Virgin Islands Hardship Letter to Mortgagor or Lender to Prevent Foreclosure

Description

How to fill out Hardship Letter To Mortgagor Or Lender To Prevent Foreclosure?

If you require to finalize, acquire, or print authentic document templates, utilize US Legal Forms, the largest collection of authentic forms available online.

Employ the site's straightforward and user-friendly search to find the documents you need.

Various templates for business and personal use are categorized by themes and jurisdictions, or by keywords. Utilize US Legal Forms to secure the Virgin Islands Hardship Letter to Mortgagor or Lender to Prevent Foreclosure in just a few clicks.

Each legal document template you acquire is yours permanently. You will have access to every form you downloaded within your account. Select the My documents section and choose a document to print or download again.

Act now and obtain, and print the Virgin Islands Hardship Letter to Mortgagor or Lender to Prevent Foreclosure with US Legal Forms. There are millions of professional and state-specific forms available for your business or personal needs.

- In case you are already a US Legal Forms member, Log In to your account and click the Obtain button to get the Virgin Islands Hardship Letter to Mortgagor or Lender to Prevent Foreclosure.

- You can also access forms you previously downloaded in the My documents section of your account.

- If this is your first time using US Legal Forms, follow the steps below.

- Step 1. Ensure you've selected the form for your specific city/state.

- Step 2. Utilize the Review feature to examine the content of the form. Make sure to read the details.

- Step 3. If you're not satisfied with the form, use the Lookup field at the top of the screen to find alternative versions of the legal form template.

- Step 4. Once you have located the desired form, click the Get now button. Choose your preferred payment plan and provide your details to sign up for the account.

- Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the purchase.

- Step 6. Choose the format of your legal form and download it onto your device.

- Step 7. Complete, edit, and print or sign the Virgin Islands Hardship Letter to Mortgagor or Lender to Prevent Foreclosure.

Form popularity

FAQ

To write a foreclosure hardship letter, start with a clear and concise introduction stating your situation and request for assistance. Describe your financial hardships and outline any efforts you are taking to remedy the situation. Make sure to express your willingness to cooperate and seek solutions. By utilizing a Virgin Islands Hardship Letter to Mortgagor or Lender to Prevent Foreclosure, you can convey your message effectively.

In a hardship letter, refrain from including irrelevant information that doesn’t relate to your financial difficulties. Avoid making accusations against the lender or displaying despair; maintain a calm and professional tone. It is vital to stick to the facts and clearly outline your circumstances related to the mortgage. Clarity and relevance are key in your Virgin Islands Hardship Letter to Mortgagor or Lender to Prevent Foreclosure.

To write a hardship letter to stop foreclosure, start by clearly stating your request to halt the foreclosure proceedings. Provide an honest summary of your financial hardships and explain how they have affected your ability to meet mortgage payments. Additionally, include any steps you are taking to improve your financial situation. A well-crafted Virgin Islands Hardship Letter to Mortgagor or Lender to Prevent Foreclosure can improve your chances of getting the help you need.

In a hardship letter, avoid excessive personal details that do not pertain to your financial situation, as they may dilute your message. Additionally, do not make false claims or use overly technical language; clarity should be your priority. It's important to keep emotions in check and focus on facts. Sticking to relevant information will strengthen your Virgin Islands Hardship Letter to Mortgagor or Lender to Prevent Foreclosure.

An example of a hardship letter for a mortgage directly communicates the reasons for your financial difficulties. In the letter, detail the specific circumstances, such as job loss or medical expenses, that have impacted your finances. It should also express your commitment to resolving the situation and request assistance. This kind of letter is essential when using a Virgin Islands Hardship Letter to Mortgagor or Lender to Prevent Foreclosure.

Filling out a financial hardship form requires gathering specific financial information. Start by detailing your income, expenses, and any debts. Be sure to explain your current situation clearly, emphasizing your need for a Virgin Islands Hardship Letter to Mortgagor or Lender to Prevent Foreclosure. Consider using uslegalforms to guide you through this process, as they provide templates and resources to ensure your letter is effective and complete.

