Line of Credit Promissory Note

What this document covers

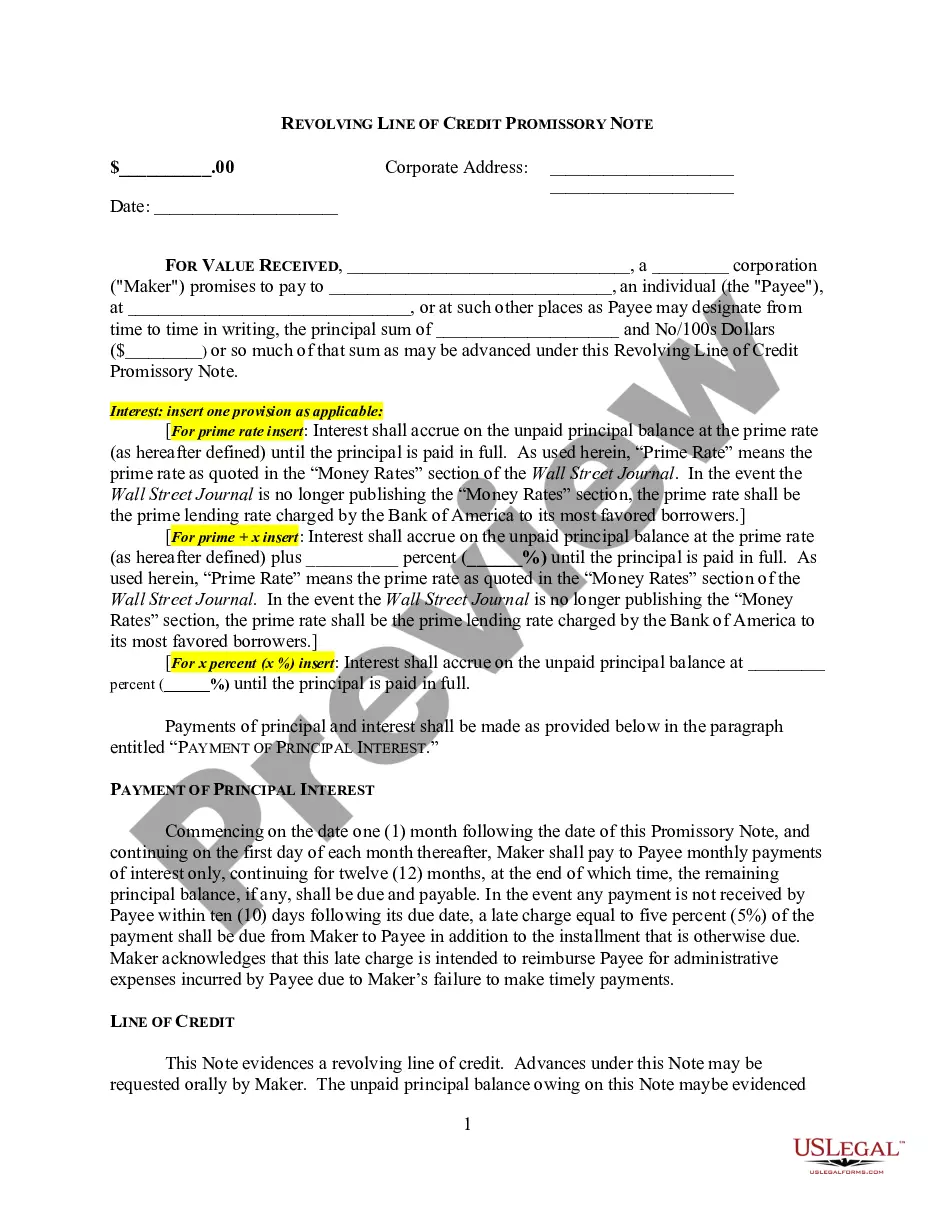

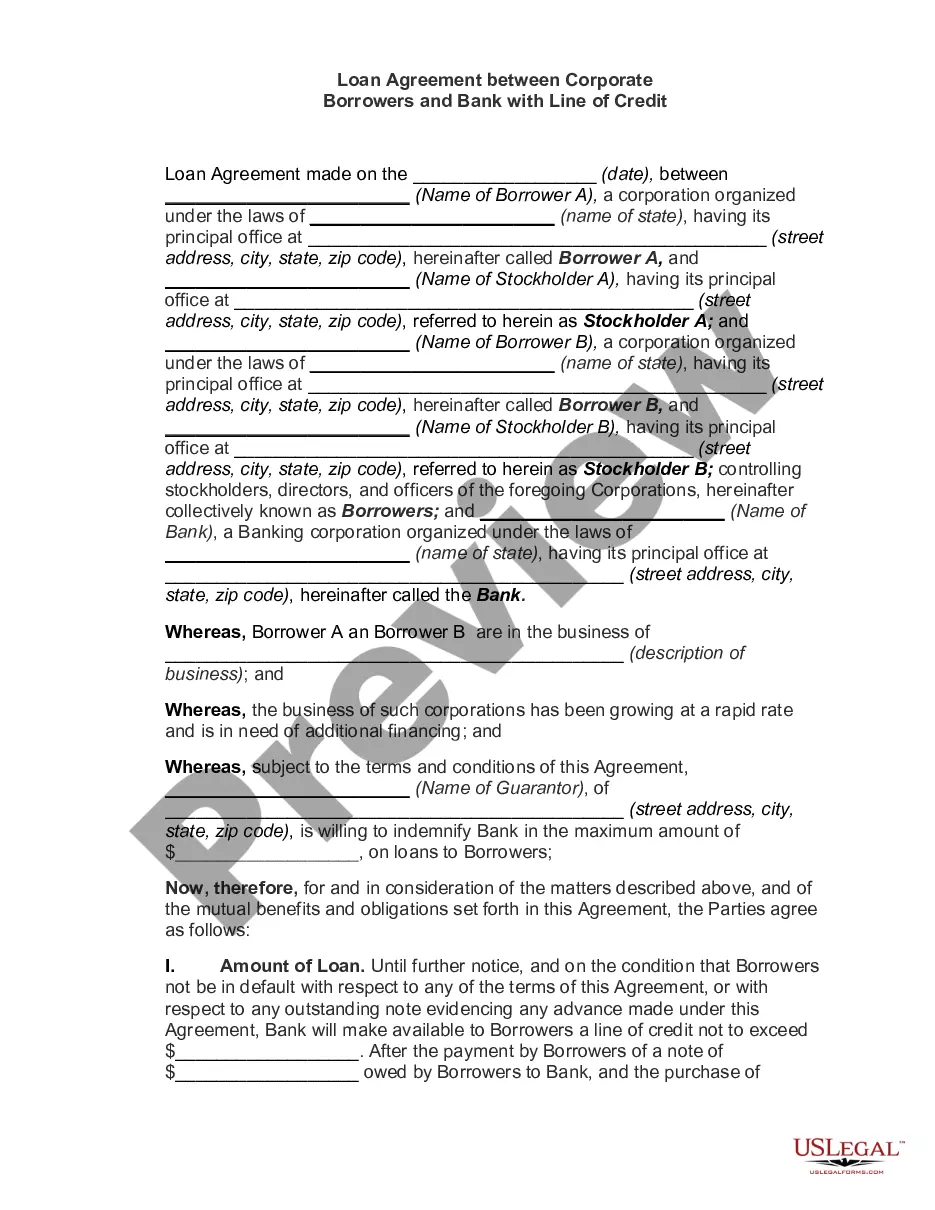

A Line of Credit Promissory Note is a legal document wherein a borrower agrees to repay the lender for funds borrowed within a specified limit, along with interest. This form is secured by collateral property, providing the lender a means of protection in case of default. Unlike other loan agreements that may require the loan to be paid in full upfront, a line of credit allows borrowers to access funds as needed up to the prescribed amount, making it a flexible financing option.

