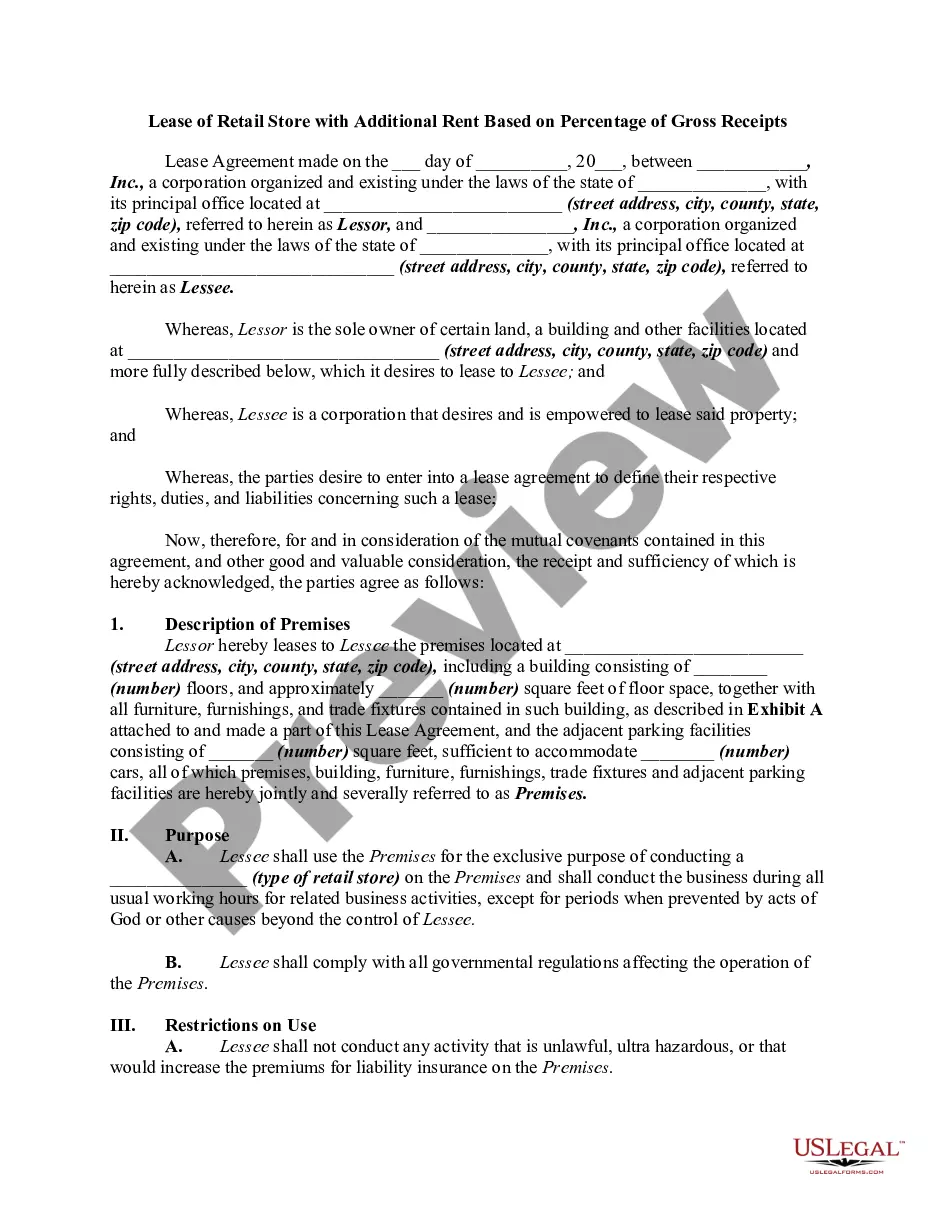

This form is a commercial lease of a building and land for the operation of a retail store with a set amount of rent along with a percentage of the gross receipts of the store as additional rent.

Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate

Instant download

Description

Free preview

How to fill out Lease Of Retail Store With Additional Rent Based On Percentage Of Gross Receipts - Real Estate?

Are you currently in a scenario where you require documents for either business or personal reasons almost every day.

There are numerous legal document templates accessible online, but finding ones you can trust is not simple.

US Legal Forms offers a vast array of template documents, including the Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate, which are designed to meet federal and state requirements.

Choose a suitable file format and download your copy.

Access all the document templates you have purchased in the My documents section. You can retrieve an additional copy of the Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate at any time if needed. Click on the desired form to download or print the document template.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- Then, you can download the Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate template.

- If you do not have an account and wish to use US Legal Forms, follow these steps.

- Find the form you need and ensure it is for the correct city/county.

- Utilize the Preview option to review the document.

- Read the description to make sure you have chosen the correct form.

- If the form does not meet your needs, use the Search area to locate the document that fits your requirements.

- Once you find the right form, click Purchase now.

- Select the pricing plan you want, fill in the necessary information to create your account, and pay for your order with your PayPal or credit card.

Form popularity

FAQ

In St. Thomas, the sales tax is applied to most transactions, impacting both consumers and retailers. For businesses under a Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate, understanding the sales tax implications is important to ensure correct tax handling. Consequently, retailers should stay informed about current rates and regulations to remain compliant and avoid penalties.

St. Thomas is often considered a favorable location for business due to its unique tax benefits, but it should not be labeled strictly as a tax haven. The Virgin Islands offer various incentives that can benefit businesses engaged in a Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate. However, understanding local laws and tax obligations is vital for leveraging these advantages correctly.

The gross receipts of a taxpayer in the Virgin Islands refer to the total revenue collected from all sources before any deductions or expenses. This figure is essential for businesses involved in a Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate. Accurate reporting of gross receipts ensures proper tax calculations and compliance with local regulations.

The Gross Receipts Tax in the Virgin Islands applies to all businesses operating in the territory. This tax is calculated on a percentage of the total revenue generated by the business, which includes sales generated under a Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate. Understanding this tax is crucial for retailers, as it impacts overall profitability and compliance.

The most common lease for retail spaces tends to be the modified gross lease, where the landlord and tenant share responsibilities for expenses. Yet, for many retail businesses, the Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate stands out. This agreement helps retailers focus on growth and enhances profitability, making it a preferred option in competitive markets.

The most common type of leasehold is the commercial leasehold, which grants tenants the right to use a property for business purposes. In retail, this commonly takes the form of leases like the Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate. This lease offers flexibility and a mutually beneficial arrangement between both landlords and retailers, driving revenue and successful business operations.

Percentage rent is calculated by applying a predetermined percentage to the tenant's gross sales exceeding a specified threshold. Typically, this is outlined in the lease agreement, like the Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate. To calculate, simply subtract the base amount from total sales, multiply the result by the agreed percentage, and ensure to keep track of sales accurately to avoid disputes.

In the retail sector, the most common lease form is the gross lease, where the landlord covers most operating expenses. However, many retail landlords prefer the Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate. This lease structure allows landlords to share in the success of the tenant's business through additional rent calculated on the store's gross sales.

Gross income generally consists of all income earned, but certain amounts may be excluded. For example, gifts, inheritance, and specific government payments do not count toward gross income. Understanding these exclusions helps maintain compliance and accurate financial reporting, especially for businesses operating under the Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate.

Filing a tax return in the US Virgin Islands involves submitting the appropriate forms to the Virgin Islands Bureau of Internal Revenue. You will typically report all sources of income, including any income derived from the Virgin Islands Lease of Retail Store with Additional Rent Based on Percentage of Gross Receipts - Real Estate. Utilizing platforms like uslegalforms can simplify this process with accurate document preparation.