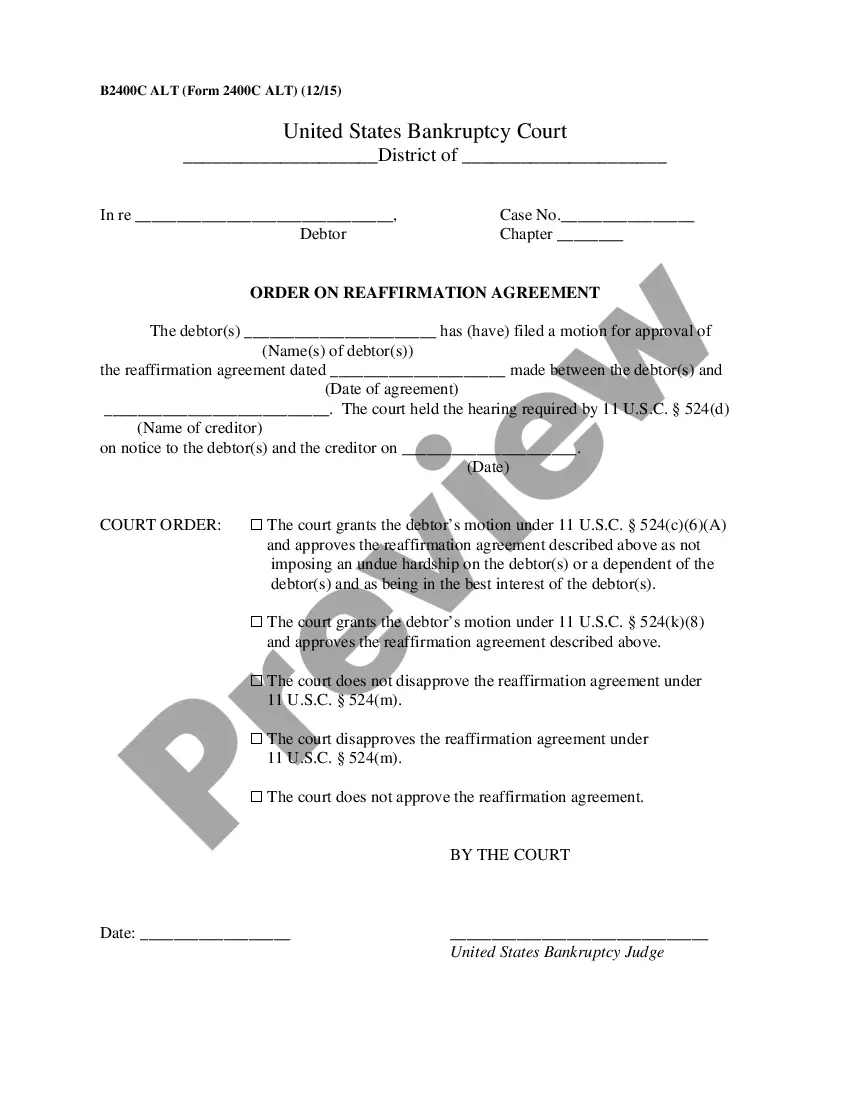

Bronx New York Reaffirmation Agreement, Motion and Order

Description

How to fill out Reaffirmation Agreement, Motion And Order?

Are you seeking to swiftly compose a legally-enforceable Bronx Reaffirmation Agreement, Motion and Order, or perhaps any other document to manage your personal or business matters? You have two choices: consult a legal expert to draft a legitimate document for you or create it entirely on your own. Fortunately, there’s an alternative option - US Legal Forms. It will assist you in obtaining professionally crafted legal documents without incurring exorbitant fees for legal services.

US Legal Forms provides a vast collection of over 85,000 state-specific document templates, comprising Bronx Reaffirmation Agreement, Motion and Order, and form packages. We offer templates for a wide range of life situations: from divorce documentation to real estate document templates. We have been in operation for over 25 years and have established an impeccable reputation with our clients. Here’s how you can join them and obtain the necessary document without any hassle.

If you have previously created an account, you can easily Log In to it, locate the Bronx Reaffirmation Agreement, Motion and Order template, and download it. To re-download the form, simply navigate to the My documents tab.

It’s simple to locate and download legal forms when you utilize our services. Moreover, the templates we offer are examined by legal professionals, which provides you with increased assurance when managing legal matters. Experience US Legal Forms today and see for yourself!

- Initially, thoroughly confirm if the Bronx Reaffirmation Agreement, Motion and Order aligns with your state’s or county’s regulations.

- If the form includes a description, ensure to check its intended use.

- Restart your search if the document does not meet your expectations by utilizing the search bar in the header.

- Choose the subscription that best suits your requirements and proceed to payment.

- Select the format in which you would like to receive your form and download it.

- Print it, fill it out, and sign where indicated.

