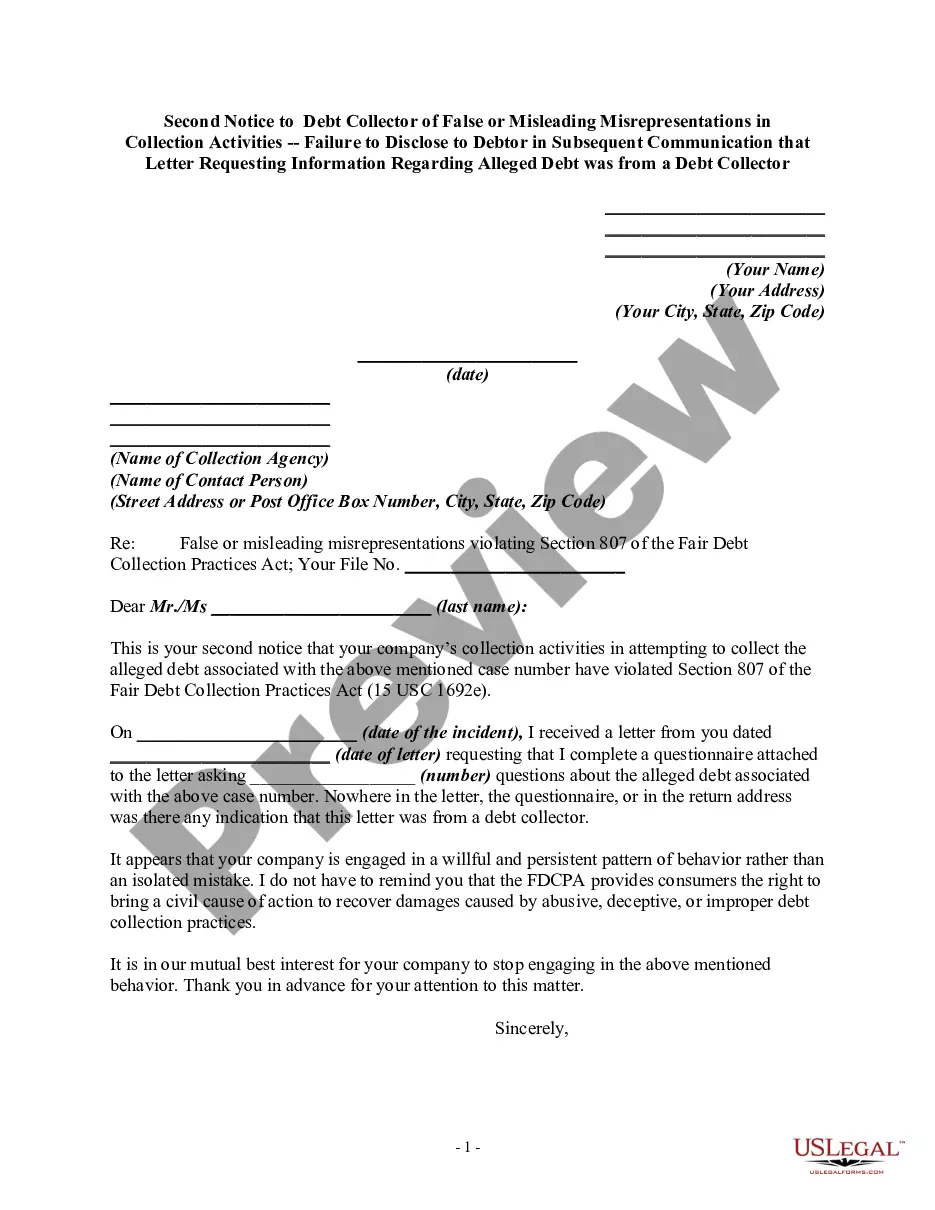

This form is a follow-up letter containing a warning that the debt collector's continued violation of the Fair Debt Collection Practices Act may result in a law suit being filed against the debt collector.

Virginia Second Notice to Debt Collector of Harassment or Abuse in Collection Activities Involving Threats to Use Violence or other Criminal Means to Harm the Physical Person, Reputation, and/or Property of the Debtor

Category:

State:

Multi-State

Control #:

US-DCPA-18.2BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Second Notice To Debt Collector Of Harassment Or Abuse In Collection Activities Involving Threats To Use Violence Or Other Criminal Means To Harm The Physical Person, Reputation, And/or Property Of The Debtor?

It is feasible to invest hours online looking for the legal documents template that satisfies the state and federal requirements you will require.

US Legal Forms offers a vast selection of legal forms that are evaluated by professionals.

You can easily download or print the Virginia Second Notice to Debt Collector of Harassment or Abuse in Collection Activities Involving Threats to Use Violence or other Criminal Means to Harm the Physical Person, Reputation, and/or Property of the Debtor from our platform.

If available, use the Preview button to review the document template as well.

- If you currently possess a US Legal Forms account, you can Log In and hit the Acquire button.

- Subsequently, you can complete, modify, print, or sign the Virginia Second Notice to Debt Collector of Harassment or Abuse in Collection Activities Involving Threats to Use Violence or other Criminal Means to Harm the Physical Person, Reputation, and/or Property of the Debtor.

