Charlotte North Carolina Installments Fixed Rate Promissory Note Secured by Residential Real Estate

Description

How to fill out North Carolina Installments Fixed Rate Promissory Note Secured By Residential Real Estate?

Locating authenticated templates tailored to your regional regulations can be difficult unless you utilize the US Legal Forms library.

It is an online compilation of over 85,000 legal documents for both personal and business purposes, catering to various real-world scenarios.

All the files are correctly categorized by usage area and jurisdiction, making the search for the Charlotte North Carolina Installments Fixed Rate Promissory Note Secured by Residential Real Estate as swift and simple as ABC.

The procedure will just take a few more steps for new users. Use the US Legal Forms library to maintain organized and legally compliant paperwork, ensuring you have critical document templates readily available for any requirements!

- Ensure you check the Preview mode and document description.

- Confirm that you've selected the correct one that fulfills your requirements and aligns with your local jurisdiction criteria.

- Look for another template if necessary.

- If you encounter any discrepancies, utilize the Search tab above to find the appropriate one. If it meets your needs, proceed to the next stage.

- Click on the Buy Now button and choose your preferred subscription plan.

Form popularity

FAQ

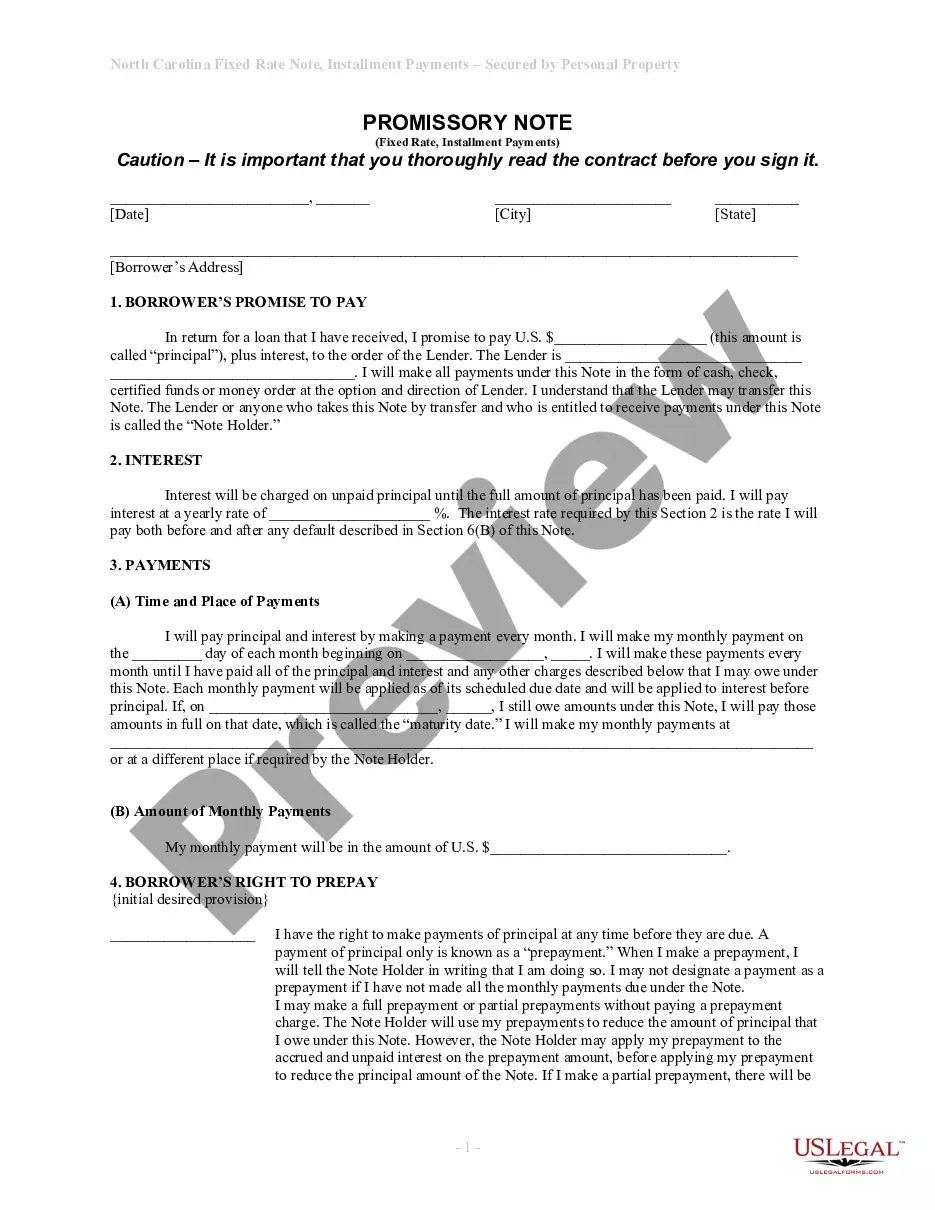

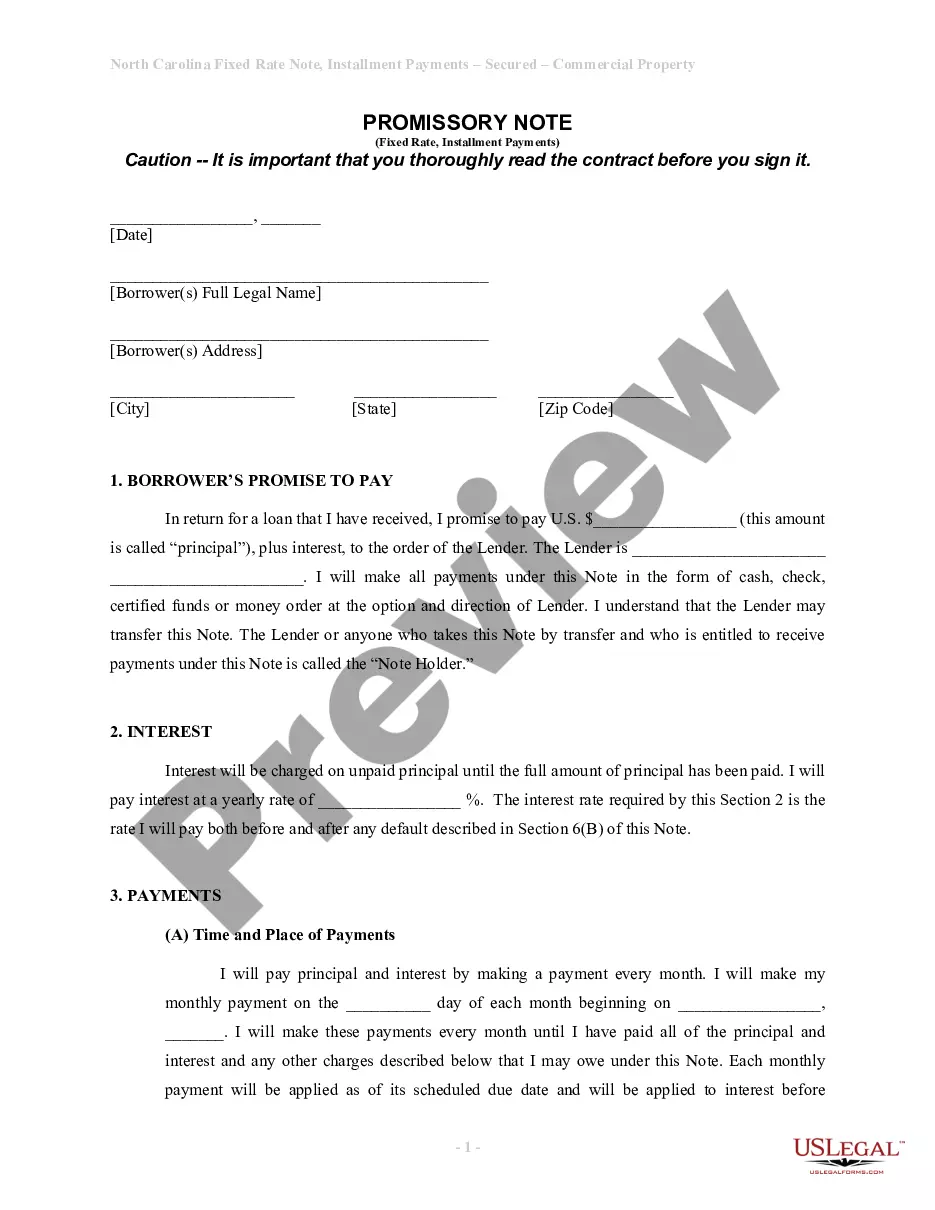

A secured promissory note should carefully outline its repayment, and default terms. For example, it should spell out the steps required for seizing collateral. It should also state if there are any grace periods for late payments, and name who shall pay for costs, and legal fees if there is a default.

