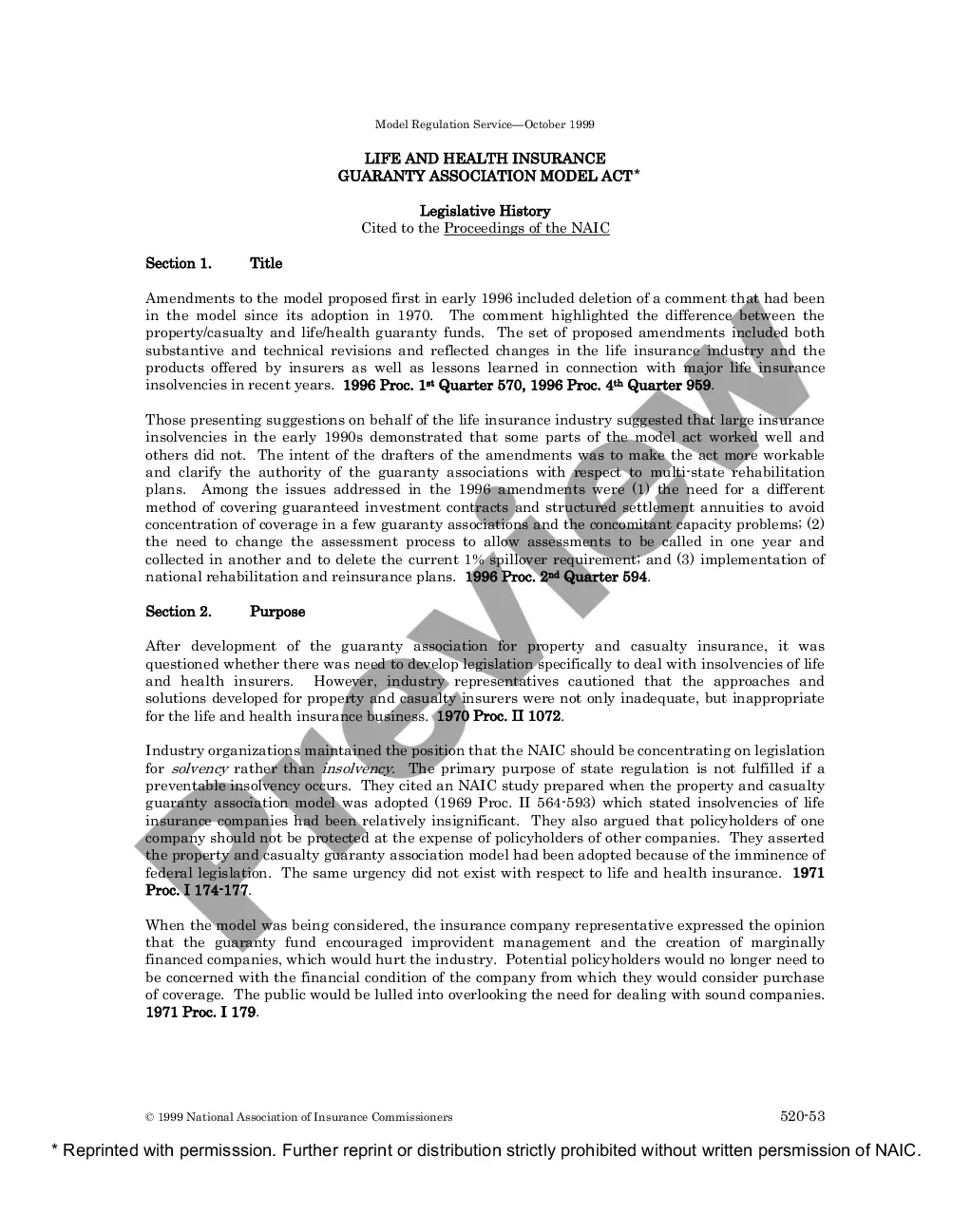

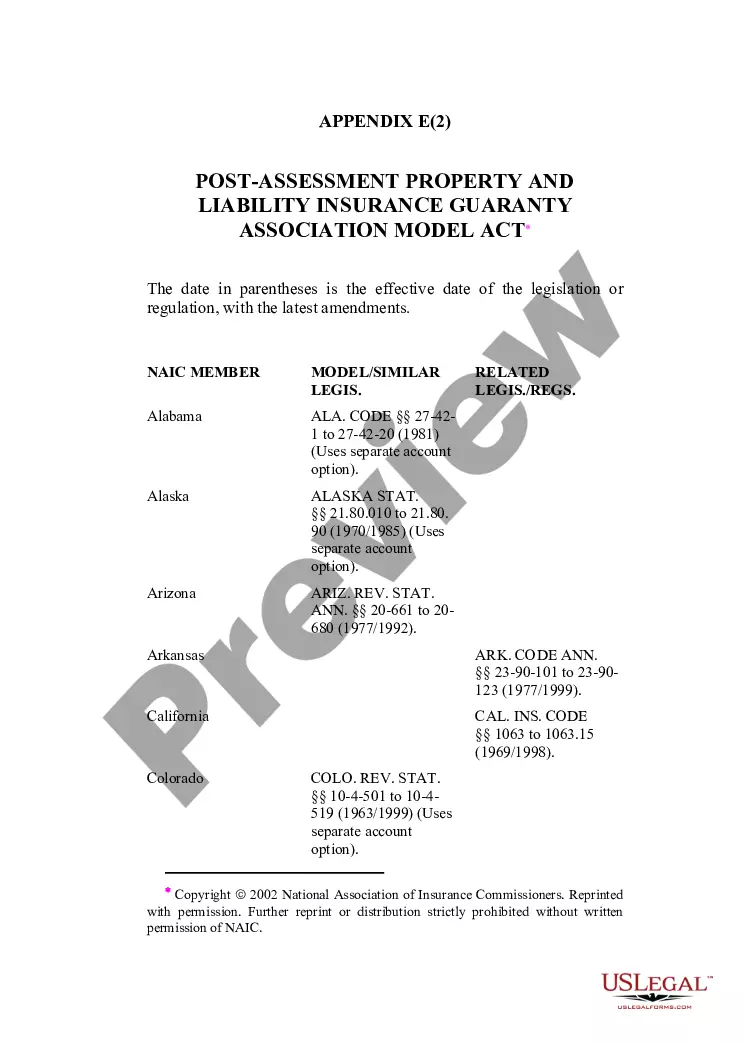

Full text of legislative history behind the Insurers Rehabilitation and Liquidation Model Act.

Insurers Rehabilitation and Liquidation Model Act Legislative History

State:

Multi-State

Control #:

US-AF02

Format:

PDF

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Insurers Rehabilitation And Liquidation Model Act Legislative History?

Employ the most extensive legal catalogue of forms. US Legal Forms is the best place for finding up-to-date Insurers Rehabilitation and Liquidation Model Act Legislative History templates. Our service offers thousands of legal documents drafted by licensed lawyers and grouped by state.

To get a sample from US Legal Forms, users simply need to sign up for an account first. If you are already registered on our platform, log in and choose the template you are looking for and buy it. After purchasing templates, users can see them in the My Forms section.

To get a US Legal Forms subscription on-line, follow the steps listed below:

- Find out if the Form name you’ve found is state-specific and suits your needs.

- When the form has a Preview option, utilize it to review the sample.

- If the template does not suit you, make use of the search bar to find a better one.

- PressClick Buy Now if the sample corresponds to your requirements.

- Choose a pricing plan.

- Create an account.

- Pay with the help of PayPal or with the debit/bank card.

- Select a document format and download the template.

- Once it is downloaded, print it and fill it out.

Save your time and effort using our service to find, download, and fill in the Form name. Join a huge number of delighted subscribers who’re already using US Legal Forms!

Form popularity

FAQ

Liquidation in finance and economics is the process of bringing a business to an end and distributing its assets to claimants. It is an event that usually occurs when a company is insolvent, meaning it cannot pay its obligations when they are due.

