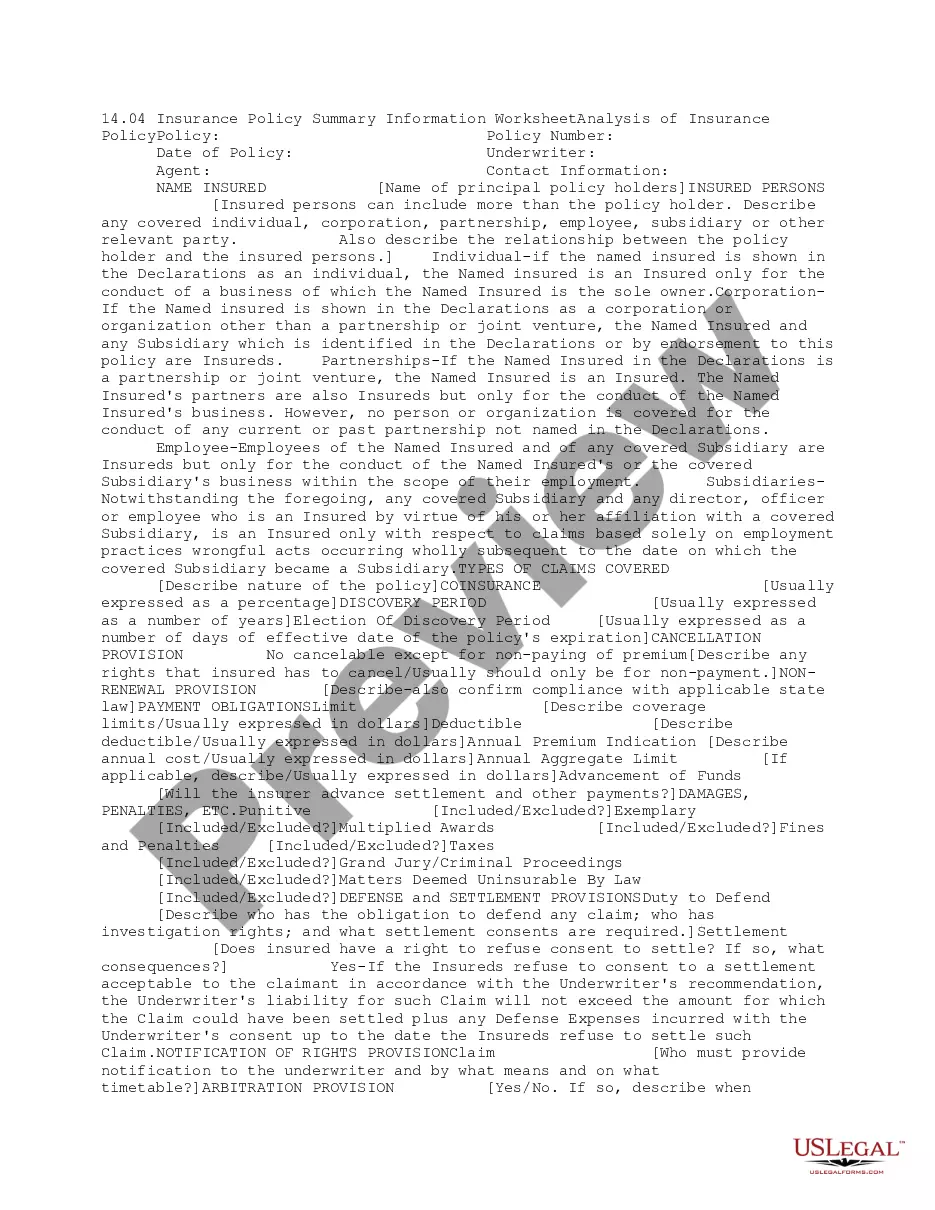

This due diligence form is a summary of insurance coverage analysis for directors and officers in a company.

Wyoming Executive Summary Director and Officer Insurance Coverage Analysis

Category:

State:

Multi-State

Control #:

US-DD01409

Format:

Word;

PDF;

Rich Text

Instant download

Description

How to fill out Executive Summary Director And Officer Insurance Coverage Analysis?

US Legal Forms - one of the most extensive collections of legal templates in the United States - offers a wide range of legal document samples that you can download or print.

While navigating the website, you can discover numerous templates for both business and personal purposes, organized by categories, states, or keywords. You can access the most current versions of forms such as the Wyoming Executive Summary Director and Officer Insurance Coverage Analysis within moments.

If you already possess a monthly subscription, Log In and download the Wyoming Executive Summary Director and Officer Insurance Coverage Analysis from the US Legal Forms library. The Acquire button will appear on every form you view. You can access all previously obtained forms from the My documents section of your account.

Afterwards, process the purchase. Use your credit card or PayPal account to complete the transaction.

Select the format and download the form to your device.

- If you are using US Legal Forms for the first time, here are simple steps to help you get started.

- Ensure you have selected the appropriate form for your city/region.

- Click the Review button to examine the contents of the form.

- Read the form description to confirm you have chosen the correct one.

- If the form does not meet your needs, utilize the Search area at the top of the screen to find one that does.

- If you are satisfied with the form, confirm your choice by clicking the Purchase now button.

- Then, select the pricing plan you would like and provide your details to register for an account.

Form popularity

FAQ

D&O policies also typically do not cover certain specified forms of misconduct, including fraudulent or criminal acts, losses relating to illegally obtained remuneration by Ds&Os, and other actions taken for their personal profit, if the proscribed conduct is established by a final, non-appealable adjudication.

Side C of the D&O policy, also known as entity coverage, ensures there is corporate coverage whenever the corporation is sued along with the Ds and Os.

Side A covers claims against directors and officers not indemnified by the corporation. The liability of D&O are personal liabilities, meaning if someone else won't pay their legal bills, they're personally on the hook. Side B is for the benefit of the corporation.

Side A Difference In Conditions insurance coverage provides excess coverage when the underlying D&O Insurance policy is used up. Side A Difference In Conditions insurance coverage responds when a claims is excluded the underlying policy.

The Directors & Officers Liability Insurance policy insures members of the board of directors, the management and employee performing a supervisory or managerial role in a company against personal liability and defense costs incurred from claims alleging them to have committed a wrongful act in the line of their duties

Side A D&O Provides financial protection when a company cannot or will not indemnify the individual directors and officers, such as per a court order. Since Side A D&O is designed to individually protect a director's assets in the event of a lawsuit, this coverage is particularly critical.

Side B. Side B is the part of the D&O policy that reimburses a company for its indemnification obligation to its directors and officers. This part of the insurance policy is generally subject to a self-insured retention or deductible.

A Side A DIC policy provides excess Side A D&O insurance that picks up coverage once a company's traditional D&O tower is exhausted. A Side A DIC policy drops down to fill in gaps in a company's D&O tower when any underlying insurer fails or refuses to pay, attempts to rescind coverage, or becomes insolvent.

Directors and officers (D&O) liability insurance protects the personal assets of corporate directors and officers, and their spouses, in the event they are personally sued by employees, vendors, competitors, investors, customers, or other parties, for actual or alleged wrongful acts in managing a company.

The D&O policy provides cover for the personal liability of Directors and Officers arising due to wrongful acts in their managerial capacity. Defence costs are also covered and are payable in advance of final judgment.