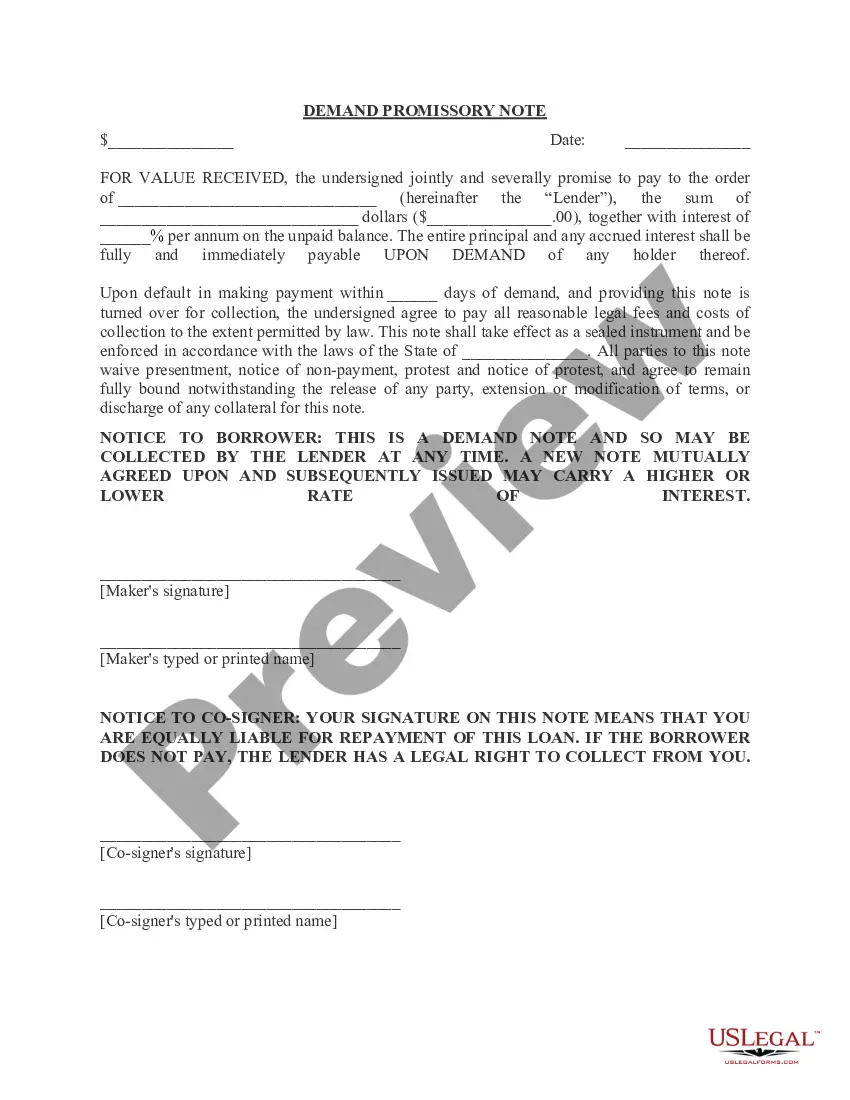

How to Fill Out a Promissory Note: Step-by-Step Guide

A promissory note is a legal document that serves as a written promise from one party (the Borrower) to another party (the Lender) to repay a specified amount of money within a defined timeline. This document outlines the terms of the loan, such as the principal amount, interest rate, repayment schedule, and any penalties for late payments. It is essential for establishing the obligations of both parties and serves as a crucial instrument in personal and commercial finance.

How to complete a form

Filling out a promissory note involves several steps to ensure accuracy and legal validity:

- Date: Add the date when the note is being executed.

- Loan Amount: Clearly state the principal amount being borrowed.

- Borrower Details: Enter the name of the Borrower and their address.

- Lender Details: Fill in the name and address of the Lender.

- Interest Rate: Specify the annual interest rate applicable to the loan.

- Payments: Describe the payment schedule, including due dates and amounts.

Make sure to review the completed form for accuracy before signing.

Key components of the form

A promissory note generally includes the following key components:

- Borrower's Promise: A declaration by the Borrower to repay the specified amount.

- Payment Terms: Details about how and when payments should be made.

- Interest Rate: The rate at which interest will accrue on the principal amount.

- Default Terms: Conditions outlining what happens if the Borrower fails to make payments.

- Governing Law: The legal jurisdiction that governs the terms of the note.

Understanding these components is crucial for both Borrowers and Lenders to ensure clarity and compliance.

Common mistakes to avoid when using this form

When filling out a promissory note, be mindful of these common mistakes:

- Leaving blank spaces: Ensure all fields are completed.

- Incorrect dates: Always double-check the dates to avoid confusion about timelines.

- Ambiguous terms: Use clear and concise language to define payment terms and conditions.

- Not discussing terms: Ensure both parties have a mutual understanding of all terms before signing.

- Failing to keep copies: Retain copies of the signed document for your records.

By being aware of these pitfalls, users can enhance the effectiveness of their promissory notes and avoid potential disputes.

What documents you may need alongside this one

When creating a promissory note, consider preparing additional documents such as:

- Mortgage Agreement: If the note is tied to real estate, include the mortgage details.

- Identification: Provide ID proof for both Borrower and Lender.

- Financial Statements: Statements reflecting the Borrower's financial capability to repay the loan.

- Witness Affidavit: A document confirming the signing of the note in front of a witness, if required.

These documents can help clarify the relationship between parties and provide legal backing for the agreement.

Key takeaways

In summary, completing a promissory note correctly is vital to protecting both the Borrower and the Lender's interests. Remember these essential points:

- Clear definitions of terms establish mutual understanding.

- Accurate and complete information prevents future disputes.

- Consulting with a legal professional can provide additional assurance.

Properly filling out and managing a promissory note can help ensure smooth financial transactions.