Virgin Islands Waiver of Qualified Joint and Survivor Annuity - QJSA

Description

How to fill out Waiver Of Qualified Joint And Survivor Annuity - QJSA?

Selecting the most suitable authorized document template can be challenging. Of course, there are numerous designs accessible on the web, but how can you obtain the authorized type you need? Utilize the US Legal Forms website. This service offers a vast collection of templates, such as the Virgin Islands Waiver of Qualified Joint and Survivor Annuity - QJSA, suitable for both business and personal needs. All documents are verified by experts and conform to state and federal regulations.

If you are already registered, sign in to your account and then click the Download button to access the Virgin Islands Waiver of Qualified Joint and Survivor Annuity - QJSA. Use your account to review the authorized documents you have previously obtained. Navigate to the My documents section of your account to acquire another copy of the document you need.

For new users of US Legal Forms, here are simple steps to follow: First, ensure you have selected the correct form for your city/state. You can browse the form using the Preview button and read the form description to confirm that it is the right one for you. If the form does not meet your needs, use the Search field to find the appropriate form. Once you are confident that the form is correct, click the Buy now button to obtain the form. Select the pricing plan you want and enter the required information. Create your account and pay for the transaction using your PayPal account or credit card. Choose the file format and download the authorized document template to your device. Complete, revise, print, and sign the downloaded Virgin Islands Waiver of Qualified Joint and Survivor Annuity - QJSA.

- US Legal Forms boasts the largest collection of authorized documents from which you can discover a variety of file templates.

- Utilize the service to download correctly formatted documents that comply with state regulations.

- The templates available cater to various legal needs, ensuring you have access to professional quality forms.

- Each document has been crafted to guide you through your legal processes efficiently.

- You can easily manage all your documents using the online platform.

- Find peace of mind knowing that all forms are checked for legal validity.

Form popularity

FAQ

Utilizing the Virgin Islands Waiver of Qualified Joint and Survivor Annuity - QJSA offers several benefits. Primarily, it provides assured income for the surviving partner, which can help maintain their standard of living after loss. Additionally, this waiver allows individuals to customize their retirement plans, ensuring they align with personal and financial goals.

