"Under SEC law, a company that offers its own securities must register these investments with the SEC before it can sell them unless it meets an exception. One of those exceptions is selling unregistered investments to accredited investors.

To become an accredited investor the (SEC) requires certain wealth, income or knowledge requirements. The investor must fall into one of three categories. Firms selling unregistered securities must put investors through their own screening process to determine if investors can be considered an accredited investor.

The Verifying Individual or Entity should take reasonable steps to verify and determined that an Investor is an "accredited investor" as such term is defined in Rule 501 of the Securities Act, and hereby provides written confirmation. This letter serves to help the Entity determine status."

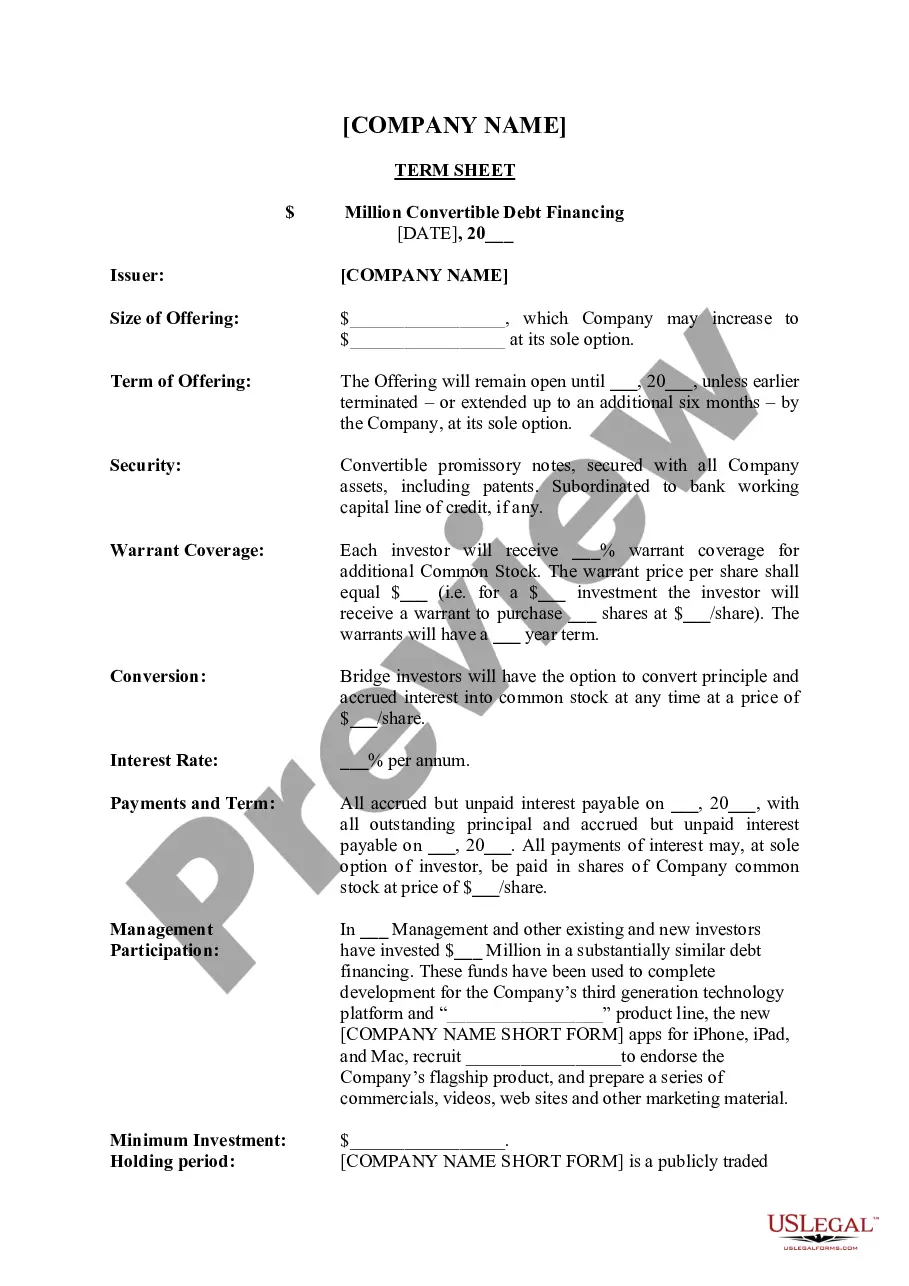

Wyoming Term Sheet - Convertible Debt Financing

State:

Multi-State

Control #:

US-ENTREP-0020-3

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Term Sheet - Convertible Debt Financing?

You are able to invest hrs online attempting to find the lawful record web template that suits the state and federal requirements you want. US Legal Forms provides 1000s of lawful kinds that are reviewed by professionals. You can easily obtain or printing the Wyoming Term Sheet - Convertible Debt Financing from our assistance.