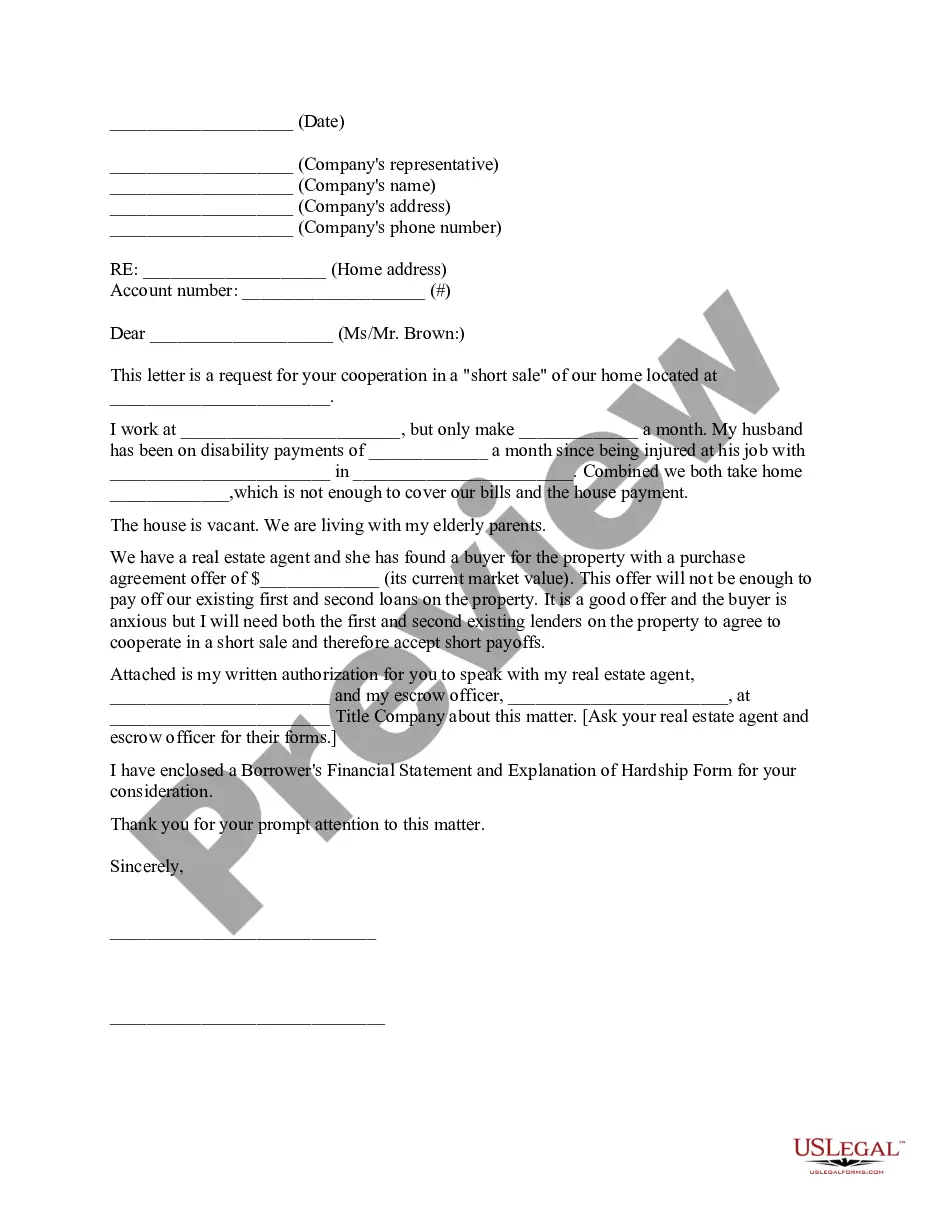

A hardship letter explains to a lender the circumstances that have made you unable to keep up with your debt payments. It provides specific details such as the date the hardship began, the cause and how long you expect it to continue.

