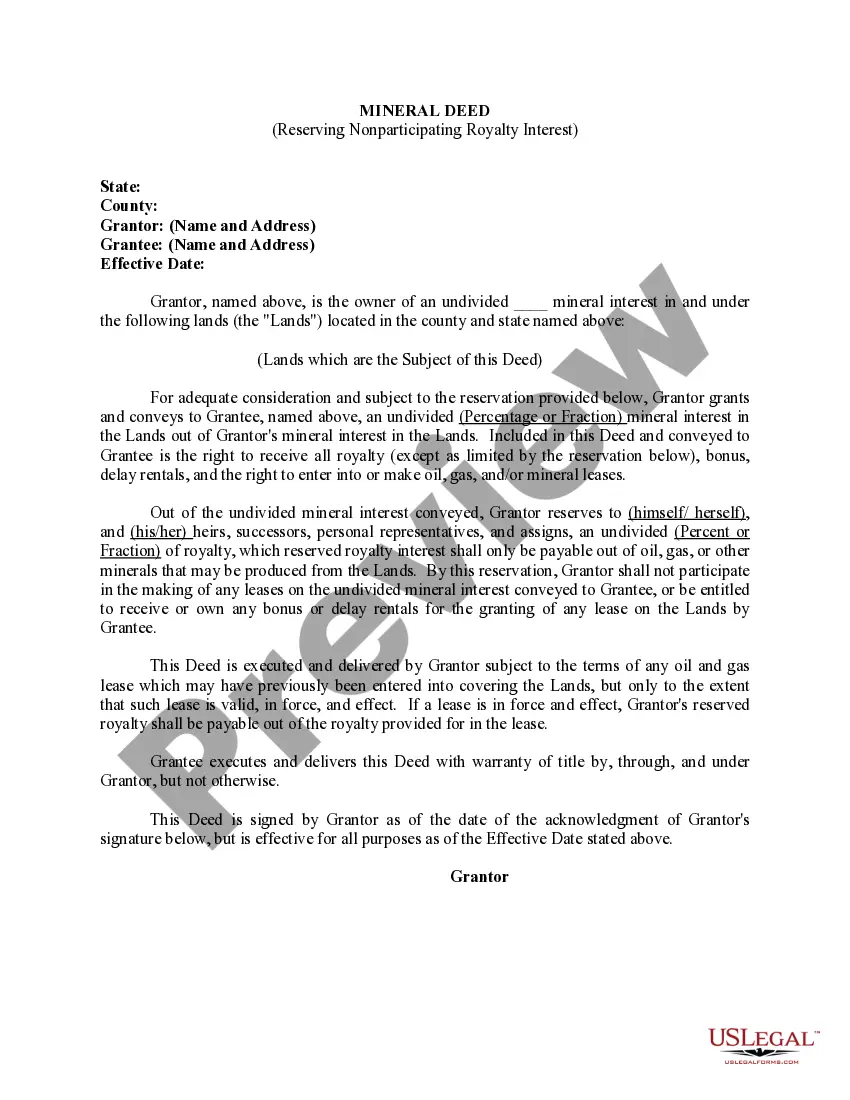

Wisconsin Term Nonparticipating Royalty Deed from Mineral Owner

Description

How to fill out Term Nonparticipating Royalty Deed From Mineral Owner?

You are able to devote hrs on-line trying to find the legal record design that suits the federal and state demands you need. US Legal Forms offers 1000s of legal types which are examined by specialists. You can actually obtain or print the Wisconsin Term Nonparticipating Royalty Deed from Mineral Owner from our support.

If you already possess a US Legal Forms account, you are able to log in and then click the Download key. After that, you are able to full, edit, print, or sign the Wisconsin Term Nonparticipating Royalty Deed from Mineral Owner. Each legal record design you buy is your own eternally. To have an additional duplicate for any acquired develop, check out the My Forms tab and then click the corresponding key.

Should you use the US Legal Forms internet site the first time, adhere to the straightforward directions below:

- First, ensure that you have selected the right record design to the county/metropolis of your choice. Look at the develop outline to ensure you have chosen the right develop. If accessible, take advantage of the Preview key to appear from the record design at the same time.

- If you wish to find an additional model from the develop, take advantage of the Research discipline to discover the design that suits you and demands.

- Upon having discovered the design you need, just click Acquire now to continue.

- Pick the rates program you need, type your qualifications, and sign up for a merchant account on US Legal Forms.

- Full the purchase. You can utilize your credit card or PayPal account to fund the legal develop.

- Pick the file format from the record and obtain it to the device.

- Make adjustments to the record if required. You are able to full, edit and sign and print Wisconsin Term Nonparticipating Royalty Deed from Mineral Owner.

Download and print 1000s of record layouts utilizing the US Legal Forms site, that provides the greatest selection of legal types. Use skilled and condition-certain layouts to tackle your organization or specific requires.

Form popularity

FAQ

The formula to calculate NPRI without proportionate share reduction is LRR ? RI = NPRI. As an example, reducing your revenue interest from 25% LRR results in 1/16 NPRI, leaving 75% NRI for working interest owners.

Mineral rights deeds are not the same as royalty deeds. Royalty deeds do not allow for surface access, or for the initiation of the extraction and sale of minerals. A royalty owner will only benefit economically if the mineral owner decides to produce and sell the minerals.

Royalty income is considered passive income by the Internal Revenue Service. This means it is generally taxed at capital gains rates, which are usually lower than the rates paid by individuals for earned income such as wages and salaries.

Mineral Rights Owner- If you are solely a mineral rights owner, you earn the royalties that come from extracting the minerals from the land in question. You do not have control over what occurs on the surface. As the mineral rights owner, you can sell, mine or produce the gas or oil below the surface.

The IRS views the profits from the sale of mineral rights as a capital gain, not income. To figure out how much you might need to pay as a capital gains tax, you need to figure out your cost basis in the mineral rights. The cost basis is the original price or value of the asset ? in this case, mineral rights.

To recap, mineral royalties held for investment are not likely to qualify for the 20 percent deduction; however, income from a working interest income appears to be eligible.

Mineral rights deeds are not the same as royalty deeds. Royalty deeds do not allow for surface access, or for the initiation of the extraction and sale of minerals. A royalty owner will only benefit economically if the mineral owner decides to produce and sell the minerals.

A quick overview of the differences between mineral rights and royalty interests shows a mineral interest is a real property interest obtained by severing the minerals from the surface and a royalty interest grants an owner a portion of the production revenue generated.