If you already possess a US Legal Forms profile, you are able to log in and click on the Down load button. After that, you are able to total, revise, printing, or signal the Wyoming Term Sheet - Convertible Debt Financing. Each lawful record web template you buy is your own property forever. To acquire another backup of the bought form, proceed to the My Forms tab and click on the related button.

Should you use the US Legal Forms internet site the first time, adhere to the basic recommendations beneath:

- Very first, ensure that you have selected the right record web template for your county/metropolis of your choice. Look at the form explanation to make sure you have picked out the appropriate form. If accessible, take advantage of the Review button to look from the record web template as well.

- If you want to discover another edition of the form, take advantage of the Research field to find the web template that meets your needs and requirements.

- Upon having discovered the web template you need, just click Buy now to continue.

- Select the prices plan you need, enter your references, and register for your account on US Legal Forms.

- Comprehensive the deal. You can utilize your Visa or Mastercard or PayPal profile to cover the lawful form.

- Select the structure of the record and obtain it for your product.

- Make modifications for your record if required. You are able to total, revise and signal and printing Wyoming Term Sheet - Convertible Debt Financing.

Down load and printing 1000s of record web templates while using US Legal Forms web site, that offers the greatest collection of lawful kinds. Use expert and status-specific web templates to deal with your company or specific needs.

Form popularity

FAQ

Convertible debt issued at a substantial premium could result in the instrument being treated entirely as an equity instrument for tax purposes, with no tax consequences during its term or upon redemption.