Example of a Liquidation The liquidation value is calculated by subtracting the liabilities from the auction value, which is $750,000 minus $550,000, or $200,000.

The liquidation approach is a method of business valuation. It measures the total worth of a company's physical assets that could potentially be sold if it were to be liquidated in the immediate future rather than run as a going concern.

2) Estimated liquidation price is just an estimate. When an account actually gets liquidated will depend on multiple factors including the performance of all contracts your account holds a position in, the currency your collateral is in, and other factors.

The Liquidation Analysis reflects estimates of the proceeds that might be realized through the liquidation of the Debtors, in accordance with chapter 7 of the Bankruptcy Code.A chapter 7 trustee would be either elected by creditors or appointed by the Bankruptcy Court to administer the estates.

The reason is that the liquidation or breakup of a company is a catalyst for the realization of underlying business value. Since value investors attempt to buy securities trading at a considerable discount from the value of a business's underlying assets, a liquidation is one way for investors to realize profits.

Liquidation value is the net value of a company's physical assets if it were to go out of business and the assets sold. The liquidation value is the value of company real estate, fixtures, equipment, and inventory. Intangible assets are excluded from a company's liquidation value.

To determine the value of a business in forced liquidation, an appraiser estimates what the likely price would be for each asset the business owns if it were sold at auction after only 60 to 90 days of advertising. He then adds the prices of all assets together to determine the business's forced liquidation value.

What Is Liquidation? Liquidation in finance and economics is the process of bringing a business to an end and distributing its assets to claimants. It is an event that usually occurs when a company is insolvent, meaning it cannot pay its obligations when they are due.