. If you already possess one, select to Log In.

- Choose the option, then an appropriate payment method, and purchase the Suffolk Statement of Current Monthly Income and Disposable Income Calculation for Use in Chapter 13 - Post 2005.

- Decide to save the form template in any format available.

- Visit the My documents section to download the document again.

Form popularity

FAQ

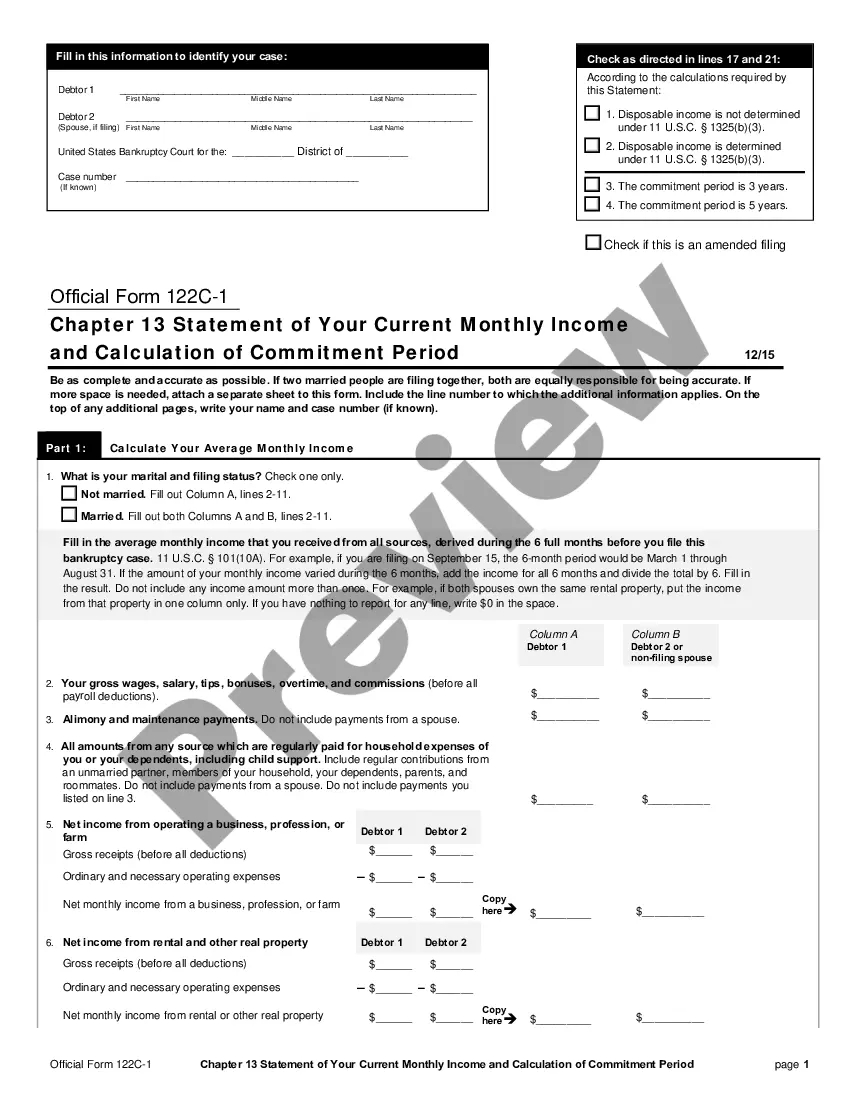

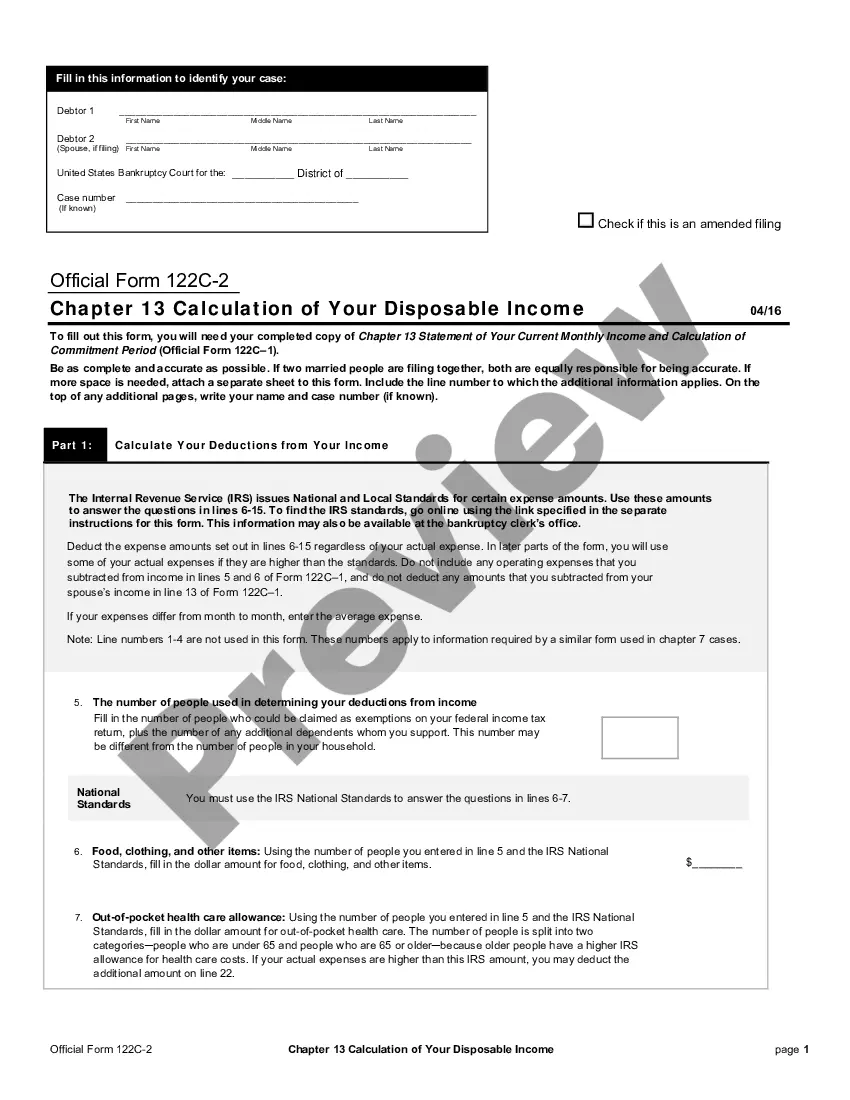

