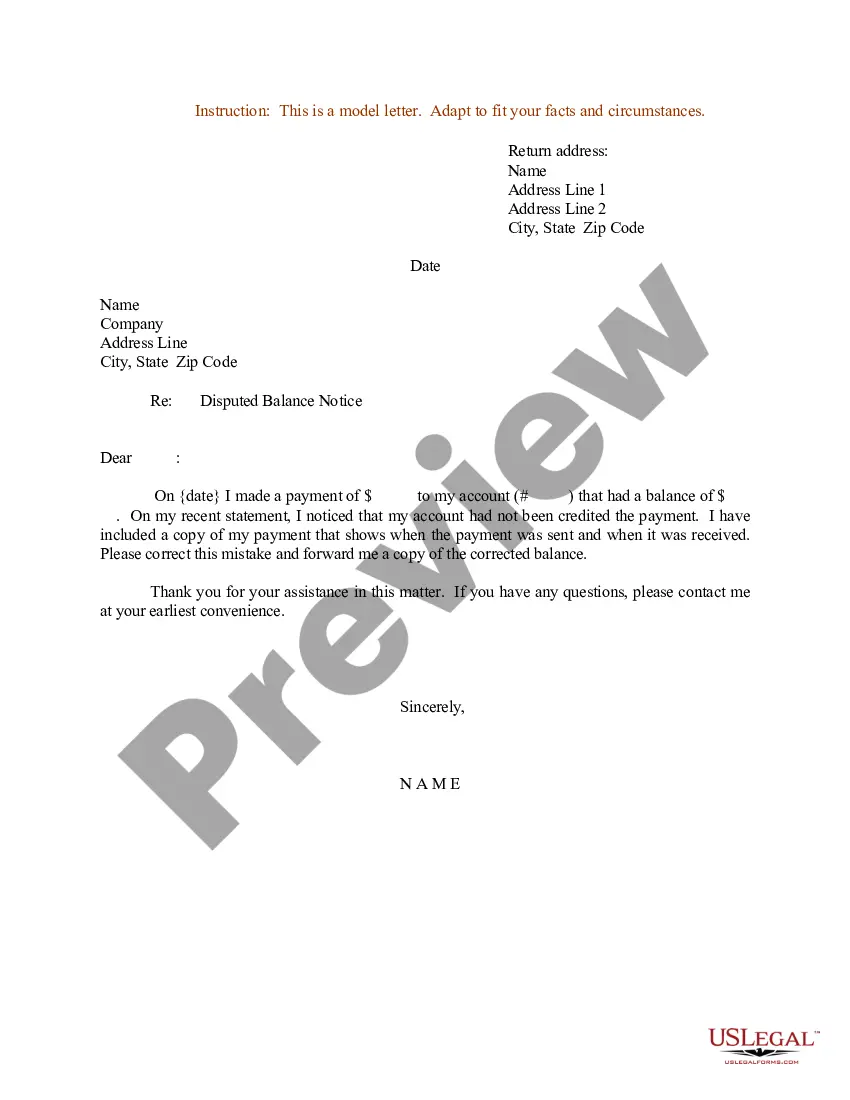

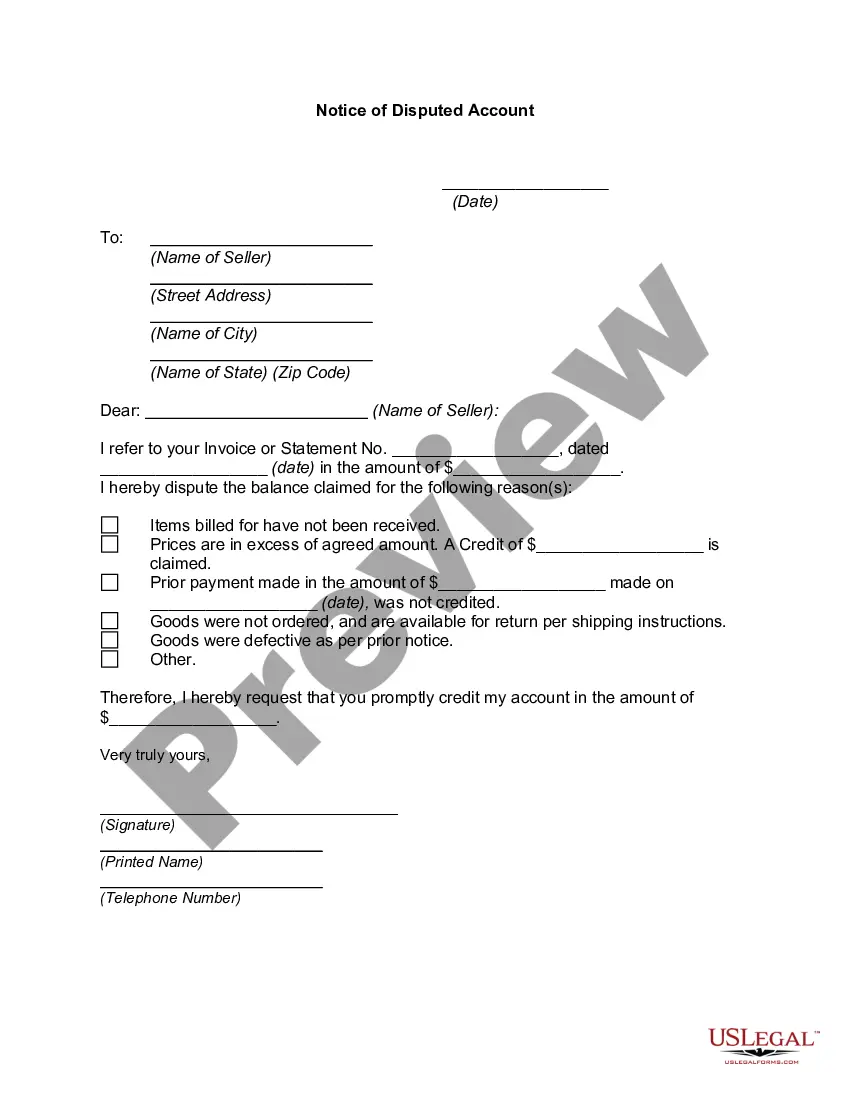

This form is to be used when a collection company is demanding full payment from you and you disagree with the balance. Use this form as your first letter of dispute.

West Virginia Letter of Dispute - Complete Balance

Instant download

Description

Free preview

How to fill out Letter Of Dispute - Complete Balance?

You can dedicate several hours online trying to locate the official document template that fulfills the state and federal requirements you need.

US Legal Forms offers thousands of official forms that have been reviewed by experts.

You can download or print the West Virginia Letter of Dispute - Complete Balance from my service.

If available, use the Review button to browse the document template as well. If you wish to obtain another version of your form, use the Search field to find the template that fits your needs. Once you have found the template you desire, click Get now to proceed. Select the pricing plan you prefer, enter your information, and create your account on US Legal Forms. Complete the payment. You can use your credit card or PayPal account to purchase the official document. Choose the format of your file and download it to your device. Make edits to your document if necessary. You can complete, modify, sign, and print the West Virginia Letter of Dispute - Complete Balance. Download and print thousands of document templates using the US Legal Forms website, which offers the largest collection of official forms. Utilize professional and state-specific templates to address your business or personal needs.

- If you already have a US Legal Forms account, you may Log In and then click the Download button.

- After that, you can complete, modify, print, or sign the West Virginia Letter of Dispute - Complete Balance.

- Each official document template you receive is yours indefinitely.

- To obtain another copy of the purchased form, go to the My documents section and click the relevant button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure you have selected the correct document template for your preferred region/city.

- Review the form description to confirm you have chosen the right document.

Form popularity

FAQ

In West Virginia, the statute of limitations for most debts is generally ten years. This limitation applies to various types of debt, including credit cards and personal loans. Once this period has expired, creditors can no longer sue you for the debt. For your peace of mind, you might want to explore using a West Virginia Letter of Dispute - Complete Balance to clarify your situation with creditors and ensure your credit report reflects accurate information.

A 609 letter is a type of letter you can send to credit bureaus to dispute unauthorized inquiries on your credit report. This letter references Section 609 of the Fair Credit Reporting Act, offering you the right to request proof of any inquiries. If you find inaccuracies, it can help in removing them. To strengthen your case, consider utilizing a West Virginia Letter of Dispute - Complete Balance, which can guide you in formatting your request comprehensively.

