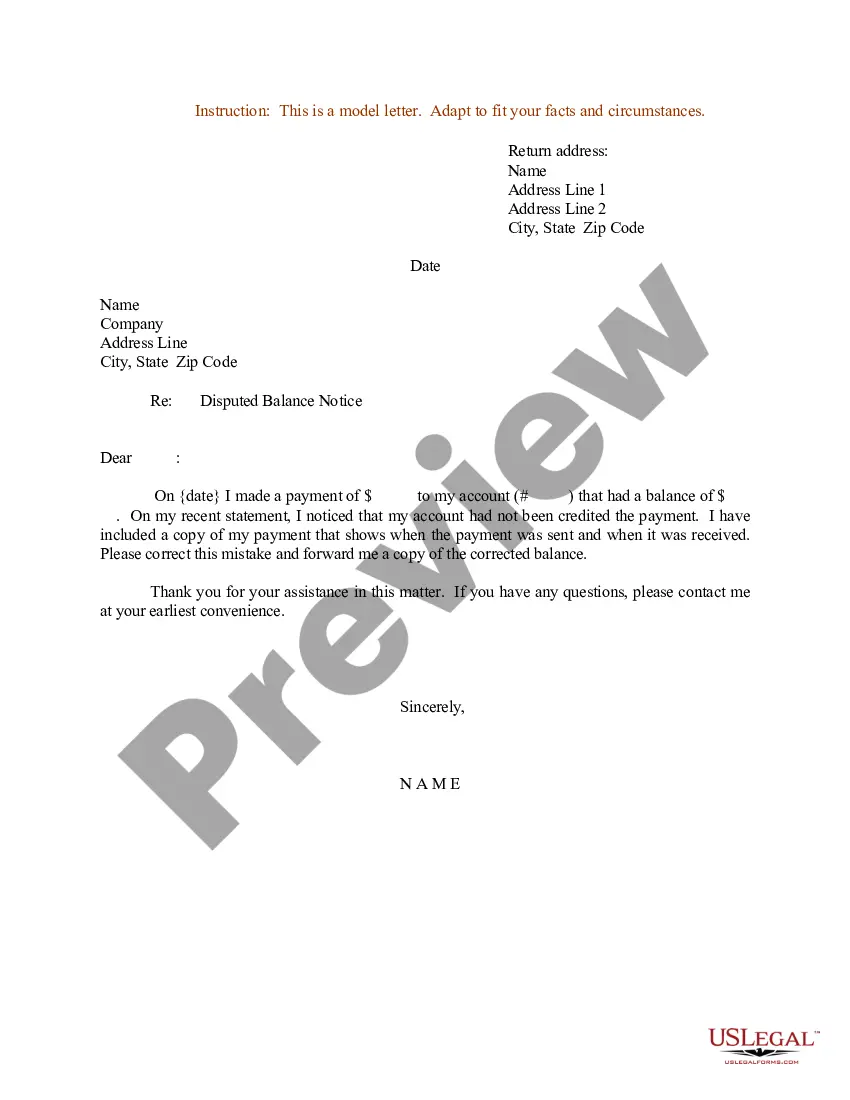

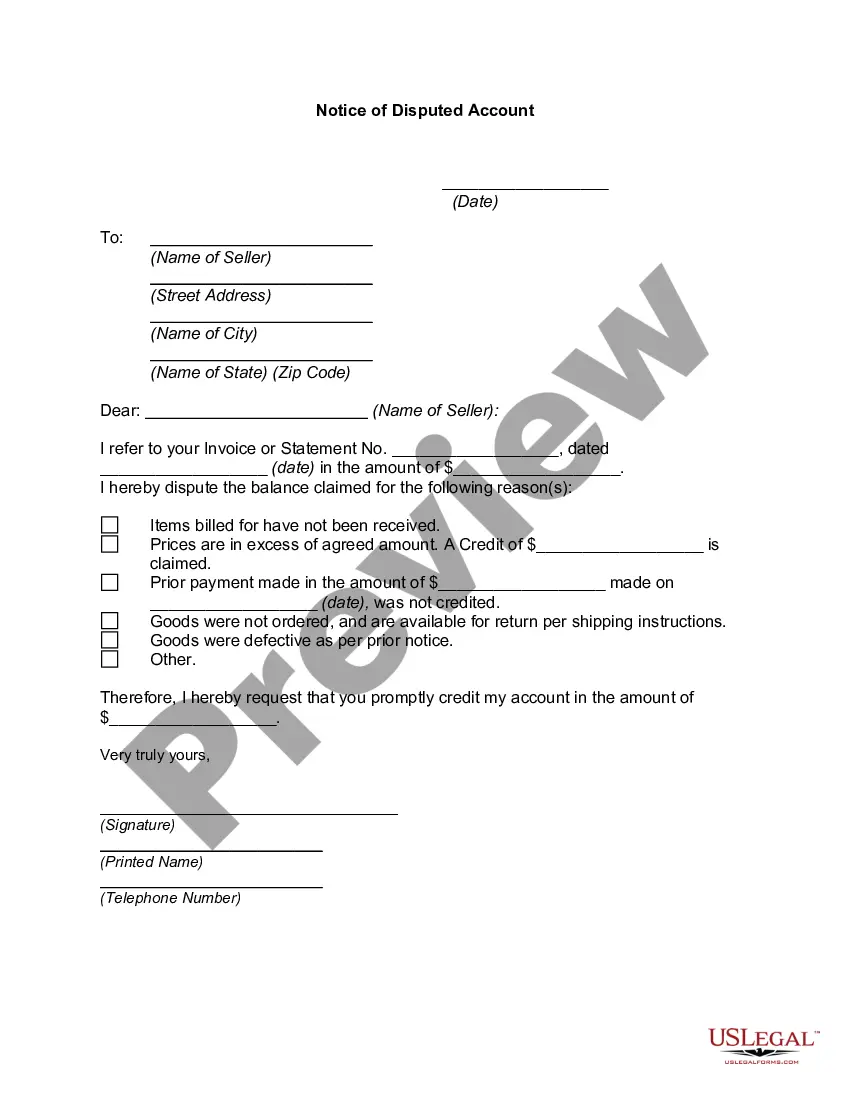

This form is to be used when a collection company is demanding full payment from you and you disagree with the balance. Use this form as your first letter of dispute.