- Every legal document template you buy is yours indefinitely.

- To obtain an extra copy of any purchased form, navigate to the My documents section and click the corresponding button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions listed below.

- First, ensure you have selected the correct document template for the state/city of your choice.

- Review the document description to confirm you have chosen the appropriate form.

Form popularity

FAQ

USLegalForms offers a variety of legal document templates, including tools to craft your own Virginia Second Notice to Debt Collector of Harassment or Abuse in Collection Activities Involving Threats to Use Violence or other Criminal Means to Harm the Physical Person, Reputation, and/or Property of the Debtor. By utilizing these resources, you can ensure your rights are recognized and defended against abusive collection practices.

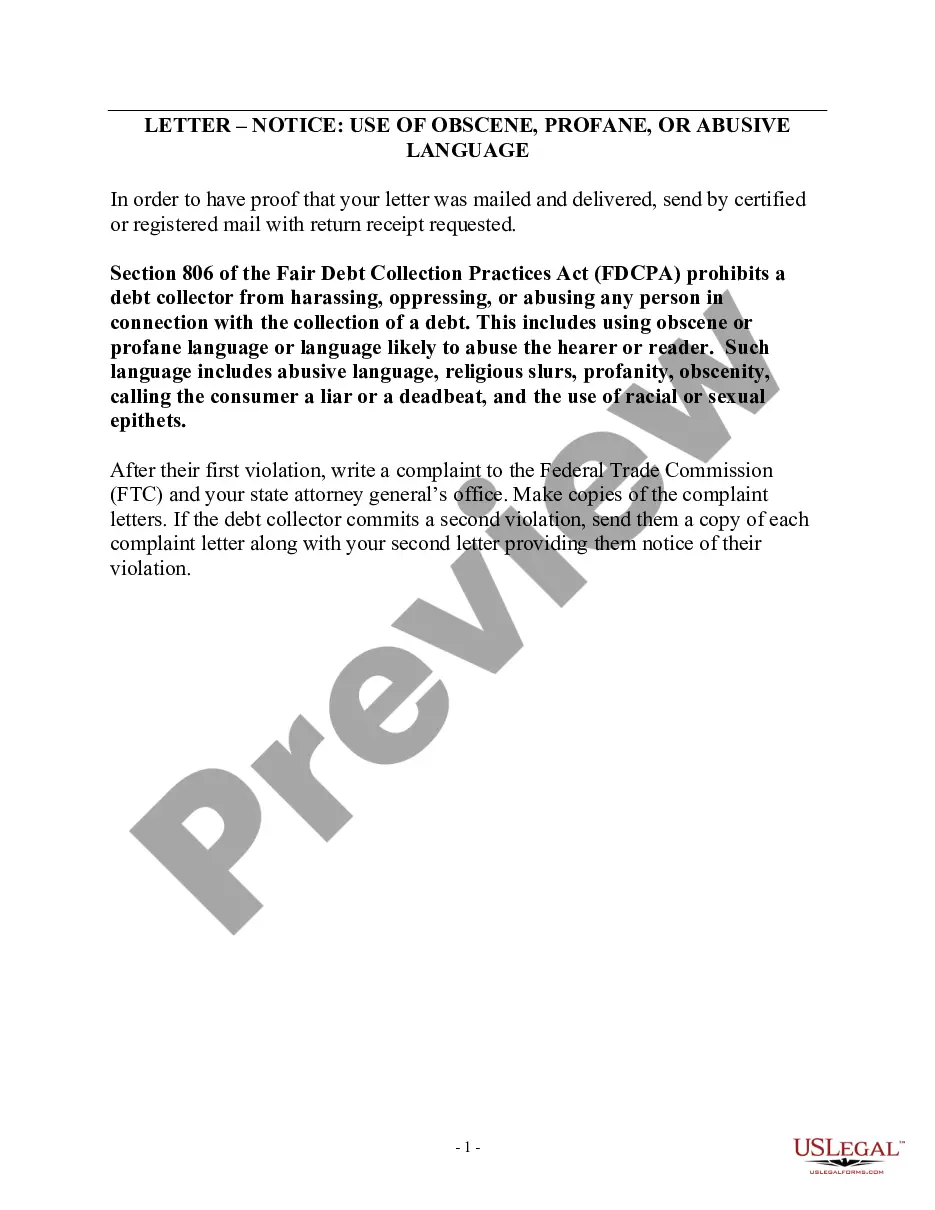

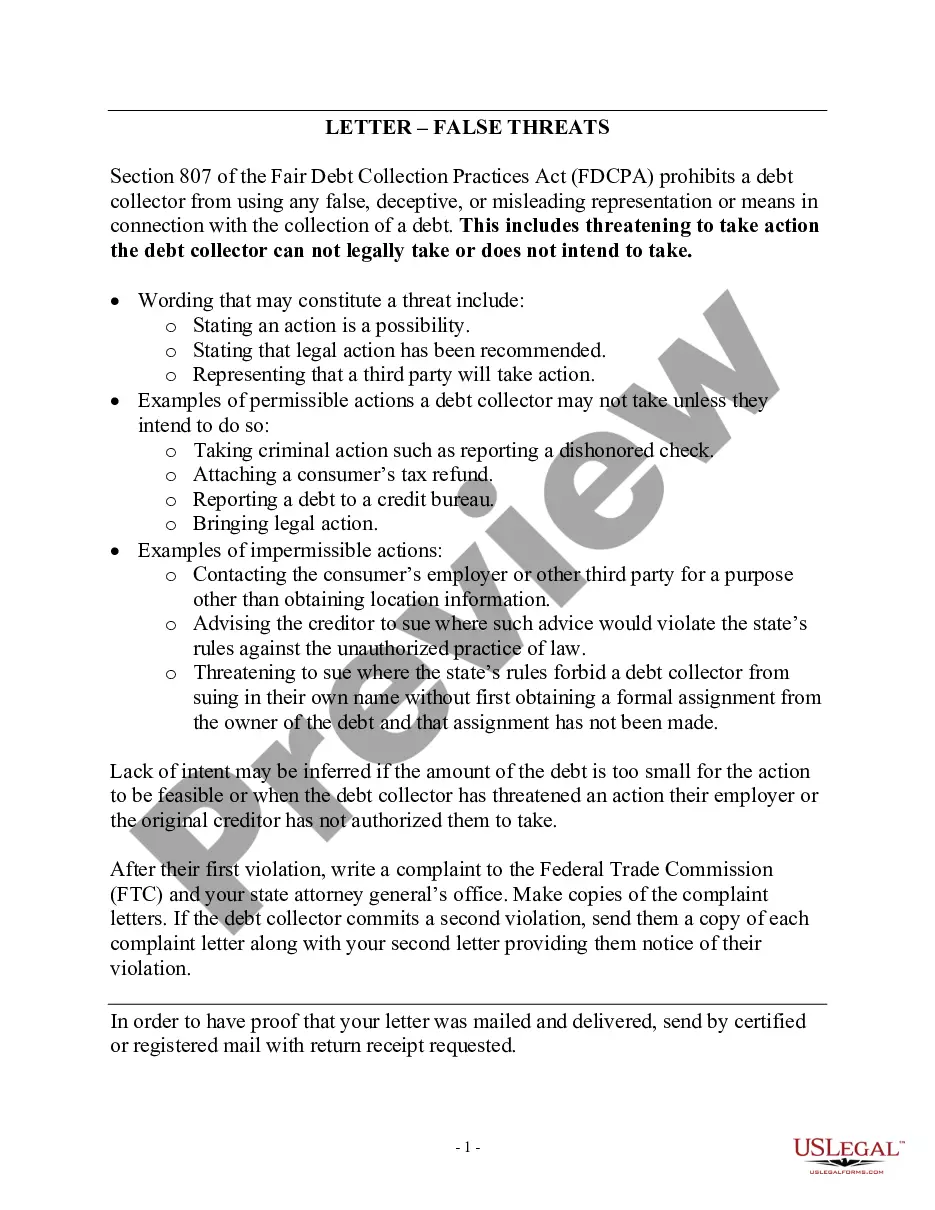

No harassment The Fair Debt Collection Practices Act (FDCPA) says debt collectors can't harass, oppress, or abuse you or anyone else they contact. Some examples of harassment are: Repetitious phone calls that are intended to annoy, abuse, or harass you or any person answering the phone. Obscene or profane language.

As we have discussed in harassment cases, a cease and desist letter is used to formally demand the harasser stops their behavior.

Fortunately, there are legal actions you can take to stop this harassment:Write a Letter Requesting To Cease Communications.Document All Contact and Harassment.File a Complaint With the FTC.File a Complaint With Your State's Agency.Consider Suing the Debt Collection Agency for Harassment.