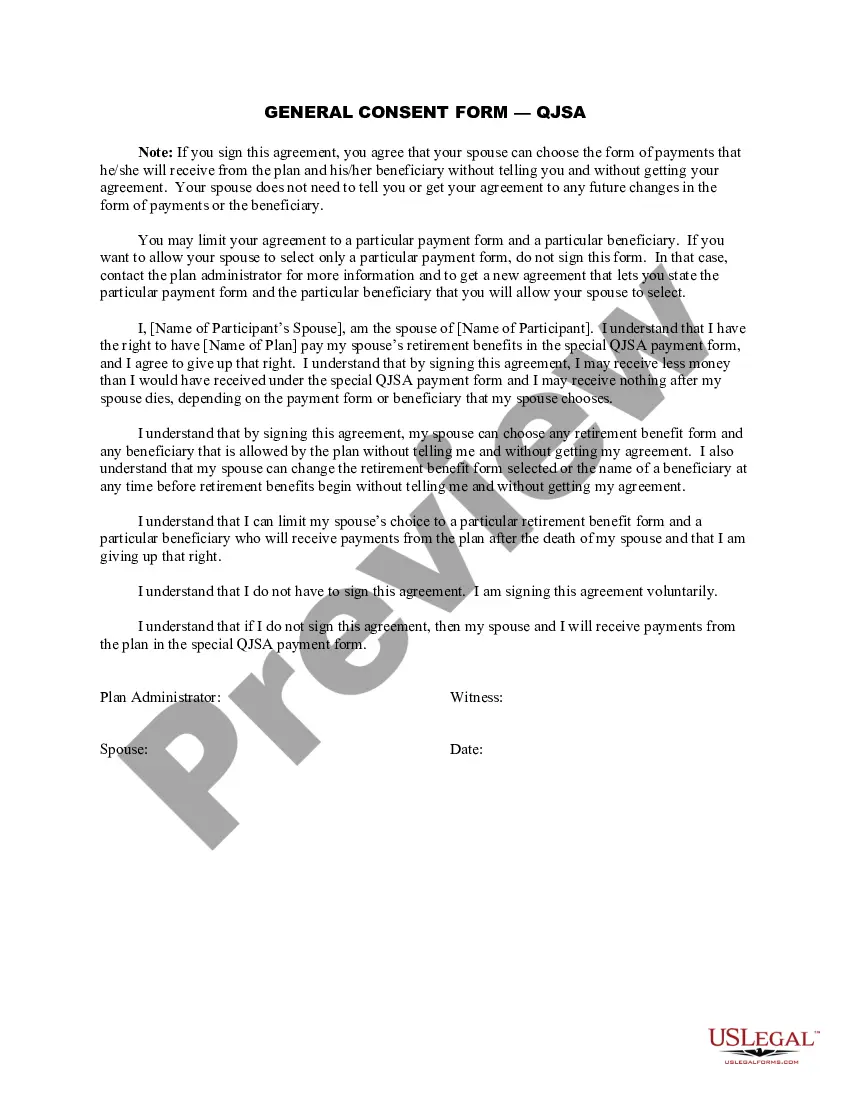

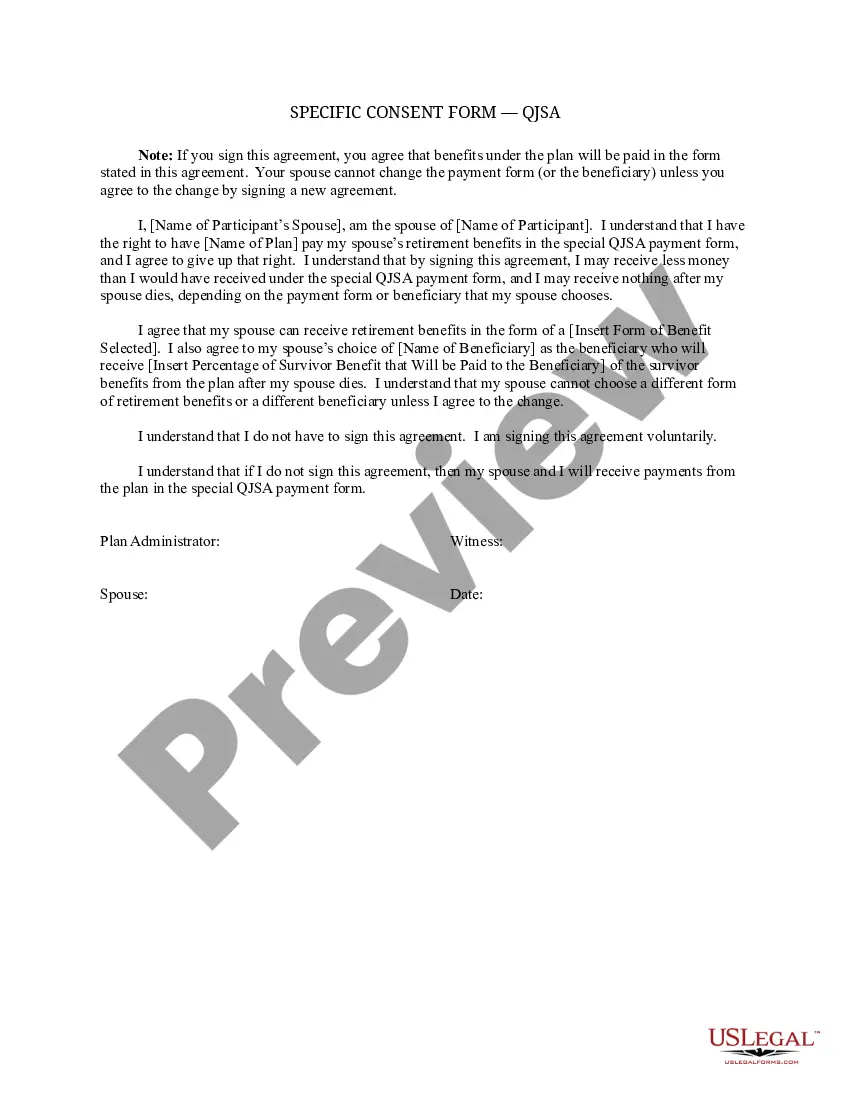

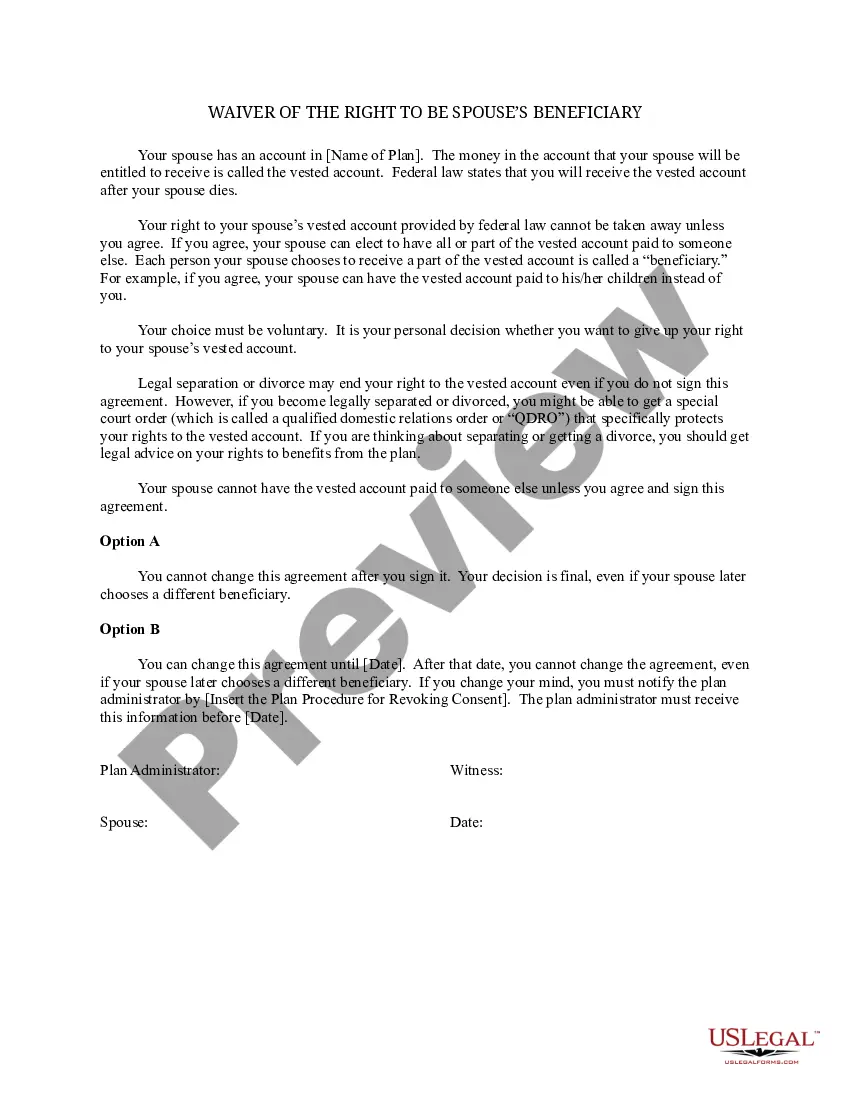

Qualified Joint and Survivor AnnuityIf your spouse consents to change the way the Plan's retirement benefits are paid, your spouse gives up his or her right to the QJSA payments. This is referred to as a waiver of the QJSA payment form.

life annuity provides the largest monthly payment but pays only during your lifetime. It's a poor choice if your spouse will need income from your pension to pay routine expenses. A jointandsurvivor annuity pays you during your lifetime and then continues to pay your spouse or other named beneficiary.

While joint and survivor annuities defer taxes, they don't allow you to avoid them completely. Once payments begin, you'll have to include those amounts as taxable income, which could increase your overall tax liability if you're also taking withdrawals from tax-deferred or taxable accounts.

Form 4 is used when the spouse of a member/former member of a pension plan agrees to waive or give up his or her right to receive survivor's benefits to permit the member/former member to designate a beneficiary other than the spouse for benefits in 2022 a pension plan, if pension payments have not started, 2022 a locked-in

More In Retirement Plans Alternatively, a participant who waives a QJSA may elect to have a qualified optional survivor annuity (QOSA). The amount paid to the surviving spouse under a QOSA is equal to the certain percentage (as chosen) of the amount of the annuity payable during the participant's life.

A qualified joint and survivor annuity (QJSA) provides a lifetime payment to an annuitant and spouse, child, or dependent from a qualified plan. QJSA rules apply to money-purchase pension plans, defined benefit plans, and target benefits.

A joint and survivor annuity is an insurance product designed for couples that continues to make regular payments as long as one spouse lives. A joint and survivor annuity has the advantage of providing income if one or both people live longer than expected. This is not a good choice for a younger couple.

A joint and survivor annuity is an annuity that pays out for the remainder of two people's lives. Depending on the contract, the annuity may pay 100 percent of the payments upon the death of the first annuitant or a lower percentage typically 50 or 75 percent.

Annuity payments you or your survivors receive after the total cost in the plan has been recovered are generally fully taxable.