Virginia Partial Assignment of Life Insurance Policy as Collateral

Description

How to fill out Partial Assignment Of Life Insurance Policy As Collateral?

If you want to complete, acquire, or print legal record templates, use US Legal Forms, the greatest variety of legal varieties, that can be found online. Take advantage of the site`s simple and handy search to get the documents you want. Numerous templates for business and person reasons are categorized by categories and states, or search phrases. Use US Legal Forms to get the Virginia Partial Assignment of Life Insurance Policy as Collateral in just a couple of clicks.

When you are currently a US Legal Forms consumer, log in in your accounts and then click the Obtain switch to get the Virginia Partial Assignment of Life Insurance Policy as Collateral. You may also gain access to varieties you earlier downloaded within the My Forms tab of your accounts.

If you use US Legal Forms the very first time, follow the instructions listed below:

- Step 1. Be sure you have selected the form for that correct area/region.

- Step 2. Take advantage of the Preview option to check out the form`s content. Don`t forget to learn the outline.

- Step 3. When you are not happy together with the kind, make use of the Look for area at the top of the screen to discover other variations of your legal kind web template.

- Step 4. After you have located the form you want, go through the Purchase now switch. Pick the rates program you favor and add your qualifications to register for an accounts.

- Step 5. Method the purchase. You can use your Мisa or Ьastercard or PayPal accounts to accomplish the purchase.

- Step 6. Find the format of your legal kind and acquire it in your product.

- Step 7. Comprehensive, change and print or indicator the Virginia Partial Assignment of Life Insurance Policy as Collateral.

Every single legal record web template you acquire is your own for a long time. You may have acces to each kind you downloaded inside your acccount. Click the My Forms section and choose a kind to print or acquire yet again.

Remain competitive and acquire, and print the Virginia Partial Assignment of Life Insurance Policy as Collateral with US Legal Forms. There are thousands of specialist and state-specific varieties you can use for the business or person requires.

