Loan Agreement - Long Form

What this document covers

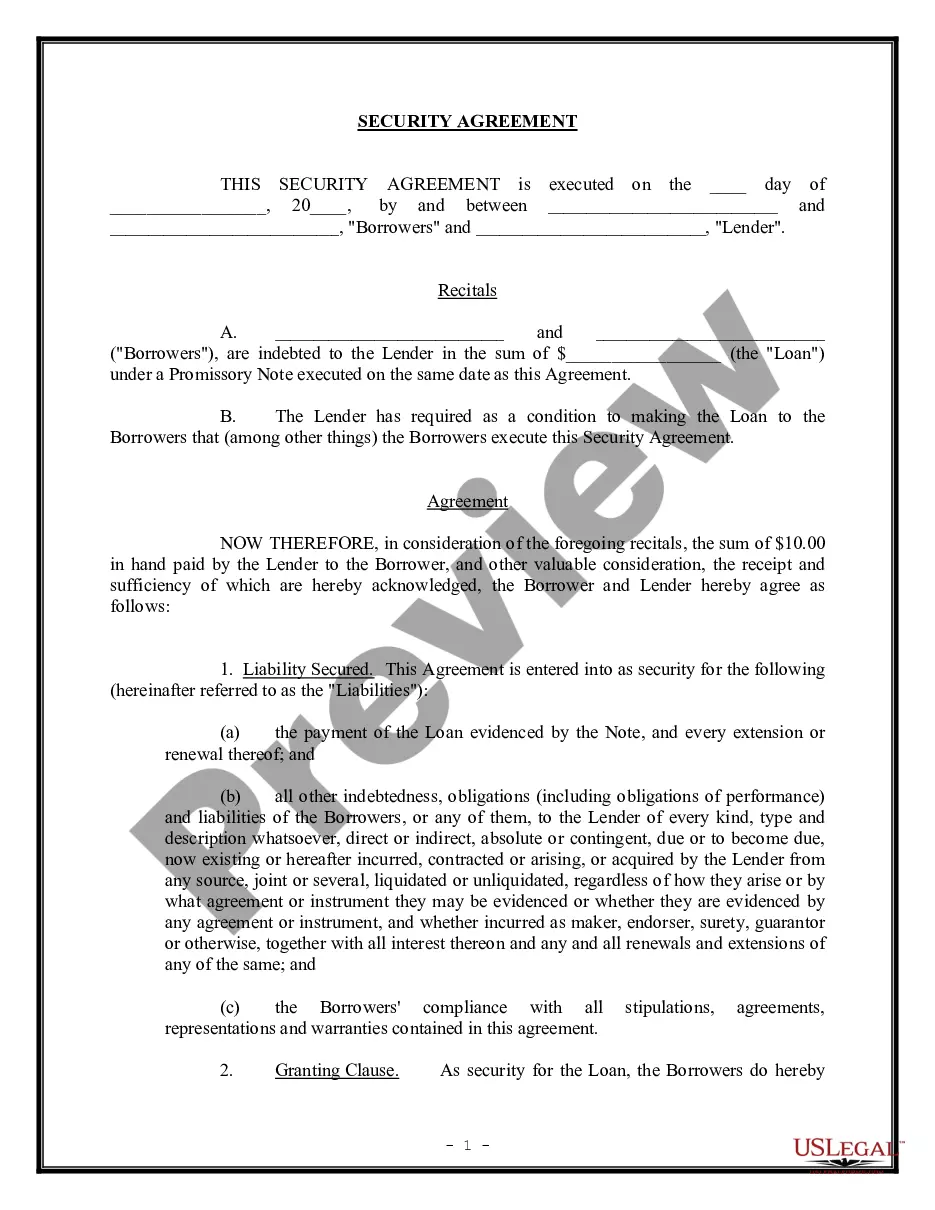

The Loan Agreement - Long Form is a legally binding document in which a lender agrees to provide a loan to a company under specified terms. This form differs from simpler loan agreements by outlining detailed clauses that govern the loan's conditions, repayment, and security provisions, ensuring that both parties understand their rights and obligations.