To write a letter for removing a collection from your credit report, start by stating your name and contact information clearly. Include details about the collection account, such as the account number and the name of the creditor. Politely request the removal of the collection and provide any supporting documents. Using a West Virginia Letter of Dispute - Complete Balance can simplify this process by offering a structured format that helps you convey your request effectively.

In West Virginia, a debt typically becomes uncollectible after a period of ten years. This time frame is defined by the statute of limitations on most types of debt. After this period, creditors cannot legally pursue collection through the courts. However, you may still want to consider using a West Virginia Letter of Dispute - Complete Balance to formally address any lingering issues related to the debt.

Filing a dispute letter involves sending your letter to the relevant party, typically through certified mail for documentation. Ensure that you keep a copy of your letter for your records. If you are using the West Virginia Letter of Dispute - Complete Balance, follow its guidelines closely to ensure compliance. Additionally, consider using platforms like uslegalforms for streamlined processes and templates that can save you time.

To start a letter of dispute, begin with your contact information and the date at the top. Next, include the recipient’s details and a clear subject line indicating the dispute. Then, introduce the purpose of your letter, making sure to mention the West Virginia Letter of Dispute - Complete Balance. This sets a professional tone and prepares the reader for the details that follow.

Yes, you can write your own dispute letter. It is essential to express your concerns clearly and accurately, guided by the West Virginia Letter of Dispute - Complete Balance. By doing so, you can convey your position effectively without needing legal representation. However, if the situation is complex, consider seeking assistance from professionals like uslegalforms for added support.

A legal dispute letter must be formal and concise. Start with your contact details and the date, followed by the recipient's information. Clearly state the dispute and reference any applicable laws or agreements, emphasizing the West Virginia Letter of Dispute - Complete Balance. Ensure you provide all necessary facts and communicate your desired outcome for clarity.

When writing a dispute letter, you should begin with your name, address, and date at the top. Follow with the recipient's information and a clear subject line indicating the nature of your dispute. In the body, detail the issue, using the West Virginia Letter of Dispute - Complete Balance as a framework. Conclude by stating what resolution you seek and include your contact information for further communication.

To write a payment dispute letter, start by clearly stating your purpose at the top. Include your contact information and any relevant account details. Then, explain the reasons for your dispute regarding the specific charges, referencing the West Virginia Letter of Dispute - Complete Balance. Be sure to keep your tone professional and provide any supporting documentation to strengthen your case.