Form popularity

FAQ

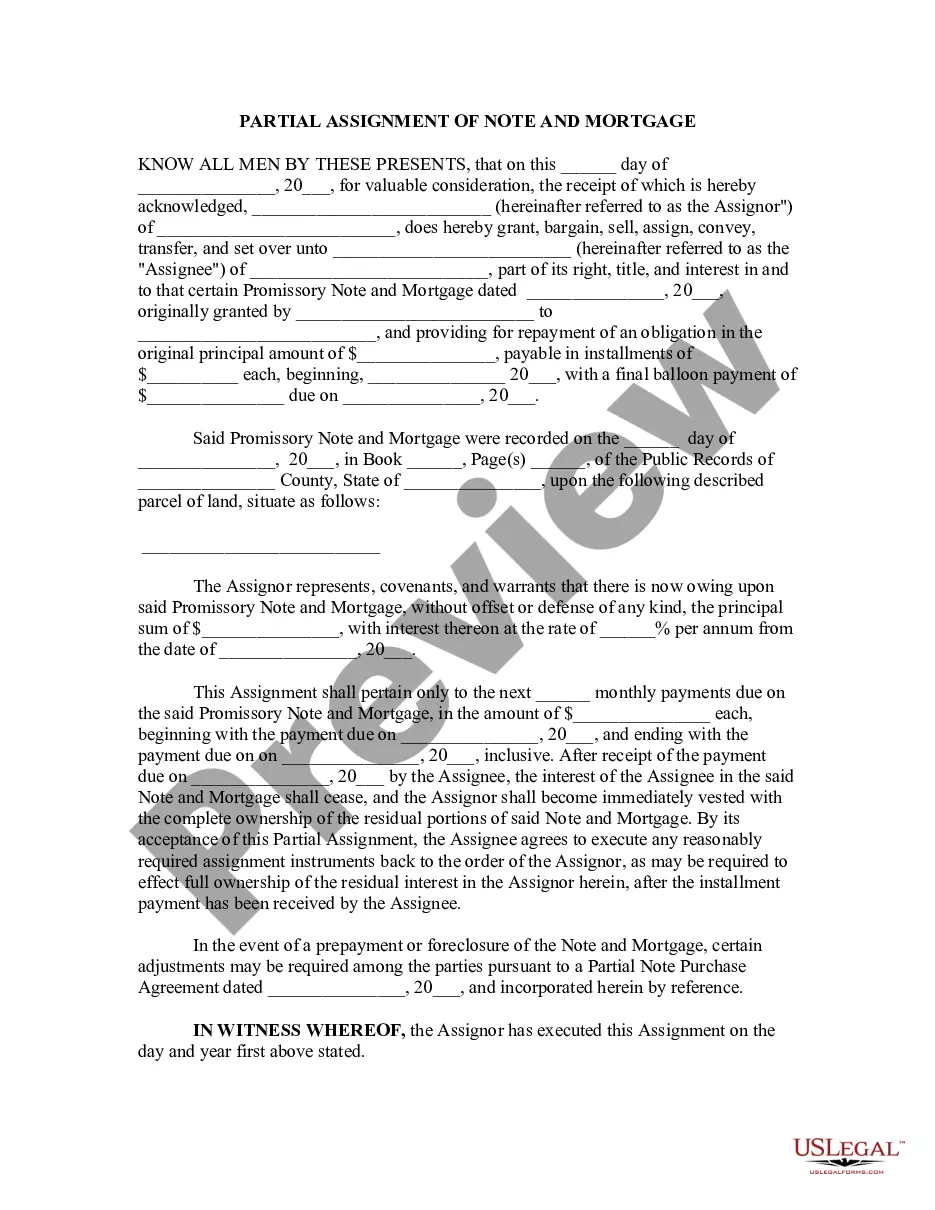

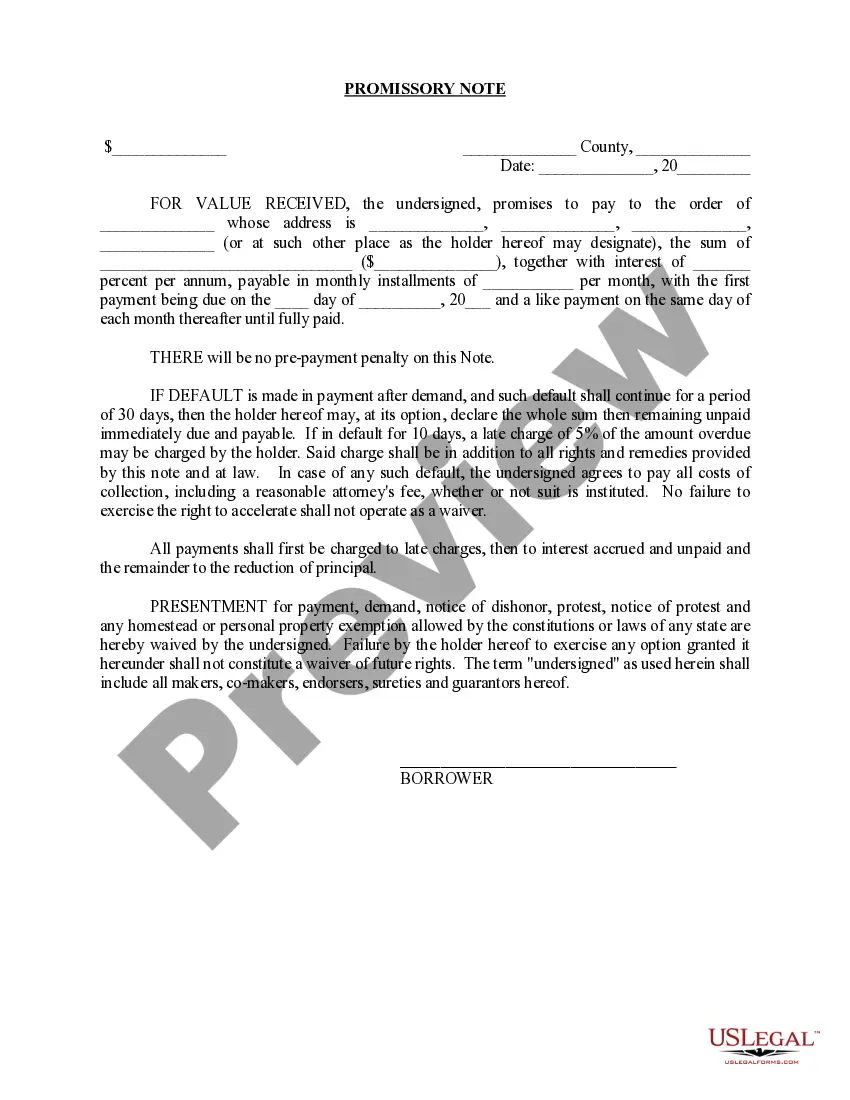

Collateral assignment of life insurance is a method of providing a lender with collateral when you apply for a loan. In this case, the collateral is your life insurance policy's face value, which could be used to pay back the amount you owe in case you die while in debt.

Under partial assignment, only the designated amount is paid to the assignee. Rest of the proceeds are paid to the nominee. If your expected insurance proceeds are more than the loan amount, you should opt for partial assignment.

With an absolute assignment, the entire ownership of the policy would be transferred to the assignee, or the lender. Then, the lender would be entitled to the full death benefit. With a collateral assignment, the lender is only entitled to the balance of the outstanding loan.

People often assign their life insurance policies to banks. A bank becomes the policy owner in this case, while the original policyholder continues to be the life assured whose death may be claimed by either the bank or the policy owner.

Under partial assignment, only the designated amount is paid to the assignee. Rest of the proceeds are paid to the nominee. If your expected insurance proceeds are more than the loan amount, you should opt for partial assignment.

A collateral assignment of life insurance is a conditional assignment appointing a lender as an assignee of a policy. Essentially, the lender has a claim to some or all of the death benefit until the loan is repaid. The death benefit is used as collateral for a loan.

Which of these actions is taken when a policyowner uses a Life Insurance policy as collateral for a bank loan? Collateral assignment" A policyowner using the Life Insurance policy as collateral for a bank loan normally would make a collateral assignment.

Collateral assignment, on the other hand, is a temporary and often revocable arrangement. The policyholder retains ownership and control over the policy but agrees that the lender has a claim to a part of the death benefit if the loan is not repaid.