Form popularity

FAQ

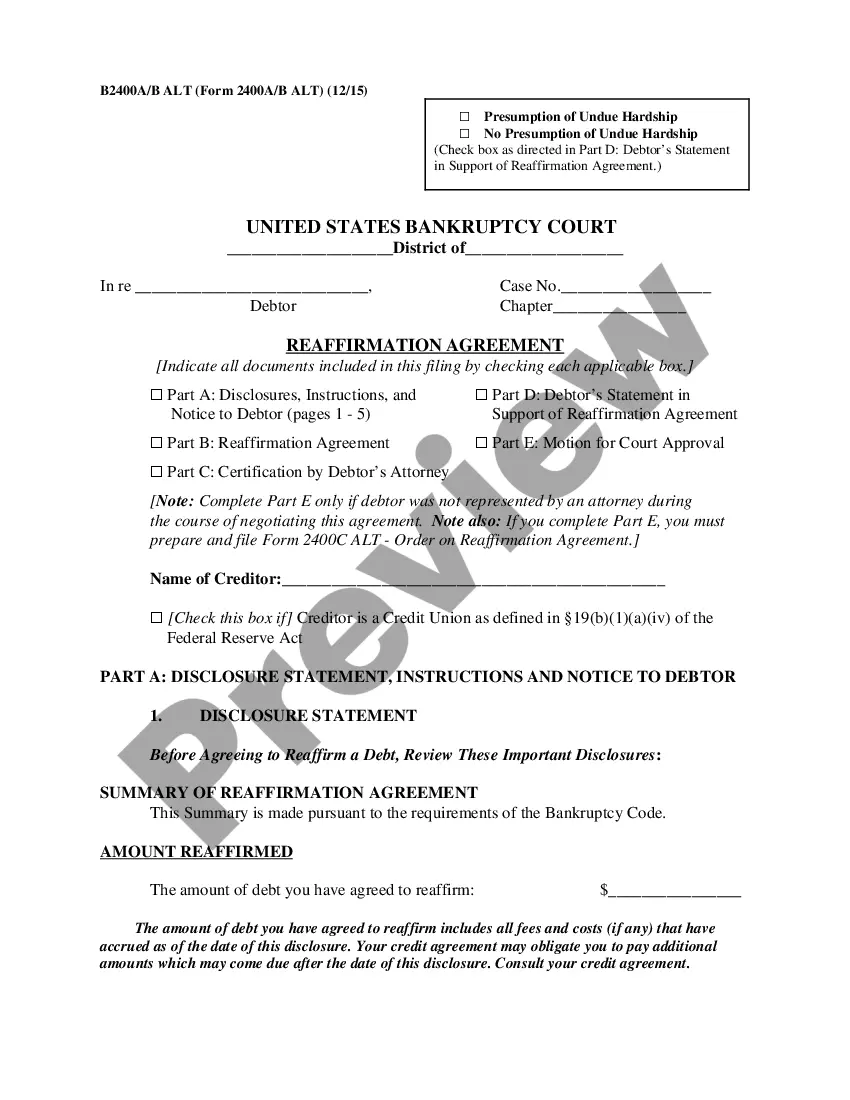

An executed reaffirmation agree- ment may be filed by any party, including the debtor or a creditor. It must be filed within 60 days after the first date set for the first meeting of creditors in the bankruptcy case unless the deadline is extended by the bankruptcy court.

If the debt you have is secured, meaning it uses your home or vehicle as collateral, and you want to maintain possession of that collateral, a reaffirmation agreement stops you from losing it through repossession or foreclosure. It can also help reduce the damage bankruptcy will have to your credit score.

Can you file a reaffirmation agreement after discharge? Once a discharge order has been entered in your bankruptcy case, you can no longer reaffirm any of the debts that were included in the discharge agreement. The same goes for if your case has been closed by the court.

If you don't sign a reaffirmation agreement, the lender can repossess your car after your case closes and the automatic stay lifts. Some car lenders are known to repossess the car immediately, even if you are current on payments.

A lender may offer you a chance to reaffirm the loan because it would prefer you to continue paying back the loan. A reaffirmation agreement can be advantageous to you because: You will keep the vehicle; You may be able to negotiate more favorable terms for the loan; and.

The truth is that you do NOT have to reaffirm your loan to refinance. There is no law that says anything like that. The hurdle is not a law, it is just the bank's policy. They may have chosen not to offer to refinance to people who chose not to reaffirm.

If you don't sign a reaffirmation agreement, the lender can repossess your car after your case closes and the automatic stay lifts. Some car lenders are known to repossess the car immediately, even if you are current on payments.

Reaffirming the debt gives it new life -- you're once again legally obligated to pay it. If you don't make the mortgage payments, the lender can foreclose and your bankruptcy won't stop this from happening.

To reaffirm a car loan, you must be able to show the court that the vehicle is necessary and that the payment is reasonable. You must also be able to show that the car payment isn't an undue hardship on your household (you'll still be able to afford the necessities of life). Effect of a reaffirmation agreement.

Reaffirmation agreements, although required by the bankruptcy laws for every secured debt that the debtor will continue to pay, are often not necessary in practice. This is because the only penalty for failure to sign the reaffirmation is that the creditor might repossess the collateral securing the loan.