In chapter 13, "disposable income" is income (other than child support payments received by the debtor) less amounts reasonably necessary for the maintenance or support of the debtor or dependents and less charitable contributions up to 15% of the debtor's gross income.

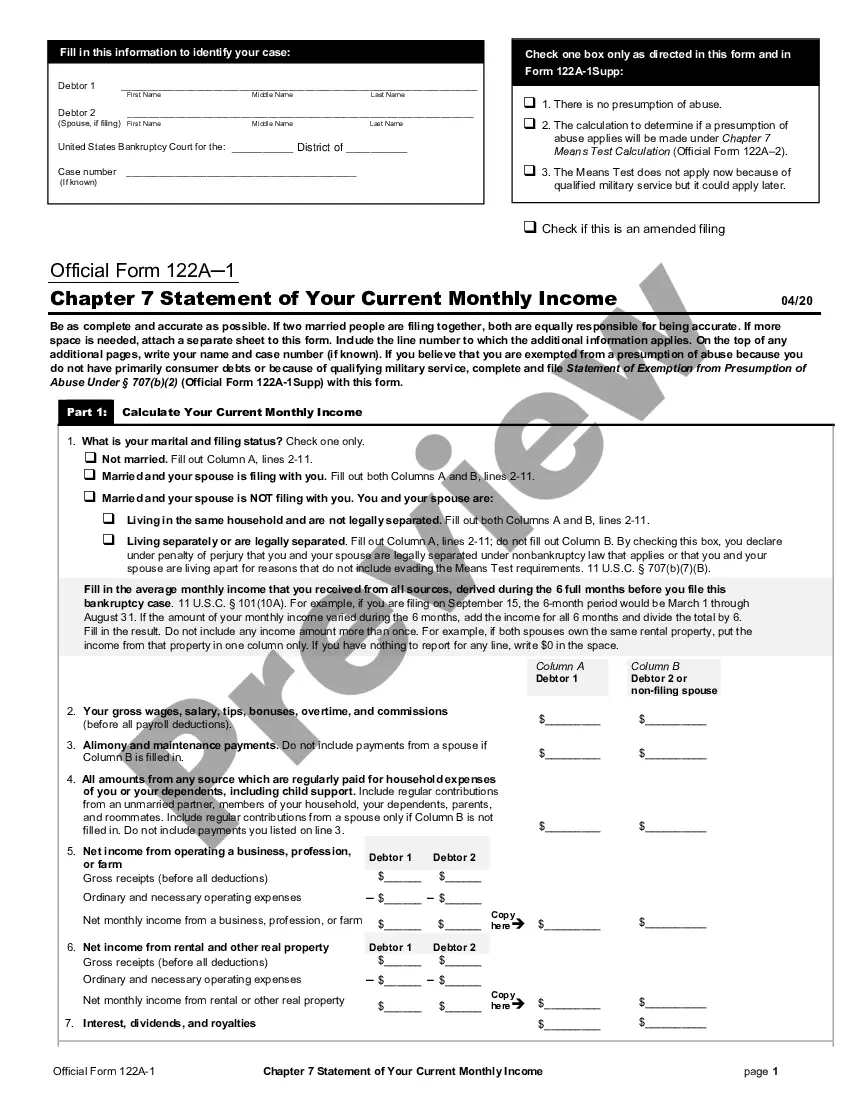

When you file for Chapter 13 bankruptcy, there is no "means test" to determine whether your income is too high. In fact, opposite forces are at work in Chapter 13 -- if your income is so low that you cannot fund a repayment plan, you won't be eligible for Chapter 13.

