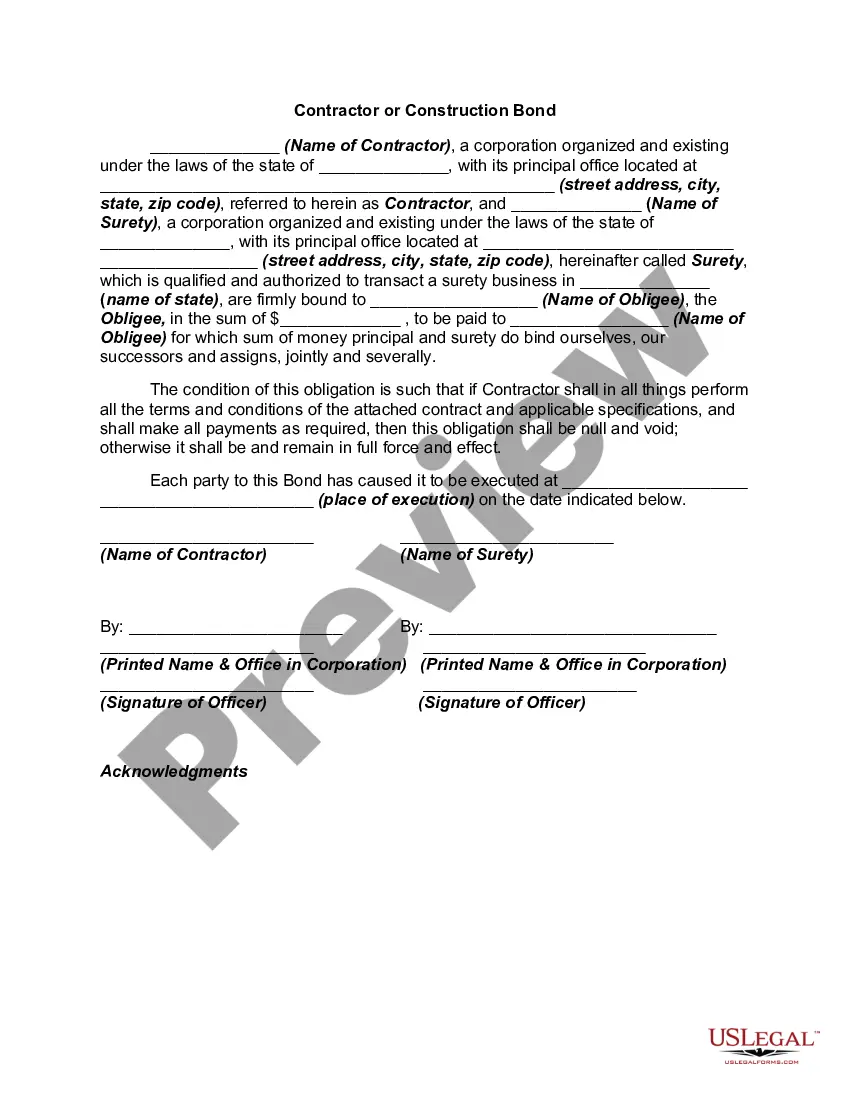

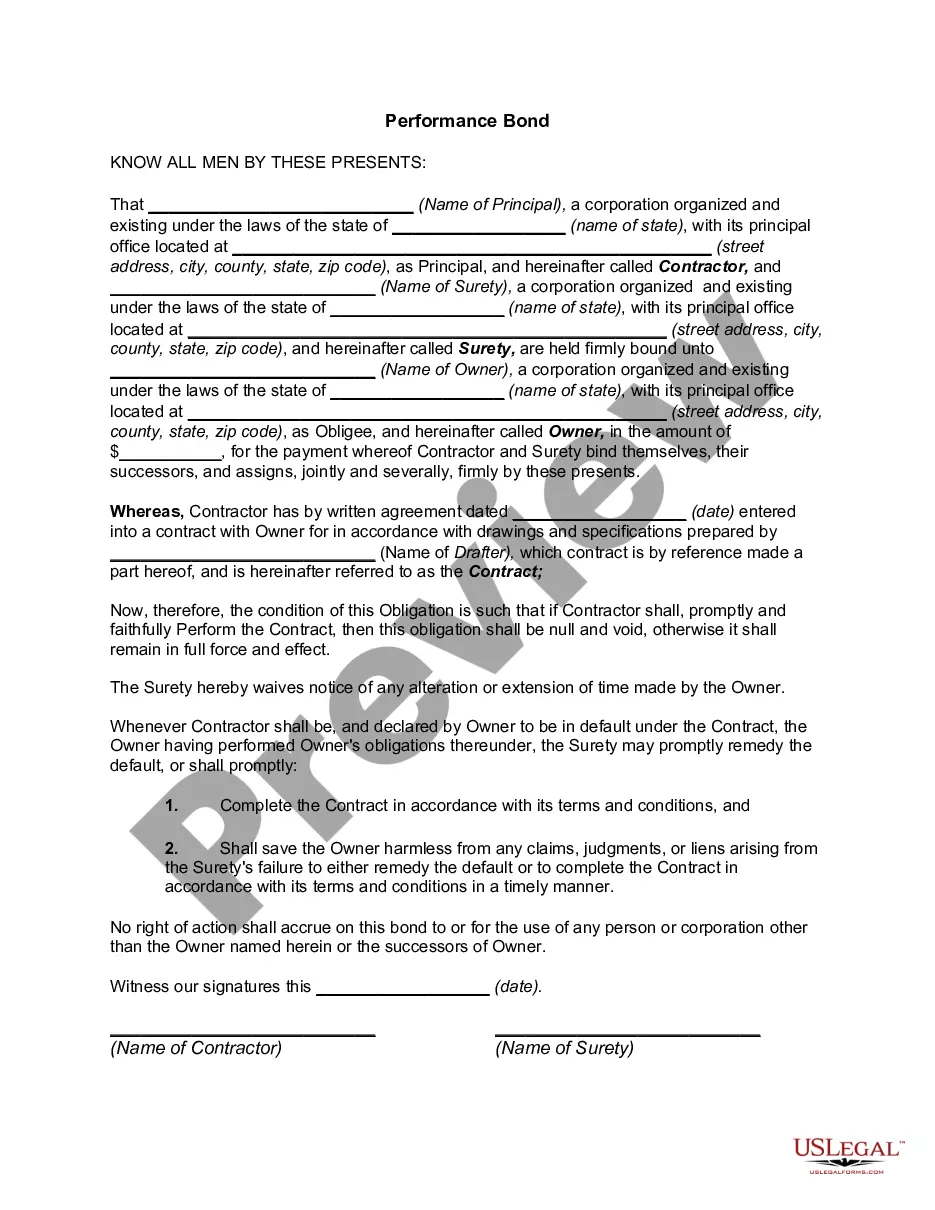

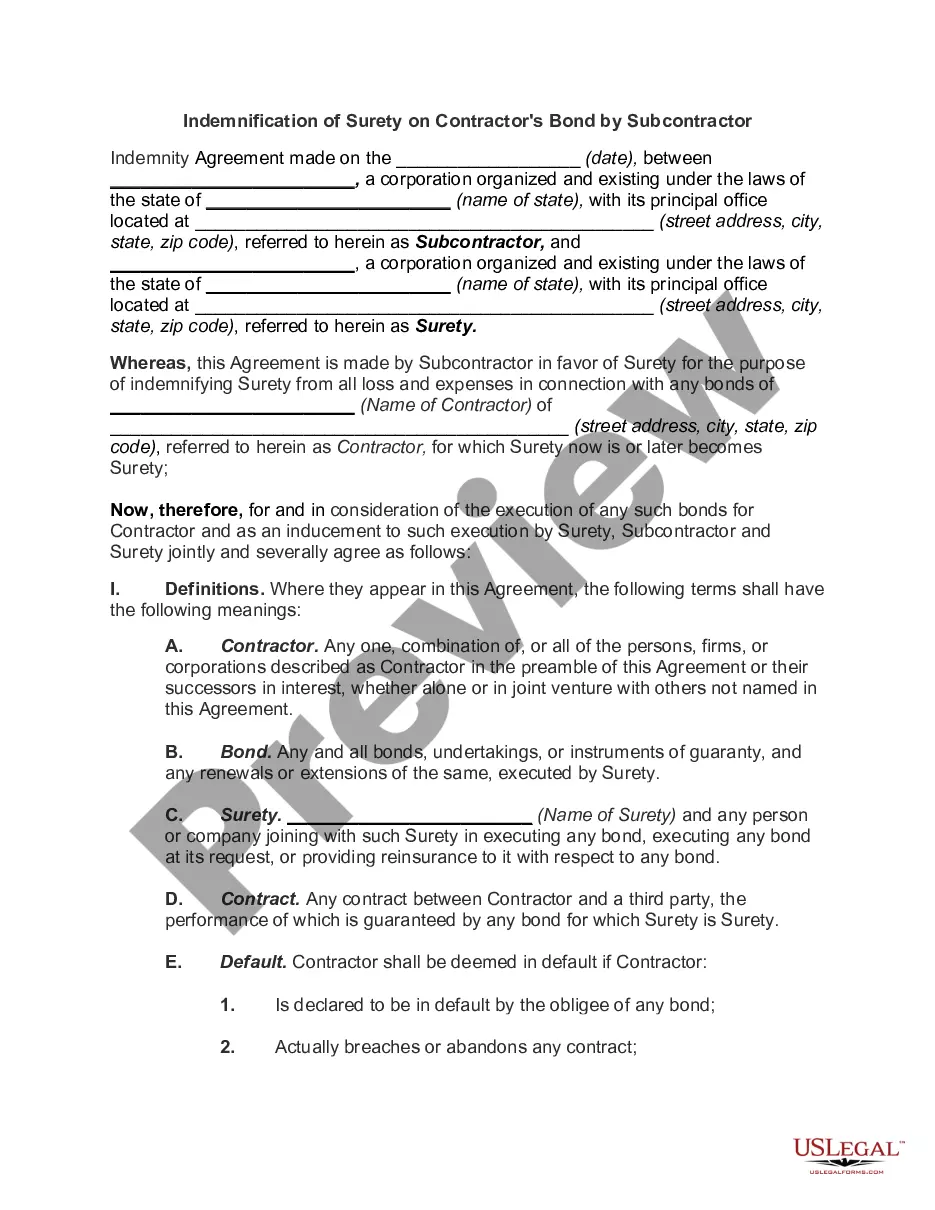

Virginia Subcontractor's Performance Bond

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Subcontractor's Performance Bond?

If you wish to full, acquire, or produce legal document themes, use US Legal Forms, the most important variety of legal kinds, that can be found on-line. Make use of the site`s basic and convenient look for to find the papers you need. Different themes for organization and individual purposes are categorized by classes and states, or keywords and phrases. Use US Legal Forms to find the Virginia Subcontractor's Performance Bond within a few click throughs.

If you are already a US Legal Forms buyer, log in for your bank account and click on the Down load button to find the Virginia Subcontractor's Performance Bond. You may also access kinds you earlier saved inside the My Forms tab of your bank account.

If you work with US Legal Forms initially, refer to the instructions beneath:

- Step 1. Ensure you have selected the shape to the correct metropolis/region.

- Step 2. Utilize the Review choice to check out the form`s content material. Never forget to read through the description.

- Step 3. If you are not satisfied with the type, take advantage of the Lookup industry on top of the monitor to get other variations in the legal type web template.