Here are a few suggestions that might work in your favor:Write a letter disputing the debt. You have 30 days after receiving a collection notice to dispute a debt in writing.Dispute the debt on your credit report.Lodge a complaint.Respond to a lawsuit.Hire an attorney.

Fortunately, there are legal actions you can take to stop this harassment:Write a Letter Requesting To Cease Communications.Document All Contact and Harassment.File a Complaint With the FTC.File a Complaint With Your State's Agency.Consider Suing the Debt Collection Agency for Harassment.

If you believe a debt collector is harassing you, you can submit a complaint with the CFPB online or by calling (855) 411-CFPB (2372). You can also contact your state's attorney general .

Under the FDCPA, you can tell a debt collector to stop contacting you; but it's not always a good idea. The federal Fair Debt Collection Practices Act (FDCPA) gives you the right to force a debt collector to stop communicating with you.

As far as verbal abuse goes, Ontario, Alberta, New Brunswick and Nova Scotia are among the provinces that state that collection agents cannot use profane, intimidating, or "coercive" language when dealing with debtors. Alberta and Northwest Territories also mention that collection agents may not threaten physical harm.

The first thing to do is to write the debt collector a letter telling them to stop calling you. You can use the sample letter language here. Under the FDCPA, they must follow your written request for no contact. If they do not, you can report them to the Federal Trade Commission (FTC).