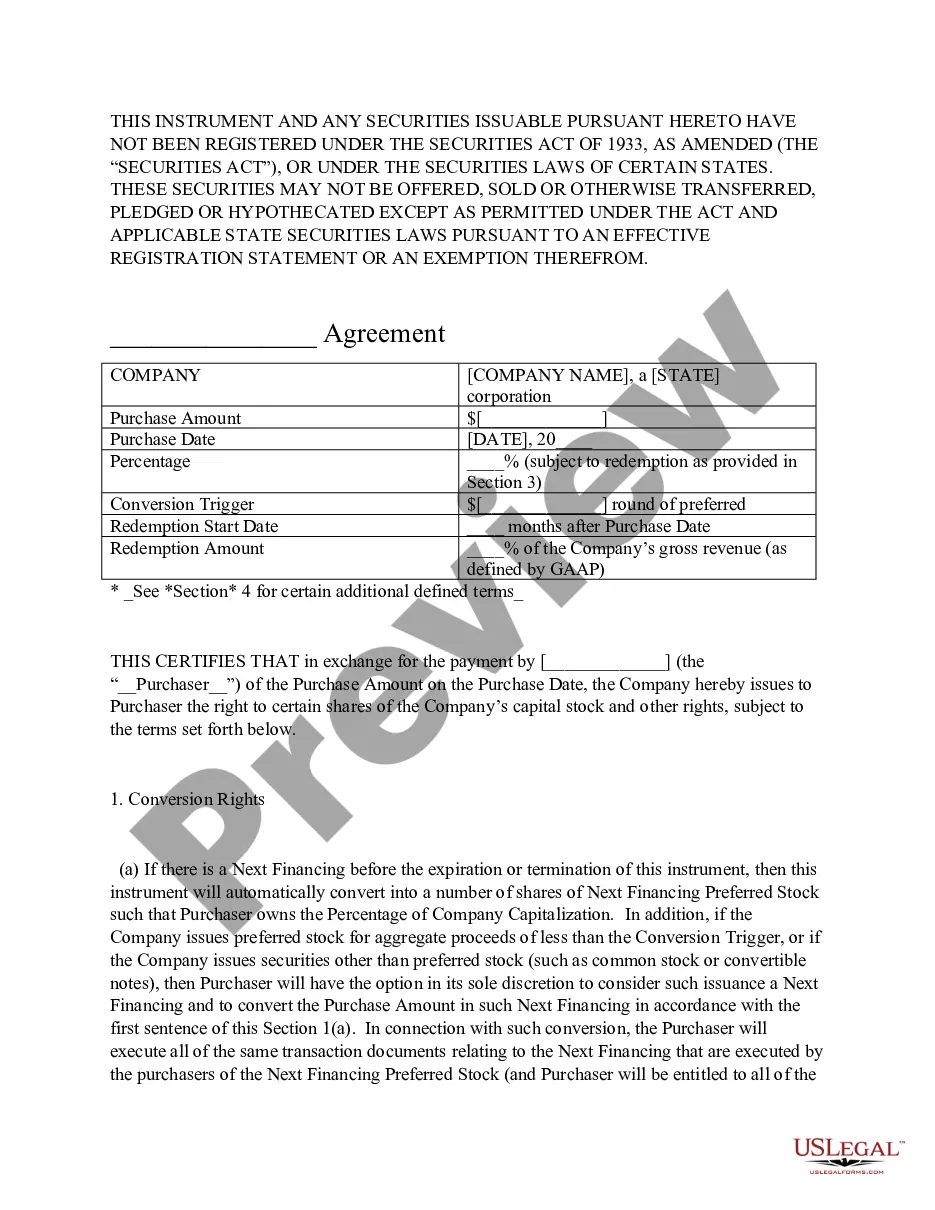

Convertible debt is a debt hybrid product with an embedded option that allows the holder to convert the debt into equity in the future. The ratio is calculated by dividing the convertible security's par value by the conversion price of equity.

The convertible debt that was listed as a non-current liability before the conversion now gets get treated as shareholder's equity.

Convertible Notes are loans ? so they are recorded on the Balance Sheet of a company as a liability when they are made. Depending on the debt's maturity date, they can either be shown as a current liability (loans maturing within 12 months) or as a Long-term liability (loans maturing over 12 months).

Conversion to Equity - Accounting for Convertible Debt When the note converts, usually during a new funding round, the liability moves to the equity section of the balance sheet. At this stage, the convertible note is settled, and new equity instruments, typically preferred shares, are issued to the investor.

Typically, the result is that the amount will convert to shares. If the convertible notes convert into shares, the company will need to determine how many shares to issue to the noteholder. To do so, the company will usually divide the loan amount, plus any accrued interest, by a certain share price.

For tax purposes, the tax basis of the convertible debt is the entire proceeds received at issuance of the debt. Thus, the book and tax bases of the convertible debt are different. ASC 740-10-55-51 addresses whether a deferred tax liability should be recognized for that basis difference.