Utah Letter of Dispute - Complete Balance

Instant download

Description

Free preview

How to fill out Letter Of Dispute - Complete Balance?

Finding the appropriate legal document template can be challenging. Clearly, there are numerous templates accessible online, but how can you locate the legal form you require? Utilize the US Legal Forms website. The service offers thousands of templates, including the Utah Letter of Dispute - Complete Balance, which can be utilized for both business and personal purposes. All templates are reviewed by experts and comply with state and federal regulations.

If you are already registered, Log In to your account and click the Download button to obtain the Utah Letter of Dispute - Complete Balance. Use your account to browse through the legal documents you have previously purchased. Navigate to the My documents section of your account and obtain another copy of the document you need.

If you are a new user of US Legal Forms, here are simple steps for you to follow: First, ensure that you have selected the correct form for your city/county. You can view the form using the Preview button and read the form description to confirm it is suitable for you. If the form does not meet your needs, use the Search field to find the appropriate form. Once you are confident the form is correct, click the Purchase now button to obtain the form. Select the payment plan you prefer and enter the required information. Create your account and complete the transaction using your PayPal account or credit card. Choose the file format and download the legal document template to your device. Finally, complete, edit, print, and sign the acquired Utah Letter of Dispute - Complete Balance.

By leveraging US Legal Forms, you can easily navigate the challenges of finding and obtaining legal templates that meet your needs.

- US Legal Forms is the largest repository of legal templates where you can discover a range of document templates.

- Utilize the service to download well-crafted documents that adhere to state standards.

- Ensure you review your selected templates carefully before finalizing your purchase.

- Take advantage of the preview and description features to verify suitability.

- Explore the variety of formats available for your downloaded documents.

- Follow the payment instructions accurately to avoid issues with your transaction.

Form popularity

FAQ

When disputing a collection, it's best to clearly express your reasons for the dispute and request specific action. You might say something like, 'I believe this debt is inaccurate and I request verification of the details.' Using the Utah Letter of Dispute - Complete Balance from US Legal Forms can help you articulate your dispute effectively, ensuring that you address all important points and maintain a professional tone.

A 609 letter is a type of letter you send to credit reporting agencies to request the removal of collections from your credit report. It references Section 609 of the Fair Credit Reporting Act, which gives you the right to request information about debts. When you use the Utah Letter of Dispute - Complete Balance template from US Legal Forms, you can effectively draft a 609 letter that outlines your request clearly and professionally.

To write a collection dispute letter, start by clearly stating your intention to dispute the debt. Include your personal information, the creditor's details, and a reference to the specific debt. In your letter, outline the reasons for your dispute, and request validation of the debt. Using the Utah Letter of Dispute - Complete Balance template from US Legal Forms can simplify this process and ensure you include all necessary details.

Writing a letter to dispute debt involves outlining your concerns clearly and concisely. Begin with your contact information, followed by the creditor's details, and specify the exact nature of the dispute. Incorporating the Utah Letter of Dispute - Complete Balance can provide a framework that highlights the critical points to cover, ultimately increasing your chances of a successful dispute.

To dispute a debt successfully, gather all relevant documentation, and clearly state your dispute in writing. Utilize the Utah Letter of Dispute - Complete Balance to ensure your letter is effective and meets legal requirements. Sending this letter to the creditor can prompt them to investigate your claims thoroughly, which often leads to a favorable resolution for you.

In Utah, the statute of limitations for most debts is typically four years. This means creditors have four years to file a lawsuit to collect a debt. After this period, the debt becomes uncollectible, and you can use the Utah Letter of Dispute - Complete Balance to formally challenge any attempts by creditors to collect on such debts. Understanding this timeframe can empower you in managing your financial obligations.

Writing a debt dispute letter requires clarity and precision. Begin by stating your intention clearly, including the details of the debt you are disputing. Make sure to reference the account number and the nature of the dispute. Using the Utah Letter of Dispute - Complete Balance template from US Legal Forms can help you ensure that all necessary information is included.

Writing a 609 credit dispute letter involves referencing your rights under the Fair Credit Reporting Act. Begin by including your personal information and the details of the credit report in question. Clearly state the inaccuracies you wish to dispute and request the removal of those items. Utilize the Utah Letter of Dispute - Complete Balance for a structured approach to ensure your letter is professional and compliant.

To write a letter disputing a debt, start by clearly stating your intention to dispute the amount owed. Include your personal information, the creditor’s details, and a description of the debt you are disputing. Be specific about why you believe the debt is incorrect, and request verification. Using the Utah Letter of Dispute - Complete Balance can help you craft a clear and effective letter.

When communicating with debt collectors, avoid making statements that could weaken your position, such as admitting to the debt without verification. Do not provide unnecessary personal information or make promises you cannot keep. Instead, use the Utah Letter of Dispute - Complete Balance to assert your rights and maintain a professional tone. This approach helps protect you from potential pitfalls during the dispute process.