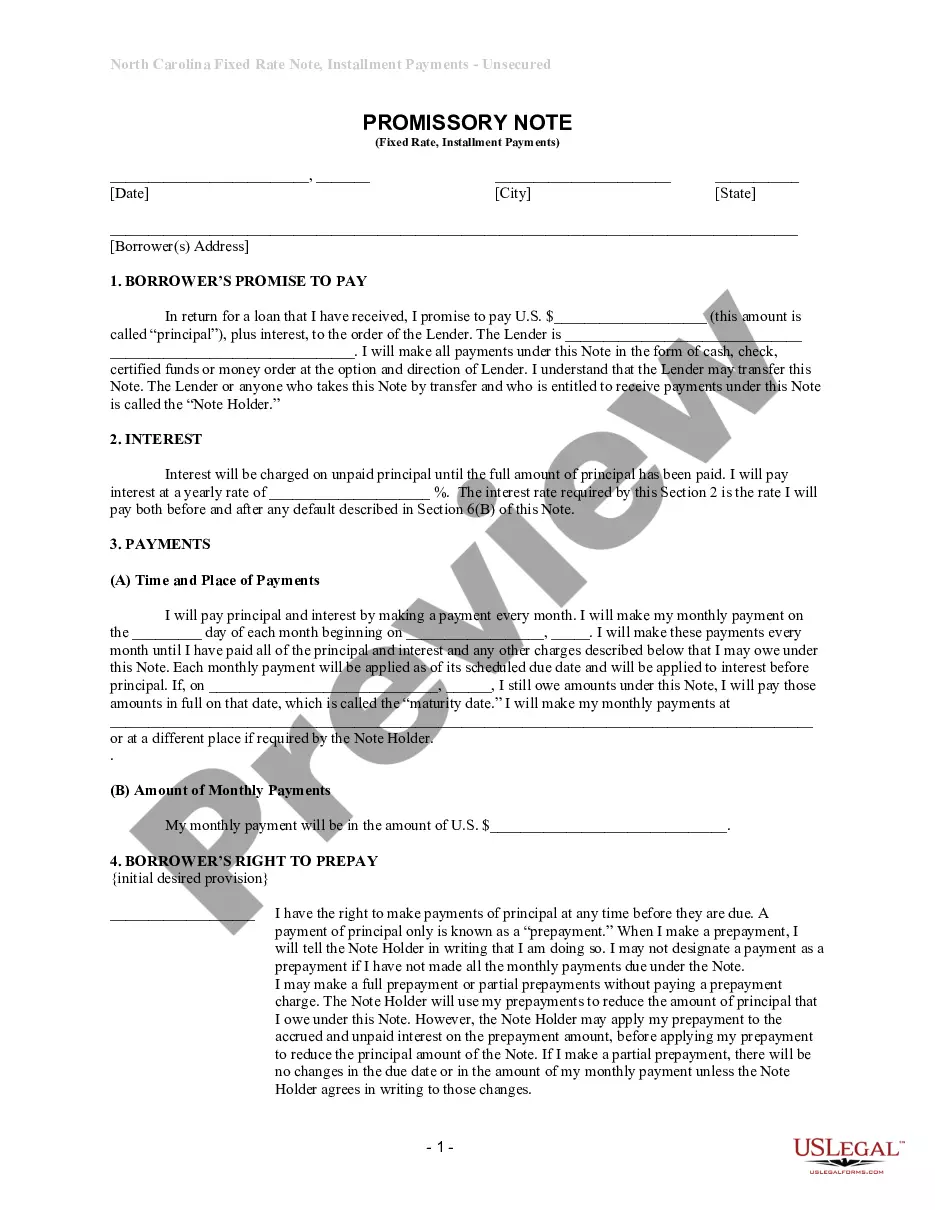

A promissory note refers to a written document stating that a certain amount of money will be paid to someone by a specified date. Generally, it is not necessary for the note to be recorded officially. The borrower is required to sign the note, but the lender may choose not to sign it.

The promissory note, a contract separate from the mortgage, is the document that creates the loan obligation. This document contains the borrower's promise to repay the amount borrowed. If you sign a promissory note, you're personally liable for repaying the loan.

Secured Promissory Notes The property that secures a note is called collateral, which can be either real estate or personal property. A promissory note secured by collateral will need a second document. If the collateral is real property, there will be either a mortgage or a deed of trust.

As part of the home loan mortgage process, you can expect to execute both a legally binding mortgage and mortgage promissory note, which work toward complementary purposes.

A promissory note and deed of trust have one simple function to secure the repayment of a loan by placing a lien on the property as collateral. If the loan is not paid, then the lender has the right to sell the property. Both documents are used to make sure the seller secures the repayment of the loan.

A promissory note can become invalid if it excludes A) the total sum of money the borrower owes the lender (aka the amount of the note) or B) the number of payments due and the date each increment is due.

A promissory note must include the date of the loan, the dollar amount, the names of both parties, the rate of interest, any collateral involved, and the timeline for repayment. When this document is signed by the borrower, it becomes a legally binding contract.

Promissory notes, also known as mortgage notes, are written agreements in which one party promises to pay another party a certain amount of money at a later date in time. Banks and borrowers typically agree to these notes during the mortgage process.

In California, loans can be secured by real property through a deed of trust. Accordingly, a deed of trust is a security instrument that functions like a mortgage.