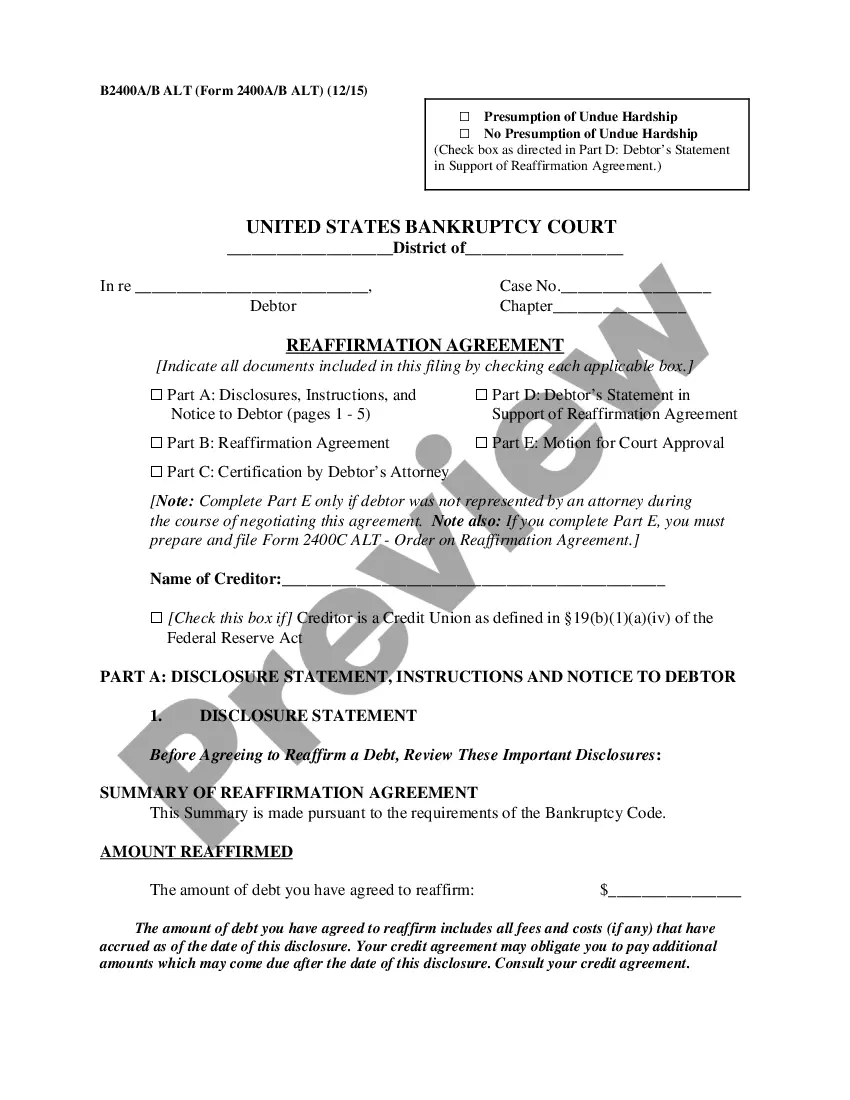

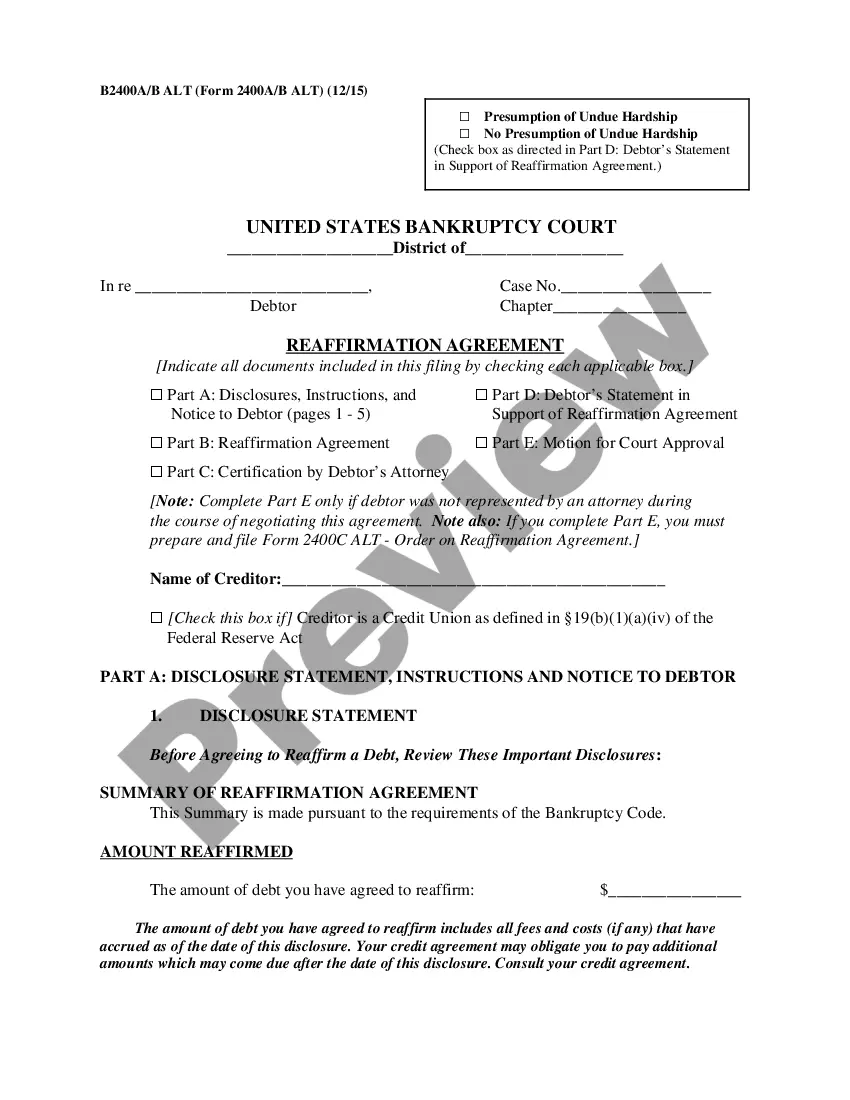

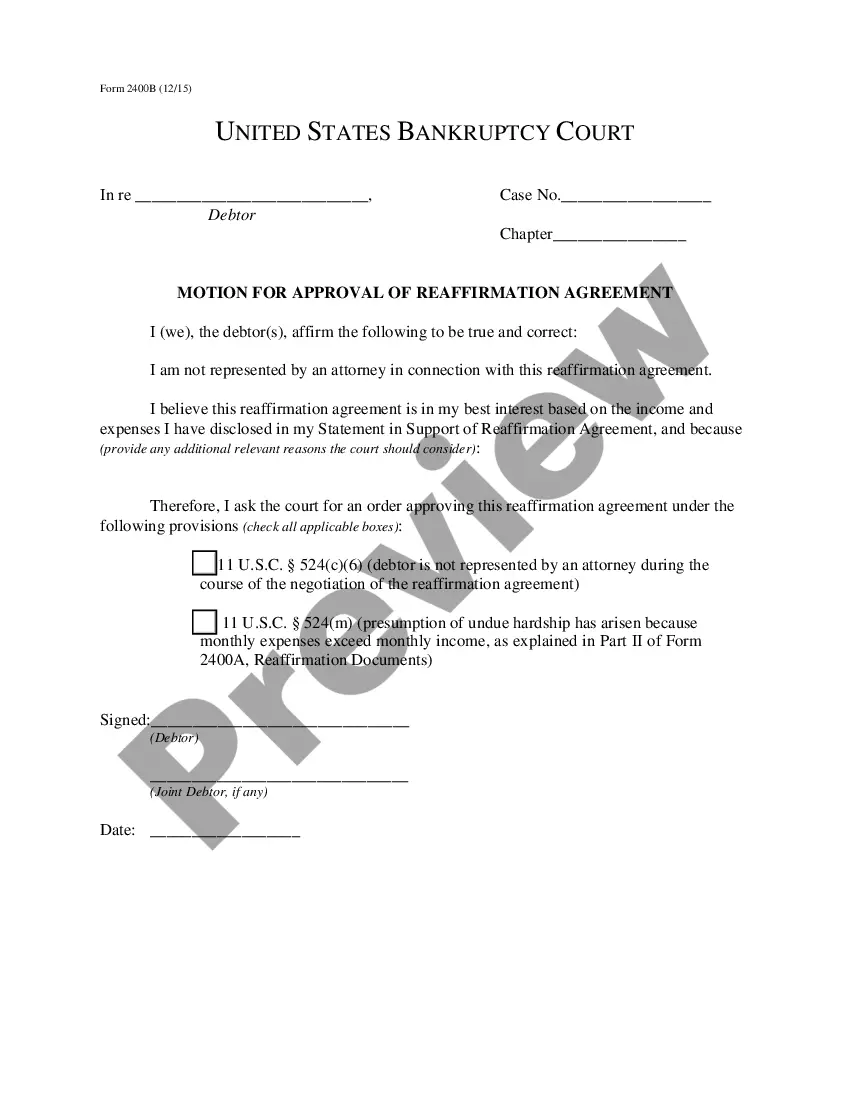