Form components explained

- Borrower and Lender Information: Names and contact details of both parties.

- Principal Amount: The maximum amount the borrower can draw from the line of credit.

- Interest Rate: The rate at which interest will accrue on the unpaid balance.

- Payment Terms: Details on when payments are due and any penalties for late payments.

- Security Clause: Information regarding the collateral that secures the note.

- Default Conditions: Circumstances under which the borrower would be considered in default and the lender's rights in that event.

State law considerations

This form is suitable for use across multiple states but may need changes to align with your state’s laws. Review and adapt it before final use.

When to use this form

This form is useful when an individual or business needs a flexible line of credit for various financial needs. Situations may include managing cash flow, covering unexpected expenses, or funding ongoing projects. Utilizing this promissory note ensures that both parties have a clear understanding of repayment terms, interest rates, and obligations, reducing the risk of disputes.

Who can use this document

This form is intended for:

- Individuals seeking a personal line of credit.

- Small businesses needing a flexible financing solution for operational costs.

- Creditors and lenders looking to draft a legally binding agreement for a line of credit.

- Borrowers who prefer secured loans with collateral.

How to prepare this document

- Identify the parties involved: Fill in the names and addresses of the borrower and lender.

- Specify the principal amount: Enter the total line of credit available to the borrower.

- Set the interest rate: Input the annual interest percentage that will be applied to the unpaid balance.

- Detail payment terms: Indicate when the principal and interest payments are due.

- Complete the security clause: Provide specifics about the property being used as collateral for the loan.

- Review and sign: Ensure both parties sign the note to validate the agreement.

Does this form need to be notarized?

To make this form legally binding, it must be notarized. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session.

Common mistakes

- Not specifying the maximum line of credit allowed.

- Failing to detail the collateral securing the note.

- Leaving out the interest rate or payment schedule.

- Not having both parties sign the document.

Why use this form online

- Convenient access: Easily download and fill out the form at your convenience.

- Editability: Customize the terms based on specific needs before finalizing.

- Legal validity: Templates are crafted by licensed attorneys, ensuring compliance with laws.

Form popularity

FAQ

Writing the Promissory Note Terms You don't have to write a promissory note from scratch. You can use a template or create a promissory note online.

Borrower and Lender Details. A promissory note outlines information about both parties including the names, streets addresses, city, state and zip code of each party. Loan Information. Legal Language. Signatures. Warnings.

In order for a promissory note to be valid, both the lender and the borrower must sign the documentation. If you are a co-signer for the loan, you are required to sign the promissory note. Being a co-signer requires you to repay the loan amount in the instance that the borrower defaults on payment.

Write the date of the writing of the promissory note at the top of the page. Write the amount of the note. Describe the note terms. Write the interest rate. State if the note is secured or unsecured. Include the names of both the lender and the borrower on the note, indicating which person is which.

A promissory note basically includes the name of both parties (lender and borrower), date of the loan, the amount, the date the loan will be repaid in full, frequency of loan payments, the interest rate charged on the loan payments, and any security agreement.

Keep the original promissory note. Once a lender executes a promissory note, he keeps the original of the promissory note. Accept full payment of the loan. Mark paid in full on the promissory note. Place a signature beside the paid in full notation. Mail the original promissory note to the borrower.

Navigate to the website: www.studentloans.gov. Click "Log In." Enter your FSA ID and Password. Click "Complete Master Promissory Note." Select the appropriate loan type. Enter Your Personal Information.

A promissory note is a contract, a binding agreement that someone will pay your business a sum of money. However under some circumstances if the note has been altered, it wasn't correctly written, or if you don't have the right to claim the debt then, the contract becomes null and void.

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.

A promissory note is a financial instrument that contains a written promise by one party (the note's issuer or maker) to pay another party (the note's payee) a definite sum of money, either on demand or at a specified future date.