Key components of this form

- Borrower's and Lender's details

- Amount and terms of the loan

- Prepayment provisions

- Conditions precedent for lending

- Security agreements and guarantees

- Events of default and legal remedies

When to use this document

This Loan Agreement should be used when a company intends to borrow funds from a lender, particularly when the loan amount is substantial and requires detailed documentation. It is ideal for businesses in need of financing for operational purposes or project development, especially if the lender requires security and thorough verification of the borrower's creditworthiness.

Who this form is for

- Businesses seeking to secure a loan from banks or financial institutions

- Entrepreneurs needing detailed loan agreements for larger amounts

- Lenders requiring a comprehensive understanding of their rights and the borrower's obligations

- Legal professionals drafting agreements for their clients in business financing

Completing this form step by step

- Identify the parties involved: Enter the names and addresses of the lender and company borrowing the funds.

- Specify the loan amount and interest rate: Clearly state the total amount being borrowed and the agreed interest rate.

- Outline the repayment terms: Include the schedule for repayment and any prepayment options.

- Detail security for the loan: Specify any collateral being offered as security against the loan.

- Include signatures: Ensure that the authorized representatives from both parties sign and date the agreement to validate it.

Notarization guidance

This form does not typically require notarization unless specified by local law. However, it is advisable to consult with legal professionals to ensure that all local legal requirements are met.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include all necessary parties in the agreement

- Neglecting to specify repayment terms clearly

- Not accounting for the lender's security interests

- Omitting necessary documentation for loan approval

- Not having the agreement notarized when required

Benefits of completing this form online

- Convenience: Download and fill the form anytime and anywhere.

- Editability: Customize the agreement to meet specific business needs.

- Reliability: Ensure that the form is drafted by licensed attorneys, providing peace of mind.

Legal use & context

- The Loan Agreement outlines binding legal obligations for both lender and borrower.

- Failure to adhere to the terms can result in legal action or defaults specified in the agreement.

- It is crucial to ensure that all states' legal requirements are met for the agreement to be enforceable.

What to keep in mind

- The Loan Agreement - Long Form is designed for formal, structured loans between businesses and lenders.

- Careful completion and review of the agreement are essential to protect both parties' interests.

- Compliance with state-specific law is crucial for ensuring the agreement's enforceability.

Looking for another form?

Form popularity

FAQ

A loan agreement is a contract between you, the borrower and the lender.There are situations where you may no longer want the loan, or the item it financed. If there are valid reasons such as fraud or a breech of contract, you should be able to get out of the loan.

Starting the Document. Write the date at the top of the page. Write the Terms of the Loan. State the purpose of the personal payment agreement and the terms for returning the money. Date the Document. Statement of Agreement. Sign the Document. Record the Document.

Come up with a schedule for repayment. Use a family contract template that includes a repayment schedule. Set and interest rate. Put your agreement in writing. Keep payment records.

Step 1 Loan Amount, Borrower and Lender. Step 2 Payment. Step 3 Interest. Step 4 Expenses. Step 5 Governing Law. Step 6 Signing.

A loan agreement is a contract between a borrower and a lender which regulates the mutual promises made by each party.Loan agreements are usually in written form, but there is no legal reason why a loan agreement cannot be a purely oral contract (although oral agreements are more difficult to enforce).

Loan terms refers to the terms and conditions involved when borrowing money. This can include the loan's repayment period, the interest rate and fees associated with the loan, penalty fees borrowers might be charged, and any other special conditions that may apply.

Also known as a loan agreement. The main transaction document for a loan financing between one or more lenders and a borrower.

The addresses and contact information of all parties involved. The conditions of use of the loan (what the money can be used for) Any repayment options. The payment schedule. The interest rates. The length of the term. Any collateral. The cancellation policy.

A personal loan agreement is a legally binding document regardless of whether the lender is a financial institution or another person. The consequences are the same if you default on the contract. As a borrower, you could be sued by the lender or lose the asset or assets used to secure the loan.

Step 1 Loan Amount, Borrower and Lender. Step 2 Payment. Step 3 Interest. Step 4 Expenses. Step 5 Governing Law. Step 6 Signing.