- Step 4. When you have located the shape you need, click on the Get now button. Pick the pricing strategy you like and add your accreditations to sign up for an bank account.

- Step 5. Process the deal. You can utilize your credit card or PayPal bank account to accomplish the deal.

- Step 6. Select the structure in the legal type and acquire it on your own gadget.

- Step 7. Total, revise and produce or indication the Virginia Subcontractor's Performance Bond.

Every single legal document web template you buy is your own property permanently. You might have acces to each and every type you saved in your acccount. Select the My Forms section and choose a type to produce or acquire again.

Contend and acquire, and produce the Virginia Subcontractor's Performance Bond with US Legal Forms. There are many professional and status-distinct kinds you may use for the organization or individual needs.

Form popularity

FAQ

To get a contractor license in the state of Virginia, you must either demonstrate a certain amount of net worth or get a $50,000 contractor license bond. Similarly, to get registered in certain counties in the state, such as Prince William County or Fairfax County you must also post a surety bond.

Performance Bonds A performance bond guarantees satisfactory performance of all duties specified in the contract. Examples would the labor of all sub-contractors, suppliers, and payment of materials. The principal will require the performance bond once awarded the contract.

The State of Virginia does not require contractors to obtain any form of liability insurance. Class A and B contractors will need to purchase and maintain a $50,000 contractor license surety bond.

Virginia doesn't require liability insurance for general contractors, but coverage may be required to obtain certain permits. It can offer important financial protection to keep your business moving forward.

A payment surety bond is a legal contract, a type of bond, that guarantees certain employees, subcontractors, and suppliers are protected against non-payment. Other common names for these include 'construction', and 'labor and material'.

?The main purpose of a construction bond is to provide the security, or guarantee, to the owner that the project he instructs the contractor to build will be completed in the case of failure or bankruptcy of the contractor's company,? says Robbert.

A performance bond is a financial guarantee to one party in a contract against the failure of the other party to meet its obligations. It is also referred to as a contract bond. A performance bond is usually provided by a bank or an insurance company to make sure a contractor completes designated projects.

When a contractor fails to abide by any of the conditions of the contract, the surety and contractor are both held liable. The three main types of construction bonds are bid, performance, and payment.