Oakland Michigan Certificate of Trust for Testamentary Trust

Description

How to fill out Certificate Of Trust For Testamentary Trust?

Organizing documents for the enterprise or individual requirements is consistently a significant obligation.

When forming an agreement, a public service application, or a power of attorney, it's vital to consider all federal and state statutes and regulations of the specific jurisdiction.

Nevertheless, minor counties and even municipalities also possess legislative protocols that you must take into account.

Utilize the search tab in the page header to find the one that meets your requirements. Ensure the template adheres to legal standards and click Buy Now. Select the subscription plan, then Log In or register for an account with US Legal Forms. Use your credit card or PayPal account to pay for your subscription. Download the chosen file in your preferred format, print it, or complete it electronically. The remarkable aspect of the US Legal Forms library is that all documentation you have ever acquired remains accessible—you can retrieve it in your profile within the My documents tab at any time. Join the platform and effortlessly obtain verified legal forms for any situation with just a few clicks!

- All these factors make it challenging and time-consuming to produce an Oakland Certificate of Trust for Testamentary Trust without expert assistance.

- It's simple to evade expending funds on lawyers drafting your paperwork and create a legally acceptable Oakland Certificate of Trust for Testamentary Trust on your own, utilizing the US Legal Forms online repository.

- It is the most comprehensive online compilation of state-specific legal documents that are professionally validated, so you can be assured of their legitimacy when selecting a template for your county.

- Previously subscribed users only need to Log In to their accounts to retain the necessary document.

- If you still lack a subscription, follow the step-by-step guide below to obtain the Oakland Certificate of Trust for Testamentary Trust.

- Browse the page you’ve opened and verify if it contains the template you need.

- To achieve this, use the form description and preview if these options are available.

Form popularity

FAQ

Another example of a testamentary trust becoming active is by way of a beneficiary completing a set deed that would entitle him to the trust. These deeds could include educational goals or even the act of getting married.