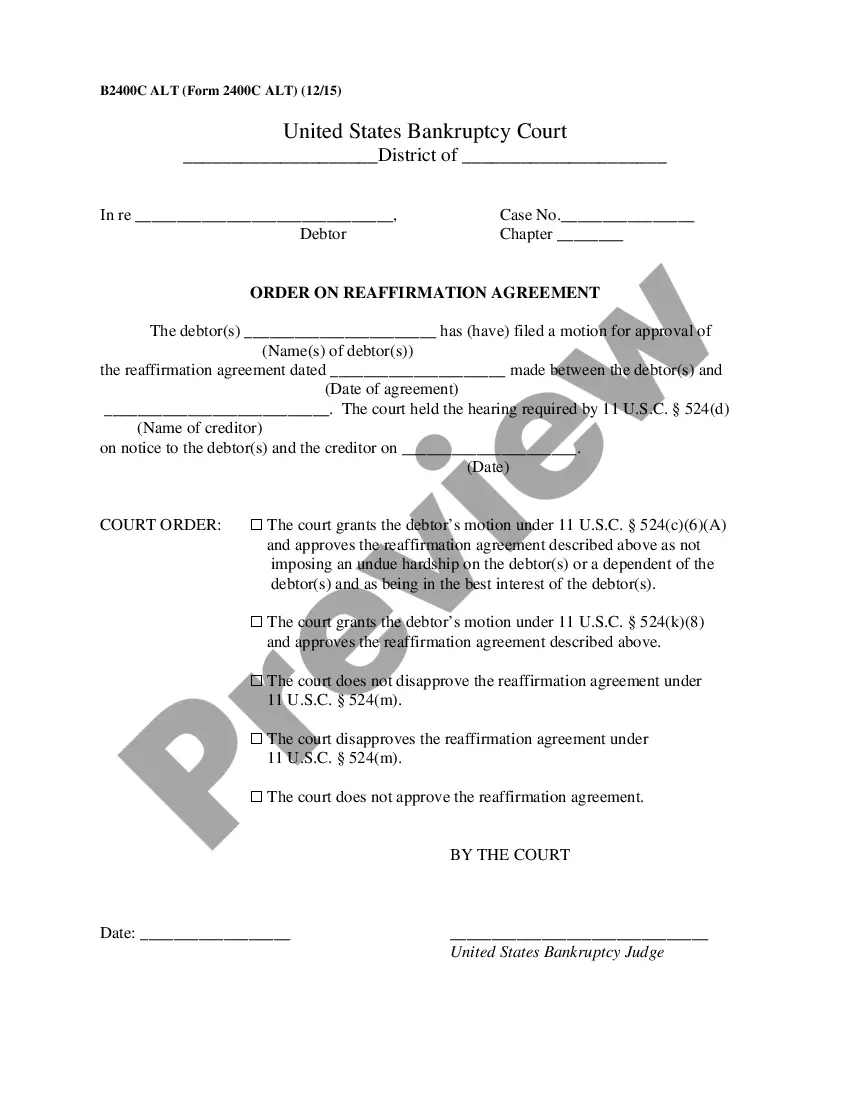

Atlanta Georgia Order on Reaffirmation Agreement

Category:

State:

Multi-State

City:

Atlanta

Control #:

US-B-2400C

Format:

PDF

Instant download

This website is not affiliated with any governmental entity

Public form

Description

Order on Reaffirmation Agreement