Certain family and household expenses might help you pass the means test for Chapter 7 bankruptcy. If your income is higher than your state's median income for a similar size household, you must complete the entire bankruptcy means test form to determine whether you qualify for Chapter 7 bankruptcy.

Requirements to File for Chapter 13 Bankruptcy When you file for Chapter 13 bankruptcy, there is no "means test" to determine whether your income is too high. In fact, opposite forces are at work in Chapter 13 -- if your income is so low that you cannot fund a repayment plan, you won't be eligible for Chapter 13.

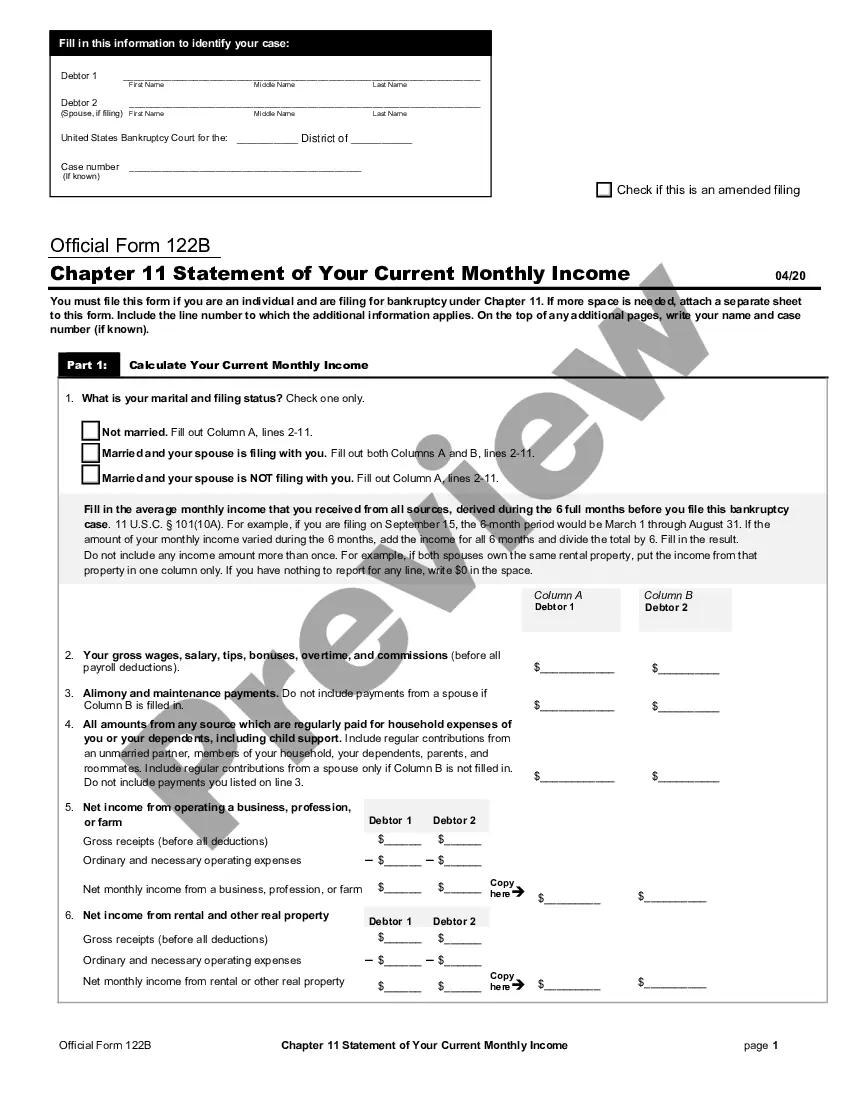

To determine your current monthly income in Chapter 13 bankruptcy, you take your average monthly income for the six-month period prior to filing for bankruptcy.

A 100% plan is a Chapter 13 bankruptcy in which you develop a plan with your attorney and creditors to pay back your debt. It is required to pay back all secured debt and 100% of all unsecured debt.

How Does the Chapter 7 Means Test Work? The means test limits the use of Chapter 7 bankruptcy to those who can't pay their debts by testing whether you have enough income to repay creditors. If you don't, you'll pass.

The means test is calculated by comparing the debtor's average income for the past six months (current monthly income), annualized, to the median income for households of the same size in the debtor's state of residence.

Either way, once you get your discharge in a Chapter 7 bankruptcy or a Chapter 13 bankruptcy, you will get credit again and be able to increase your score. Lenders will look at your credit histories such as on-time payments and debt to income ratio to determine if they should extend credit to you.

The means test measures several things, including: whether your income is less than your state's median income. whether you have disposable income available to pay back some or all of your debt in a Chapter 13 case, and.