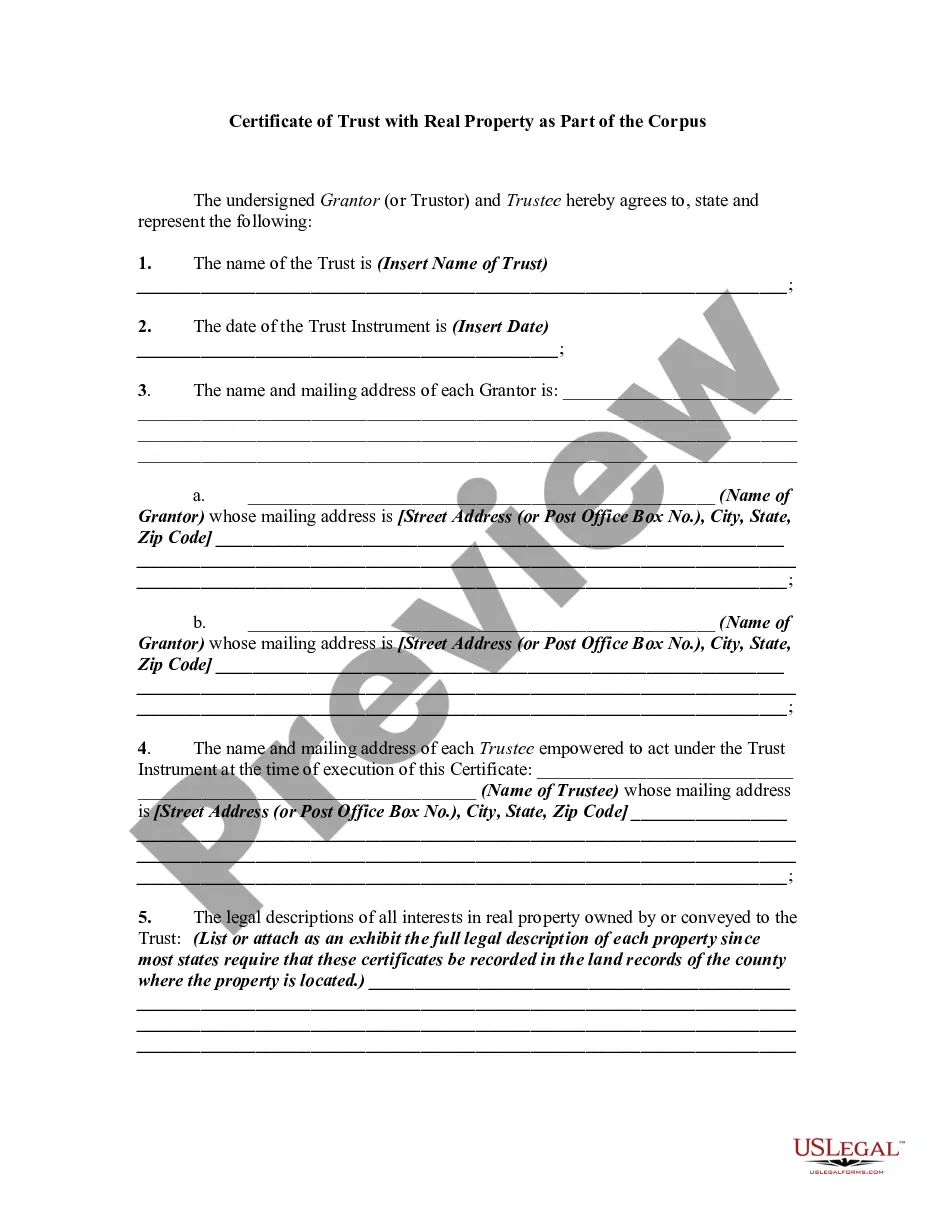

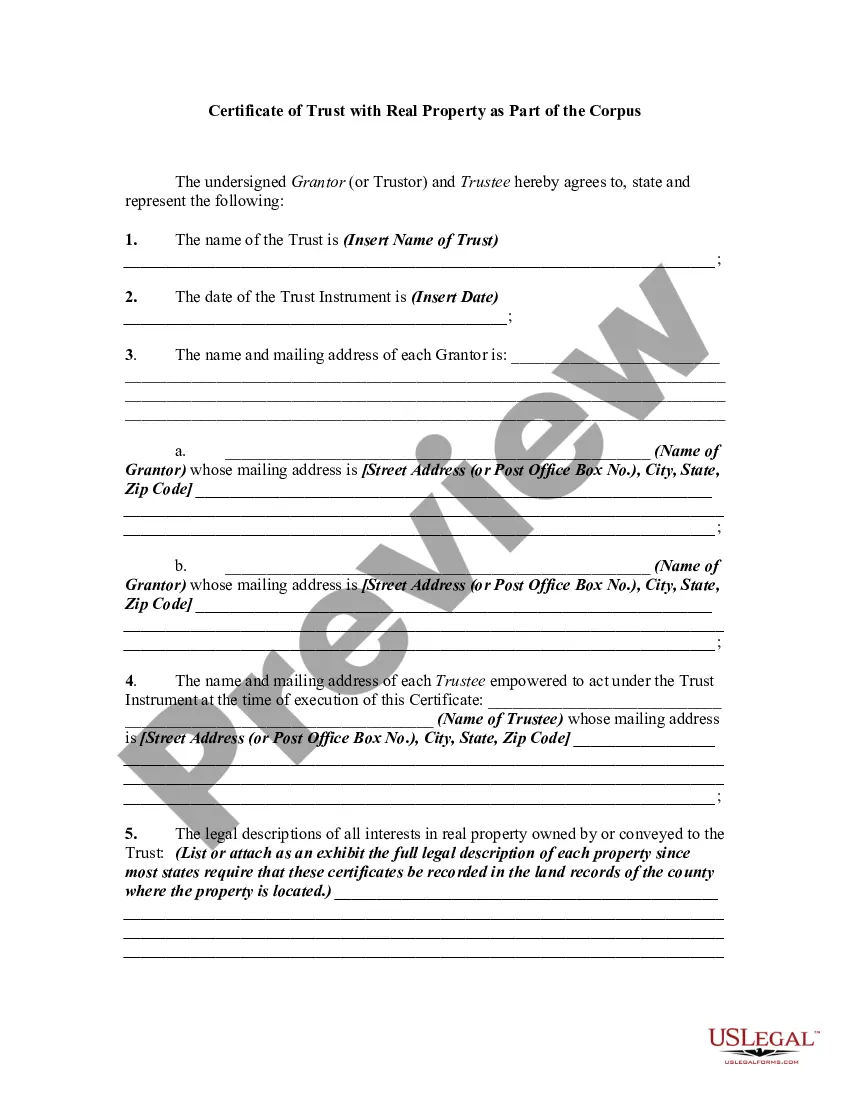

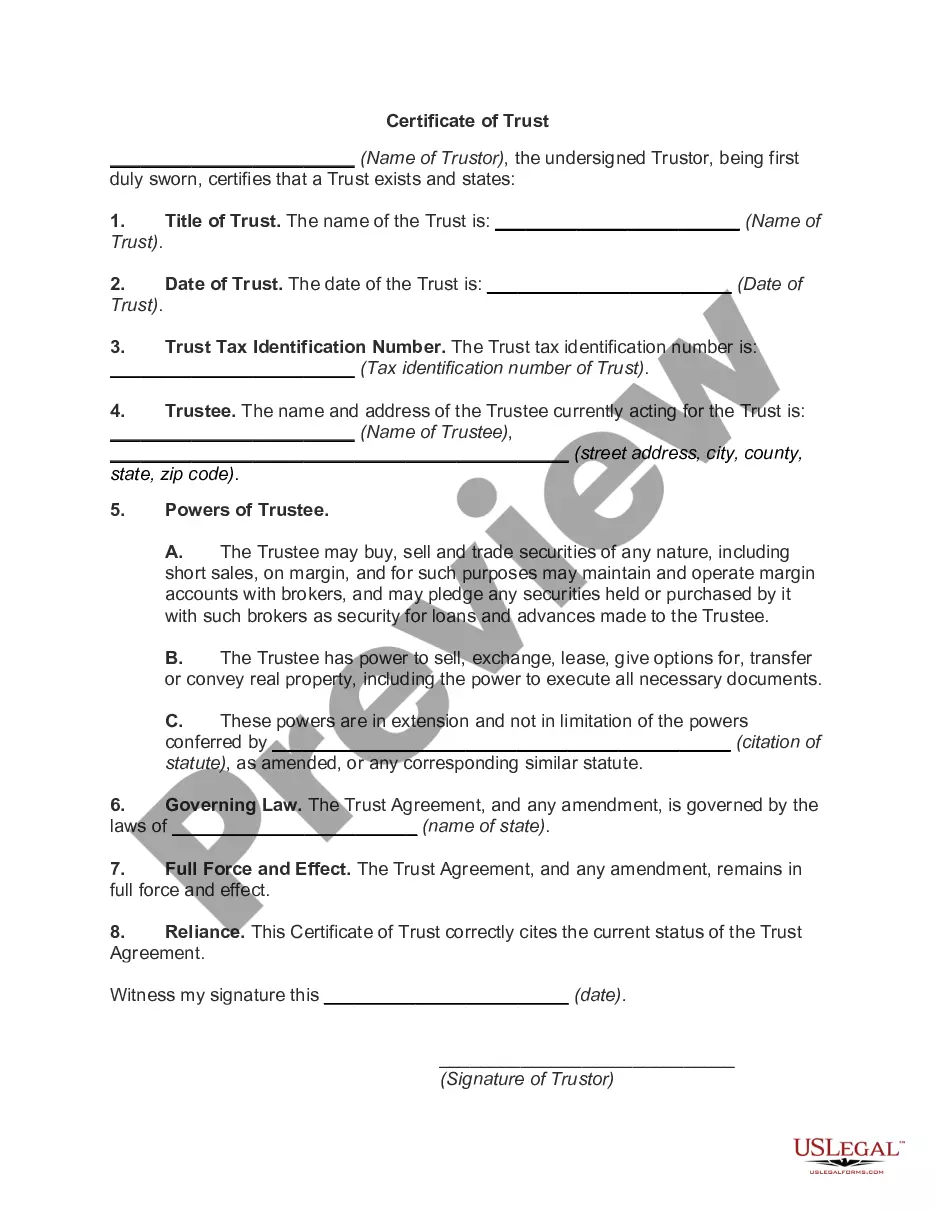

To create a testamentary trust, the settlor must designate a trustee (and possibly successor trustees) as well as beneficiaries of the trust. The document that creates the trust should also state which assets will enter the trust real estate, life insurance proceeds, bank accounts, all assets of the estate, etc.

A testamentary trust guarantees probate. A revocable living trust gives you, or rather your family, a shot at avoiding probate.

A testamentary trust is a trust that is to contain a portion or all of a decedent's assets outlined within a person's last will and testament. A testamentary trust is not established until after the person passes away in which the executor or executrix settles the estate as outlined in the will.

Living trusts and testamentary trusts A living trust (sometimes called an inter vivos trust) is one created by the grantor during his or her lifetime, while a testamentary trust is a trust created by the grantor's will. Only a funded living trust avoids probate court.

Some possible disadvantages are: There is no actual benefit for you, the will maker, although there may be benefits for your beneficiaries. Cost testamentary trusts are often more complex, they generally cost more to produce and they generally involve ongoing accountancy and other fees during their operation.

Taxation of Testamentary Trusts Once a testamentary trust has been created, it becomes a taxable entity in its own right and is thus subject to income taxes. If it has $600 or more in annual income, it must file a U.S. Income Tax Return for Estates and Trusts (Form 1041) for that year.

The testamentary trust is a provision within the will that outlines the estate's executor and instructs that person to create the trust. However, the trust is not immediately established after the person's death since the will must go through the probate process.

To help you get started on understanding the options available, here's an overview the three primary classes of trusts. Revocable Trusts. Irrevocable Trusts. Testamentary Trusts.

To create a testamentary trust, the settlor must designate a trustee (and possibly successor trustees) as well as beneficiaries of the trust. The document that creates the trust should also state which assets will enter the trust real estate, life insurance proceeds, bank accounts, all assets of the estate, etc.