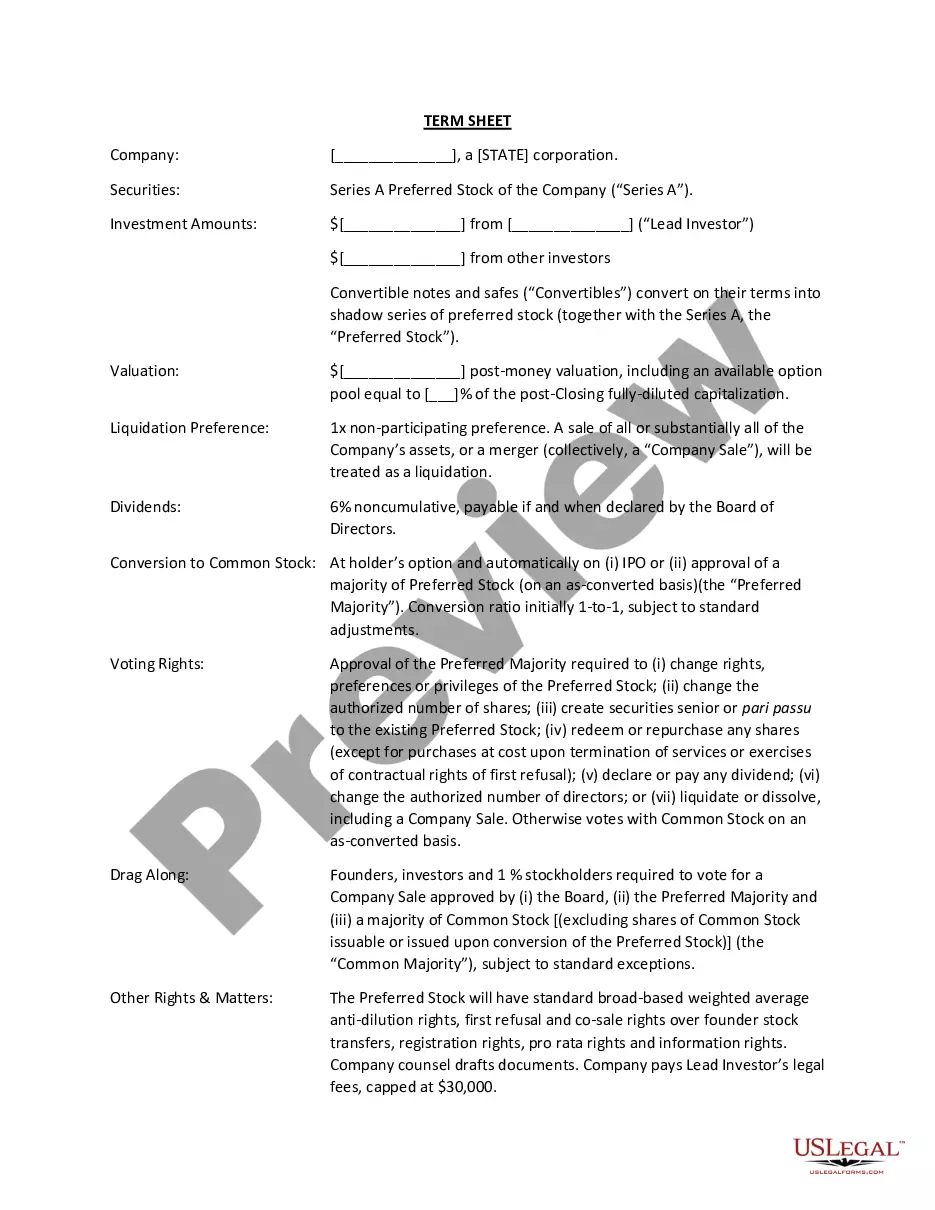

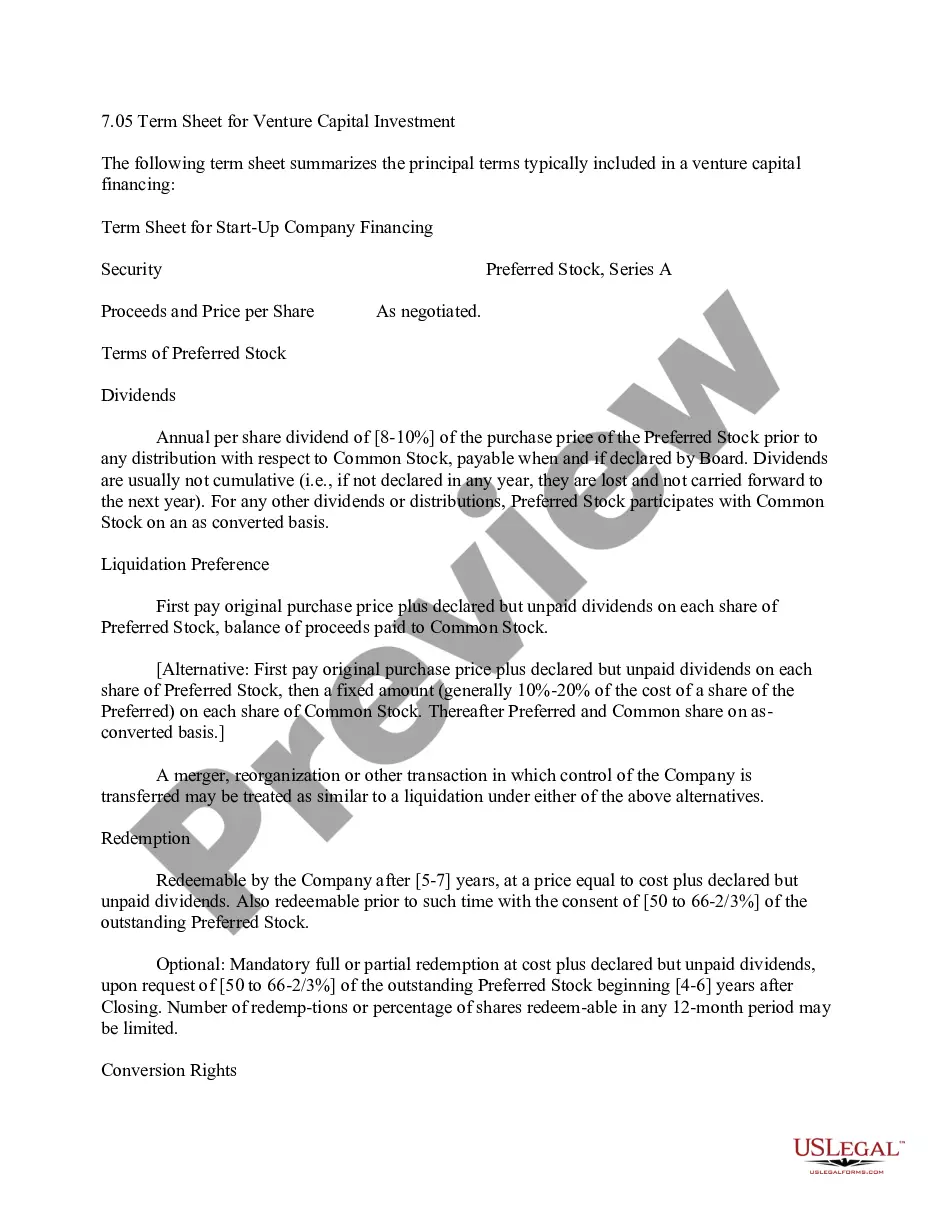

Although it is customary to forego a term sheet, in some cases it may be required if the parties need to negotiate certain terms. It can be advantageous to use a term sheet for the company to easily summarize the terms of the notes for potential other investors purchasing a convertible note.