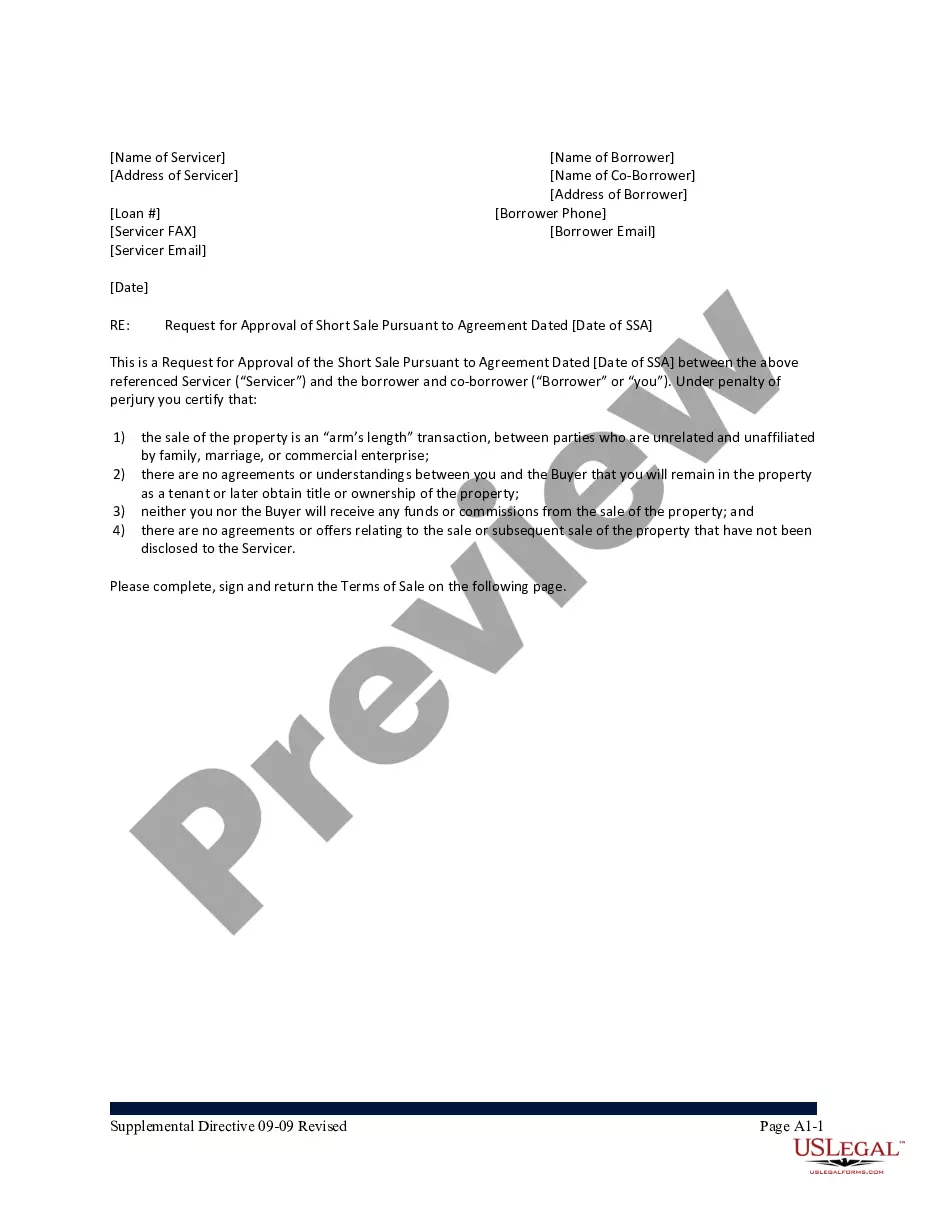

Loss mitigation options include temporary and long-term relief, including options that allow borrowers who are behind on their mortgage payments to remain in their homes or to leave their homes without a foreclosure, such as, without limitation, refinancing, trial or permanent modification, repayment of the amount owed

What Happens if My Mortgage Is Delinquent? For starters, your lender may charge you late fees. If you continue to miss payments, the lender may ultimately declare your mortgage to be in default and begin foreclosure proceedings to take your home away from you and sell it.

Even though a foreclosure could take months or years to complete, lenders could start the foreclosure process in as little as 30 to 90 days after your forbearance ends, if your servicer cannot contact you, says Mark McArdle, assistant director, mortgage markets at the CFPB.