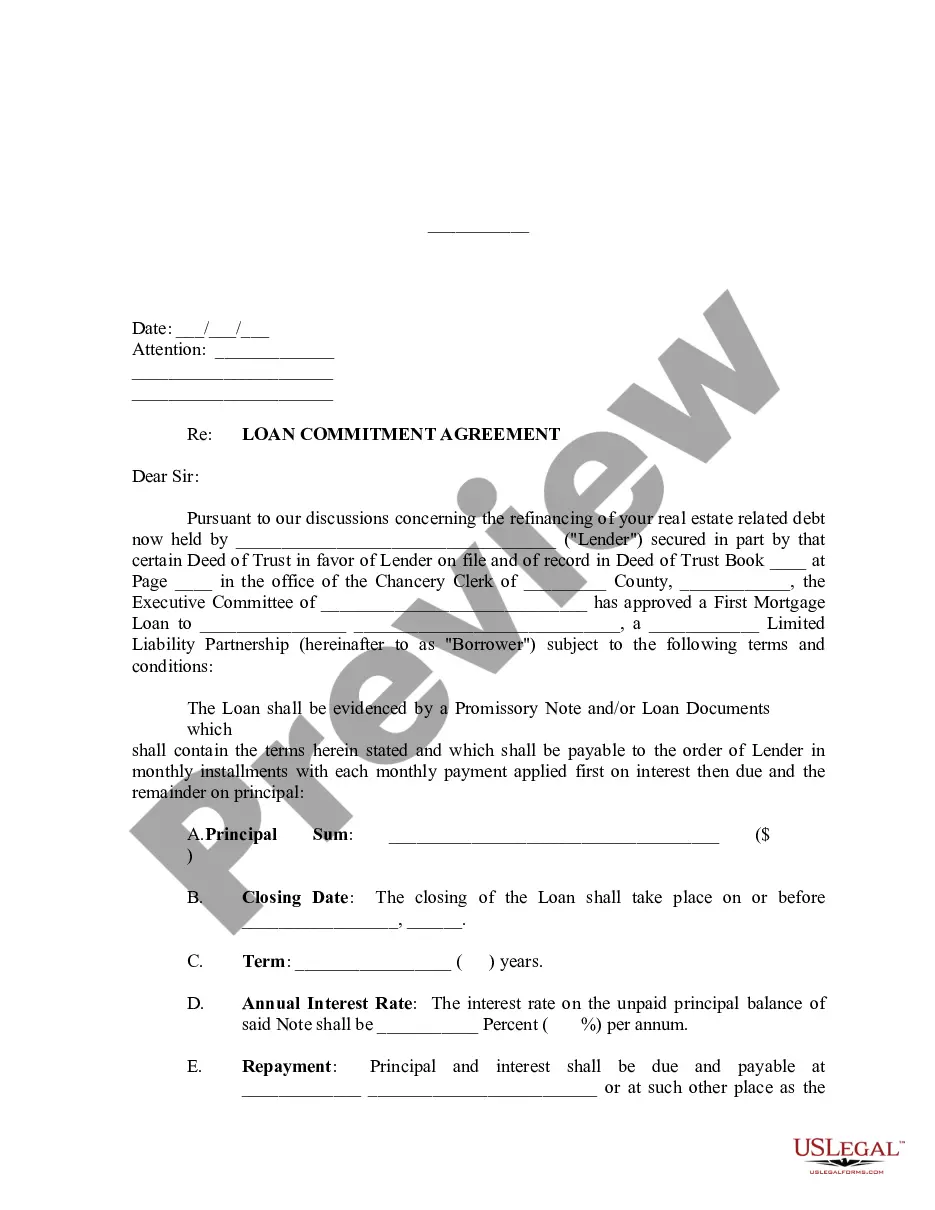

Virginia Loan Commitment Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Loan Commitment Agreement?

Have you been in a placement that you need papers for sometimes business or specific uses almost every day time? There are plenty of legitimate file themes available on the Internet, but getting ones you can rely on is not straightforward. US Legal Forms delivers thousands of form themes, just like the Virginia Loan Commitment Agreement, that happen to be composed to fulfill state and federal requirements.

Should you be currently knowledgeable about US Legal Forms web site and possess a merchant account, just log in. Afterward, it is possible to obtain the Virginia Loan Commitment Agreement web template.

If you do not offer an profile and wish to start using US Legal Forms, abide by these steps:

- Discover the form you want and ensure it is for the appropriate city/county.

- Use the Preview switch to analyze the form.

- See the explanation to ensure that you have chosen the correct form.

- When the form is not what you are trying to find, utilize the Search discipline to get the form that fits your needs and requirements.

- If you get the appropriate form, click Purchase now.

- Opt for the pricing prepare you want, complete the necessary information and facts to produce your money, and buy the order utilizing your PayPal or bank card.

- Decide on a hassle-free paper format and obtain your backup.

Locate each of the file themes you may have bought in the My Forms menus. You may get a more backup of Virginia Loan Commitment Agreement whenever, if needed. Just select the essential form to obtain or print the file web template.

Use US Legal Forms, probably the most considerable assortment of legitimate types, to conserve time as well as stay away from blunders. The assistance delivers appropriately produced legitimate file themes which you can use for a range of uses. Make a merchant account on US Legal Forms and begin making your way of life a little easier.

Form popularity

FAQ

Does A Loan Commitment Letter Mean I'm Approved? After you're preapproved, you'll receive a conditional mortgage commitment letter. That does not mean you're approved for the loan. With this conditional approval, you'll still have steps to take in the mortgage application process.

A commitment is not synonymous with an approval. While receiving a firm commitment or a conditional commitment are both positive pieces of news on your homebuying journey (especially the firm letter), this isn't the end of the application process.

As long as nothing changes financially with the applicant during the house hunting phase and the home's appraisal value covers the loan amount, the loan commitment generally stands. However, the lender reserves the right to reduce the loan amount or deny the application.

The qualification of the loan is dependent on the borrower's income and credit history. A loan commitment is when a financial institution makes an agreement to lend a certain amount of cash to an individual or business.

Of Title 6.2 of the Code of Virginia. "Commitment" means a written offer to make a mortgage loan signed by a person authorized to sign such offers on behalf of a mortgage lender. "Commitment agreement" means a commitment accepted by an applicant for a mortgage loan, as evidenced by the applicant's signature thereon.

The must-have details in your loan commitment letter are the lender's and borrower's information, loan type and amount, repayment agreement, and loan expiration.

A mortgage commitment letter includes the amount being borrowed, the interest rate, and the length of the loan. There will also be conditions attached, such as the requirement to carry homeowner's insurance. A lender can still deny a loan at closing if these conditions have not been met.

A loan commitment is an agreement by a commercial bank or other financial institution to lend a business or individual a specified sum of money. A loan commitment is useful for consumers looking to buy a home or a business planning to make a major purchase.